Die Bibliothek · 014 · Industry ReportDie Bibliothek · 014 · 산업 보고서

As fashion executives look ahead to 2026, they are contending with a fundamentally new reality. US tariffs have redrawn global trade maps and forced brands and suppliers to rapidly adjust. Consumers are rethinking their spending, seeking value and redirecting share-of-wallet toward health and wellbeing. The swift onset of AI means fashion leaders are simultaneously navigating a rapidly changing technological landscape. The disruptions may feel daunting, but in BoF and McKinsey's reading, they are part of a wider set of longer-term systemic shifts the report has been tracking for ten years.2026년을 앞두고 패션 임원들은 근본적으로 새로운 현실과 마주하고 있다. 미국 관세는 글로벌 무역 지도를 다시 그렸고, 브랜드와 공급사는 빠르게 조정과 적응을 강요받았다. 소비자들은 지출을 재고하며 가치(value)를 찾고, 자신의 건강과 웰빙을 향해 지갑 점유율을 옮기고 있다. AI의 빠른 도래는 패션 리더들이 동시에 빠르게 변화하는 기술 지형을 항행해야 함을 의미한다. 이러한 격변은 부담스럽게 느껴질 수 있지만, BoF와 McKinsey의 해석에 따르면 이는 본 보고서가 10년에 걸쳐 추적해 온 더 큰 구조적 변화의 일부다.

Whereas in previous years executives were uncertain about what lay ahead, now they appear to have accepted that constant change is simply the new normal. ‘Challenging’ has overtaken ‘uncertainty’ as the word executives use most frequently to describe the industry, with tariffs cited as the number one hurdle. Forty-six percent expect conditions to worsen in 2026, up from 39% in last year's survey. By geography, 36% view North America as unpromising or very unpromising — double last year's share. Not everyone is downbeat: 25% believe conditions will improve, up from 20%. Sentiment toward China is picking up: 28% view it as unpromising in 2026, down from 41% a year earlier.전년까지 임원들이 ‘앞날에 대한 불확실함’을 안고 있었다면, 이제는 ‘끊임없는 변화가 곧 새로운 정상’임을 받아들인 것으로 보인다. 임원들이 산업을 가장 자주 묘사하는 단어는 ‘불확실(uncertainty)’에서 ‘도전적(challenging)’으로 바뀌었으며, 1위 장벽으로는 관세가 꼽힌다. 46%가 2026년 여건 악화를 전망하며 전년의 39%에서 상승했다. 지역별로는 36%가 북미를 ‘전망이 어둡거나 매우 어둡다’고 평가 — 전년의 두 배. 모두가 비관적인 것은 아니다: 25%는 여건이 개선될 것으로 보며 전년의 20%에서 상승. 중국에 대한 정서도 회복 중이다 — 2026년 전망에서 28%가 ‘어둡다’고 답했으며, 1년 전의 41%에서 큰 폭으로 감소.

With turbulent conditions — volatile input costs, supply chain disruptions, slow growth straining fashion's economic model — AI is shifting from a competitive edge to a business necessity. Companies are reshaping workforces, with some existing jobs becoming more AI-centric and roles shifting toward higher-value creative and analytical tasks. To harness this change, companies must redesign processes, compete for AI talent (often outside the fashion ecosystem), and protect the essential creativity that makes fashion tick. The mandate is a shift from small pilots toward a fundamental reassessment of how organisations work.변동성이 큰 투입 비용, 공급망 단절, 패션의 경제 모델에 부담을 주는 저성장 등 격변하는 여건 속에서, AI는 경쟁 우위에서 비즈니스 필수재로 이동하고 있다. 기업들은 일부 기존 직무를 AI 중심으로 재편하고, 역할은 더 높은 가치의 창의적·분석적 업무로 이동하면서 인력을 재구성하고 있다. 이 변화를 활용하기 위해 기업들은 프로세스를 재설계하고, (흔히 패션 생태계 밖에서) AI 인재 확보를 위해 경쟁해야 하며, 패션을 작동시키는 본질적 창의성을 보호해야 한다. 명령은 명확하다 — ‘작은 파일럿’에서 ‘조직 운영 방식 자체에 대한 근본적 재평가’로의 전환.

AI is also transforming how people shop. Customers are turning to large language models to search for products, compare offerings, and receive tailored recommendations. Some already use AI as style and wardrobe consultants. As agentic commerce emerges, brand presence in AI chatbot responses becomes the new SEO. Generative engine optimisation will be a 2026 priority.AI는 사람들이 쇼핑하는 방식 또한 바꾸고 있다. 고객들은 제품을 검색하고, 비교하고, 맞춤 추천을 받기 위해 LLM에 의존하기 시작했다. 일부는 이미 AI를 스타일·옷장 자문가로 활용 중이다. 에이전틱 커머스가 부상하면서, AI 챗봇 응답 안에서의 브랜드 존재감이 새로운 SEO가 된다. ‘Generative Engine Optimisation(GEO)’이 2026년의 우선 과제가 될 것이다.

The report concludes that 2026's main agenda will be adapting to an environment where trade, consumer behaviour, and technology remain in simultaneous flux. Agile brands that can adapt quickly are most likely to emerge as the winners.보고서는 2026년의 주요 의제가 ‘무역, 소비자 행동, 기술이 동시에 유동적인 환경에 대한 적응’이 될 것이라고 결론짓는다. 빠르게 적응할 수 있는 민첩한(agile) 브랜드가 승자로 부상할 가능성이 가장 높다.

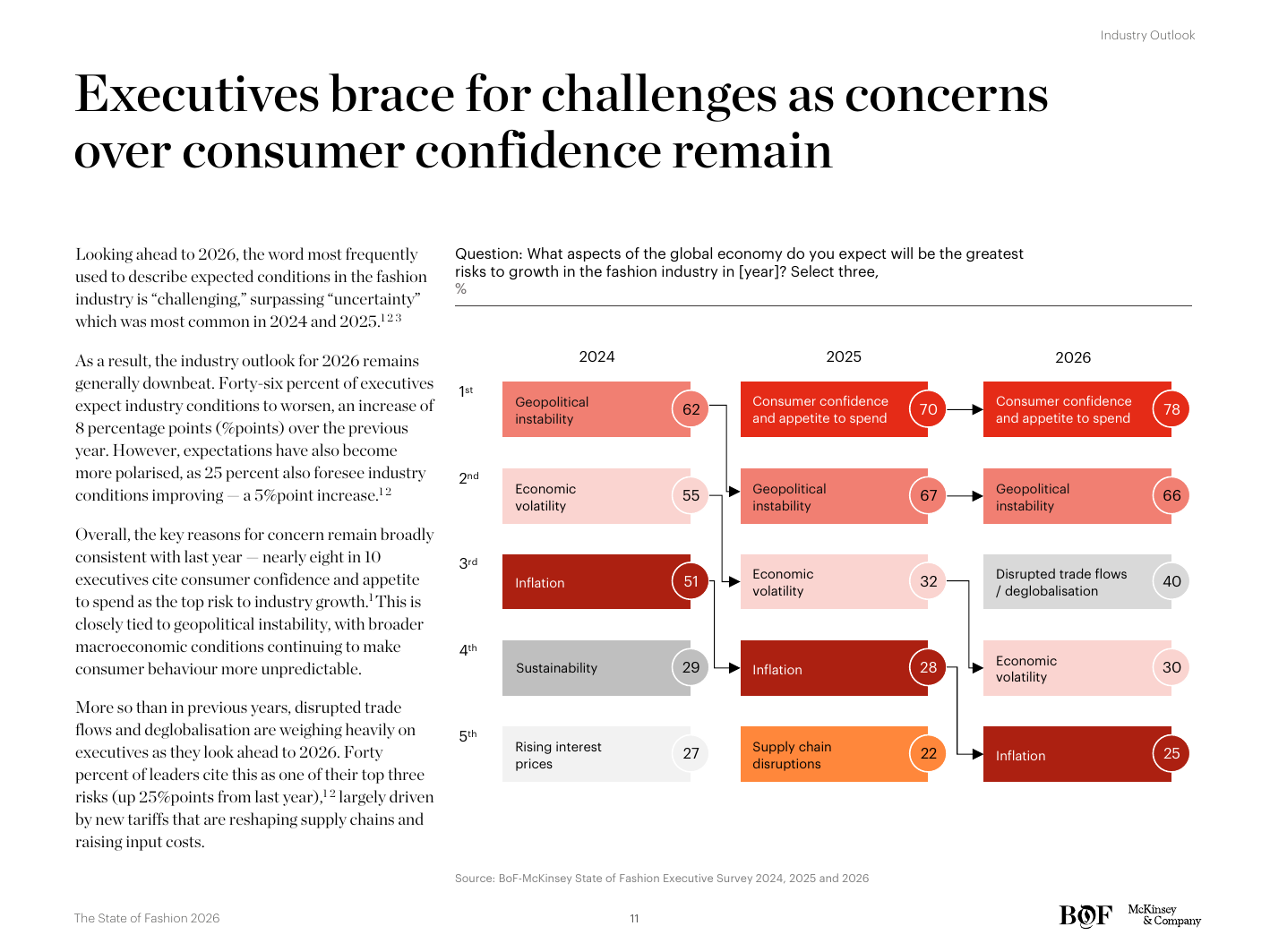

Looking ahead to 2026, the word most used to describe expected conditions in the fashion industry is ‘challenging,’ surpassing ‘uncertainty’ which was most common in 2024 and 2025. Many fashion industry leaders enter the new year bracing for further disruption, particularly stemming from US tariffs and weak consumer confidence. Overall the key reasons for concern remain broadly consistent with last year — ample aid for executives to call out consumer confidence and tariffs as the top risks — but the report notes a clearly heightened sense of instability, with executives flagging volatility itself as a structural feature rather than a temporary state.2026년을 바라보며 패션 산업의 예상 여건을 묘사하는 데 가장 많이 쓰인 단어는 ‘도전적(challenging)’이며, 이는 2024년과 2025년의 1위였던 ‘불확실(uncertainty)’을 추월했다. 패션 산업의 많은 리더들은 미국 관세와 약한 소비 심리에서 비롯된 추가 단절(disruption)에 대비하며 새해를 맞고 있다. 우려의 이유는 작년과 큰 틀에서 일치하지만 — 임원들이 소비 심리와 관세를 1위 리스크로 꼽는 데는 충분한 근거가 있다 — 보고서는 변동성 자체가 일시적 상태가 아니라 구조적 특성으로 자리 잡았다는 점을 임원들이 지적하고 있다고 명시한다.

McKinsey projects global fashion industry revenue growth in the low single-digit range for 2026, with continued bifurcation between value/discount and the rest. Luxury is expected to improve modestly relative to 2025 but to remain well below the double-digit run rate of the post-pandemic years. The fashion segment overall is expected to hold a low single-digit growth profile, with regional dispersion: continued caution in North America given tariff and macro overhang, gradual recovery in China, and resilient growth in India and the Middle East.McKinsey는 2026년 글로벌 패션 산업 매출 성장률을 한 자릿수 초반으로 전망하며, 밸류·디스카운트 세그먼트와 그 외의 분기(分岐)는 지속될 것으로 본다. 럭셔리는 2025년 대비 완만한 개선이 예상되나, 팬데믹 이후 두 자릿수 성장률에는 크게 못 미친다. 패션 세그먼트 전체는 한 자릿수 초반 성장 프로필을 유지할 것으로 예상되며, 지역별 분포는 다음과 같다: 관세와 거시 부담을 안은 북미는 지속적 신중함, 중국은 점진적 회복, 인도와 중동은 견조한 성장.

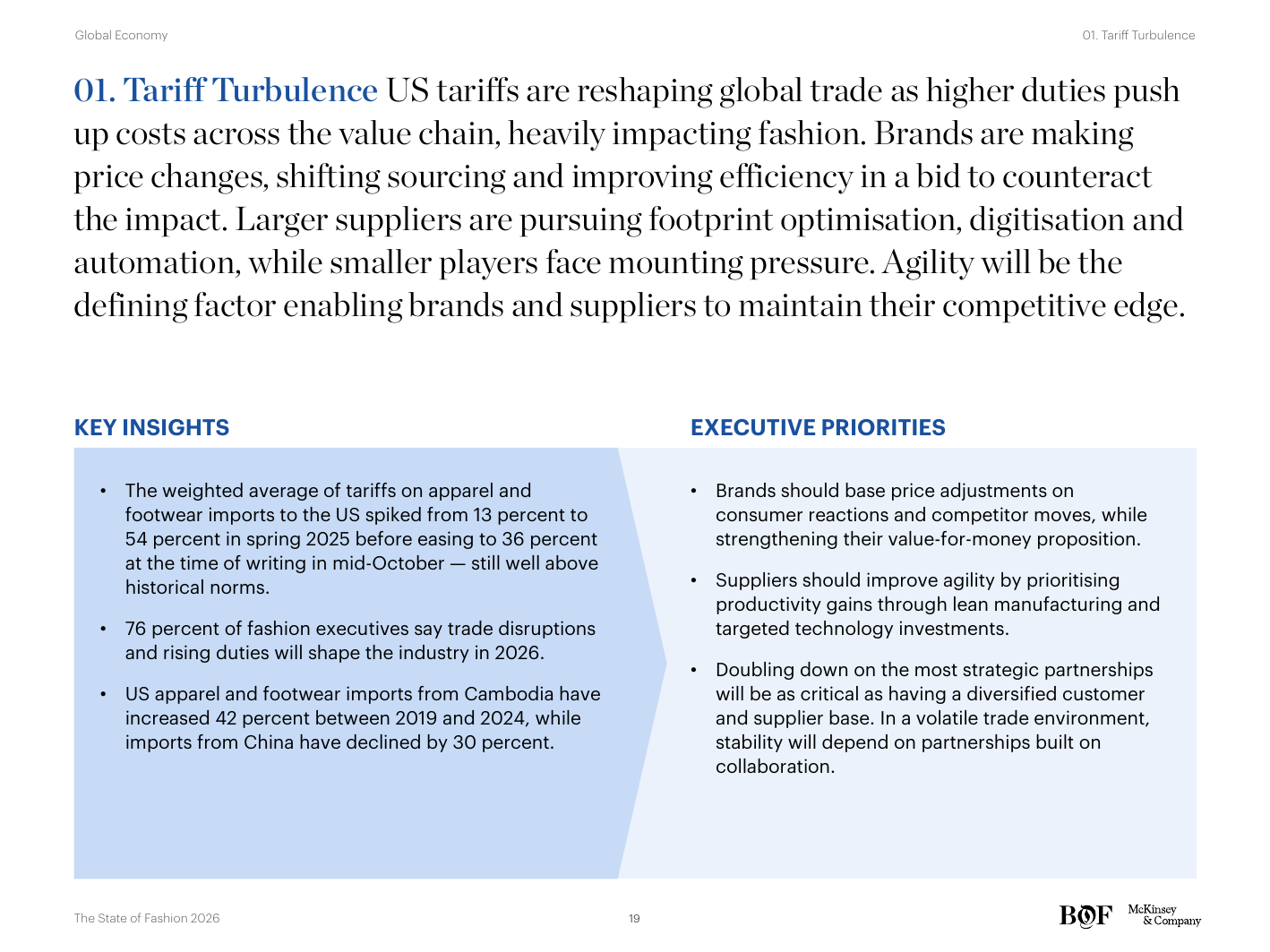

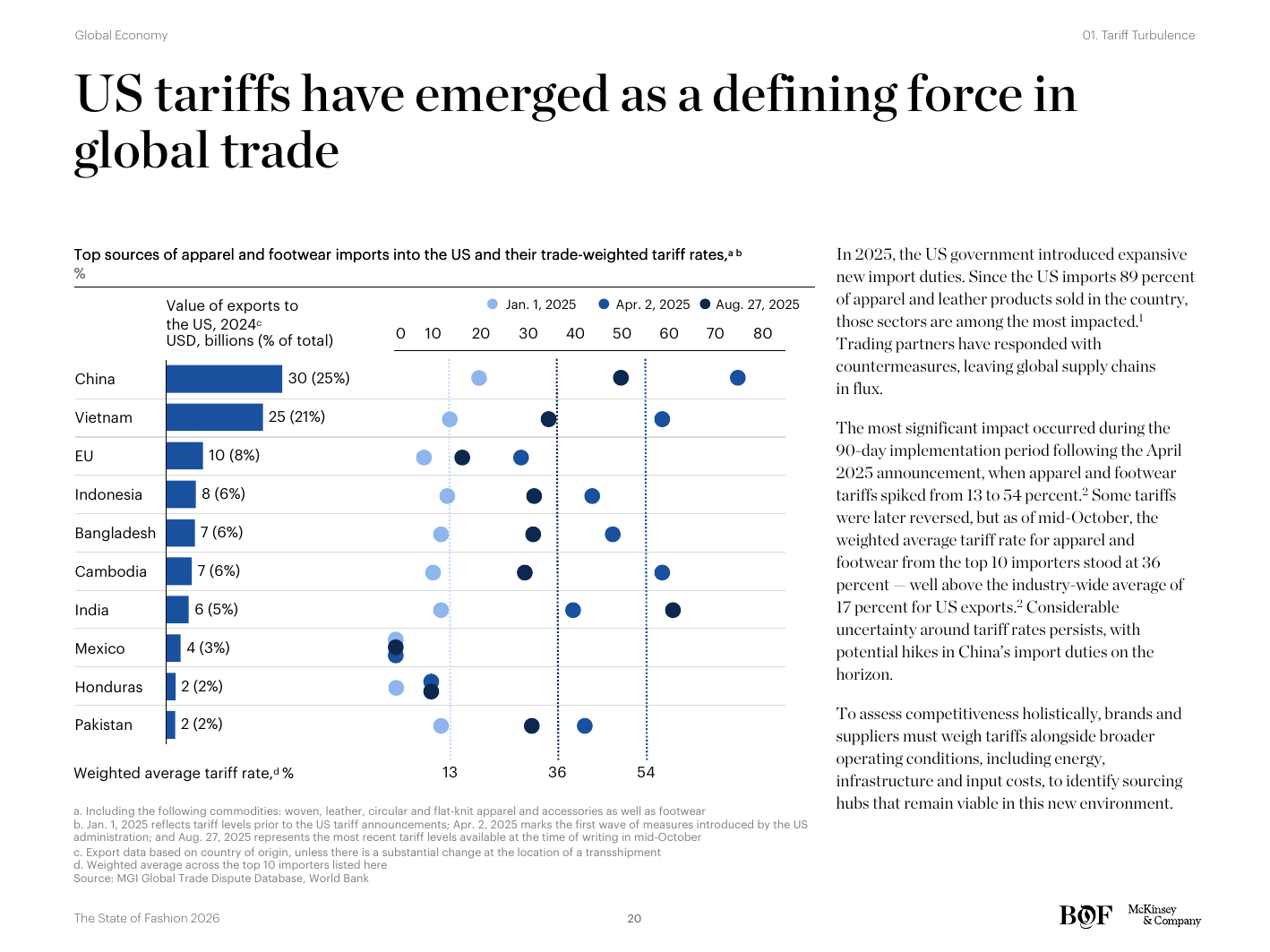

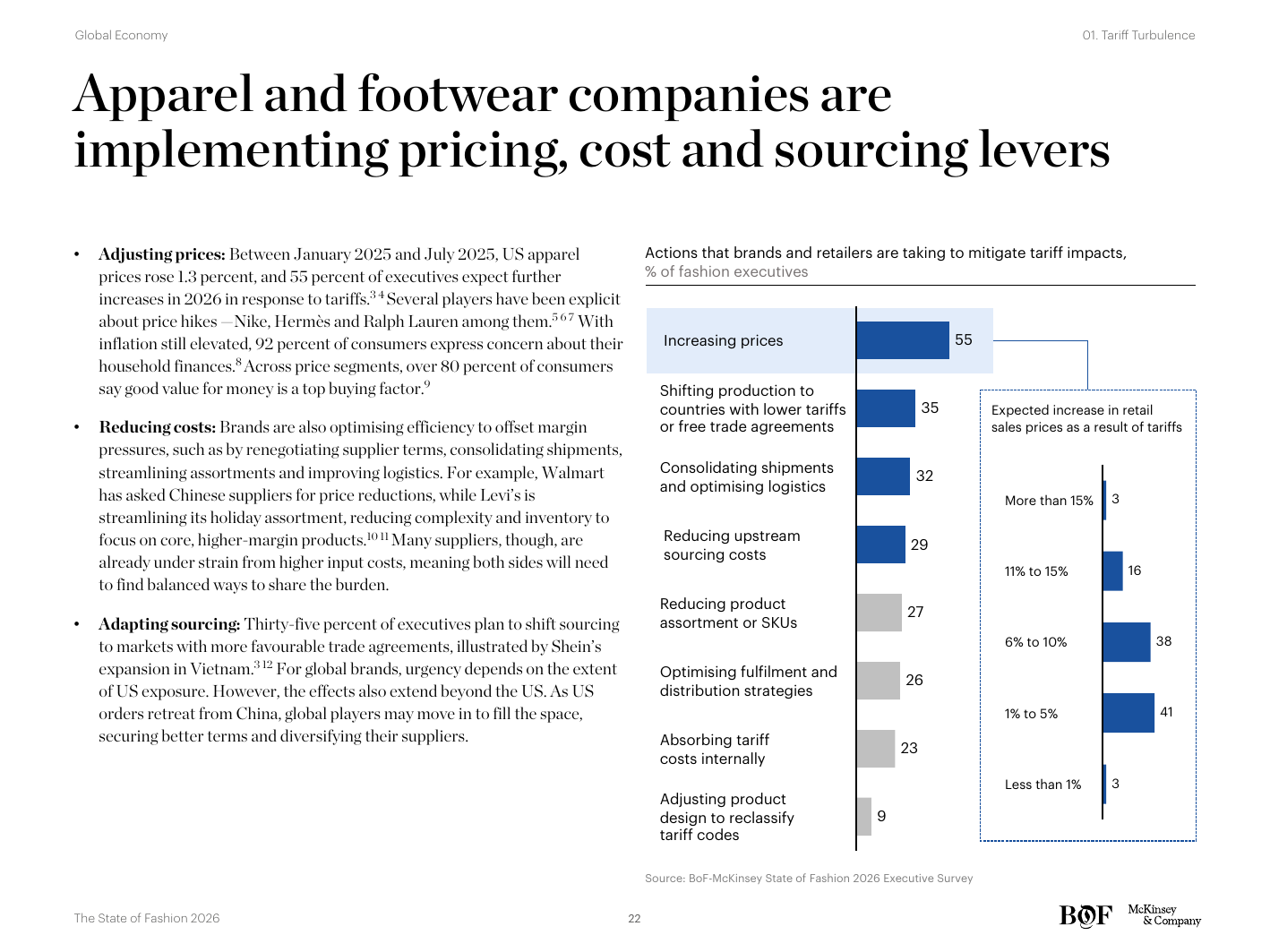

US tariffs are reshaping global trade as higher duties push up costs across the value chain, heavily impacting fashion. The weighted average of tariffs on apparel and footwear imports to the US spiked from 13% to 54% in spring 2025 before easing to 36% at the time of writing — still well above historical norms. Brands are making price changes, shifting sourcing and improving efficiency in a bid to counteract the impact. Larger suppliers are pursuing footprint optimisation, digitisation and automation, while smaller players face mounting pressure. Agility will be the defining factor enabling brands and suppliers to maintain their competitive edge.미국 관세는 가치사슬 전반의 비용을 끌어올리며 글로벌 무역을 재편하고 있으며, 패션 산업에 큰 충격을 주고 있다. 미국 의류·신발 수입에 대한 가중평균 관세는 2025년 봄 13%에서 54%로 급등한 뒤, 본 보고서 집필 시점에 36%로 안정되었으나 — 여전히 과거 평균을 크게 상회한다. 브랜드들은 가격 조정, 소싱 이동, 효율 개선으로 충격을 상쇄하려 하고 있다. 대형 공급사들은 생산 거점 최적화, 디지털화, 자동화를 추진 중이고, 소형 플레이어들은 가중되는 압박에 직면해 있다. 민첩성(agility)이 브랜드와 공급사의 경쟁력을 좌우하는 결정적 요인이 될 것이다.

Three numerical anchors define the chapter. 76% of fashion executives say trade disruptions and rising duties will shape the industry in 2026. US apparel and footwear imports from Cambodia have increased 42% between 2019 and 2024, while imports from China have declined by 30% — a sustained sourcing rotation that began before this tariff wave and is now accelerating. And executive surveys show the most-cited mitigation actions are: shifting sourcing, raising prices, redesigning products to lower duty classifications, and renegotiating supplier terms.본 장을 정의하는 세 가지 수치적 앵커. 패션 임원의 76%가 무역 단절과 관세 상승이 2026년 산업을 좌우할 것이라 답한다. 미국 의류·신발 수입은 2019년에서 2024년 사이 캄보디아에서 42% 증가, 중국에서 30% 감소했다 — 이번 관세 파동 이전부터 시작된 소싱 회전이 가속화되는 흐름이다. 그리고 임원 조사가 보여 주는 가장 자주 언급되는 완화 조치는 다음과 같다: 소싱 이동, 가격 인상, 더 낮은 관세 분류로의 제품 재설계, 그리고 공급사 거래 조건 재협상.

Gass took over Levi's in 2024 from Chip Bergh and has since accelerated a streamlining strategy: divesting non-core categories, narrowing the wholesale account base, and doubling down on direct-to-consumer. Her tariff thesis is that the brands which can articulate clear consumer value — durable, well-made, with a story — will absorb the cost increases better than those competing primarily on price. In her words, in a volatile environment, the only durable answer is to simplify the model and double down on the few things customers come to you for.Gass는 2024년 Chip Bergh로부터 Levi's를 인계받은 후 단순화 전략을 가속화해 왔다 — 비핵심 카테고리 매각, 도매 계정 기반 축소, DTC 강화. 그녀의 관세 명제는 다음과 같다: 명확한 소비자 가치 — 내구성 있고, 잘 만들어지고, 이야기를 가진 — 를 표현할 수 있는 브랜드가, 주로 가격으로 경쟁하는 브랜드보다 비용 상승을 더 잘 흡수할 것이다. 그녀의 표현으로, 변동성이 큰 환경에서 유일하게 내구성 있는 답은 모델을 단순화하고 고객이 우리에게 찾아오는 소수의 것에 집중하는 것이다.

“Consumers are still going to buy, but as more and more brands raise prices, [shoppers will] migrate to brands that do have that value in the broadest sense.”“소비자들은 여전히 구매를 합니다. 그러나 점점 더 많은 브랜드가 가격을 올릴수록, 쇼퍼들은 가장 넓은 의미의 ‘가치’를 제공하는 브랜드로 이동할 것입니다.” — Michelle Gass

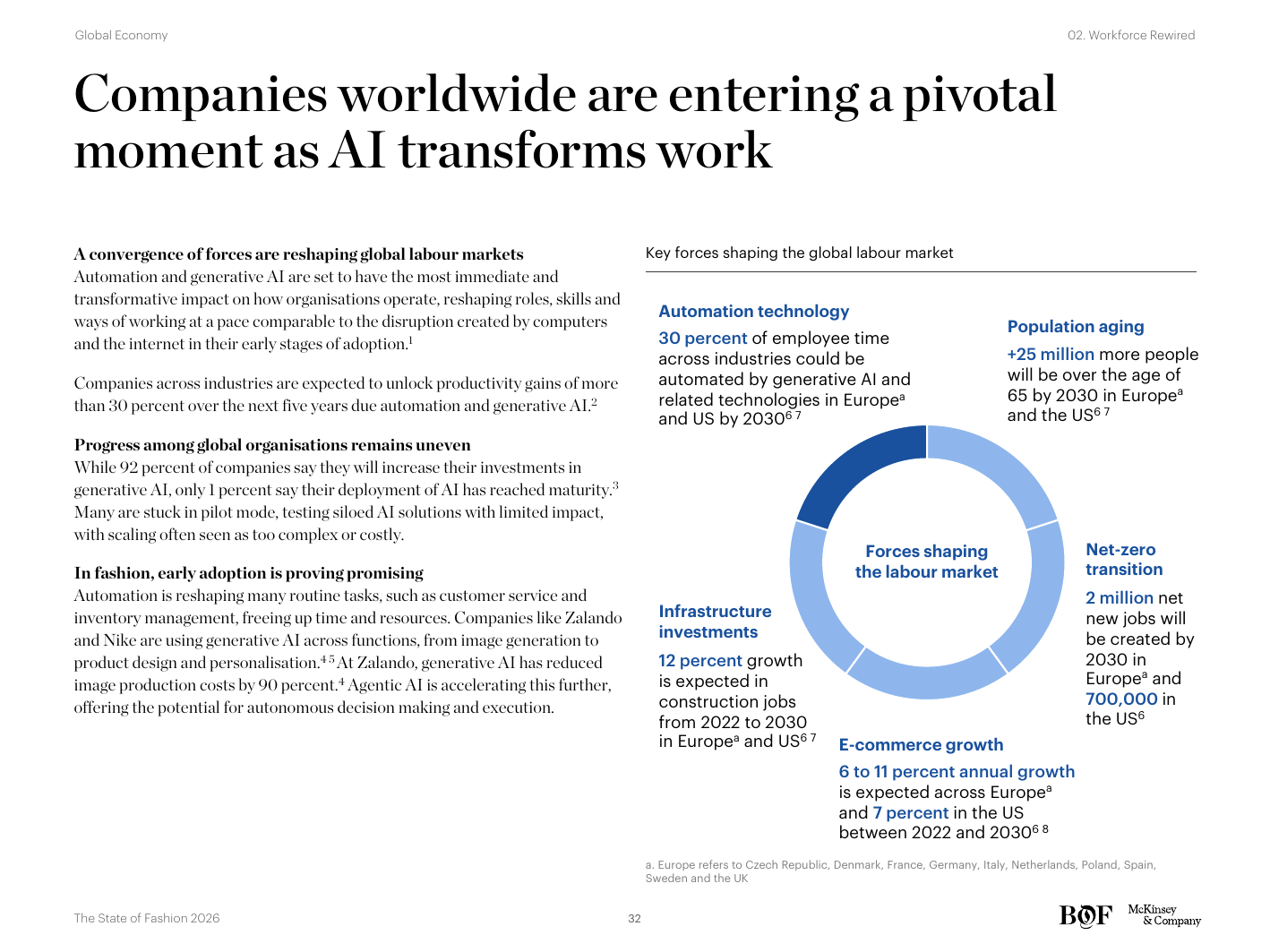

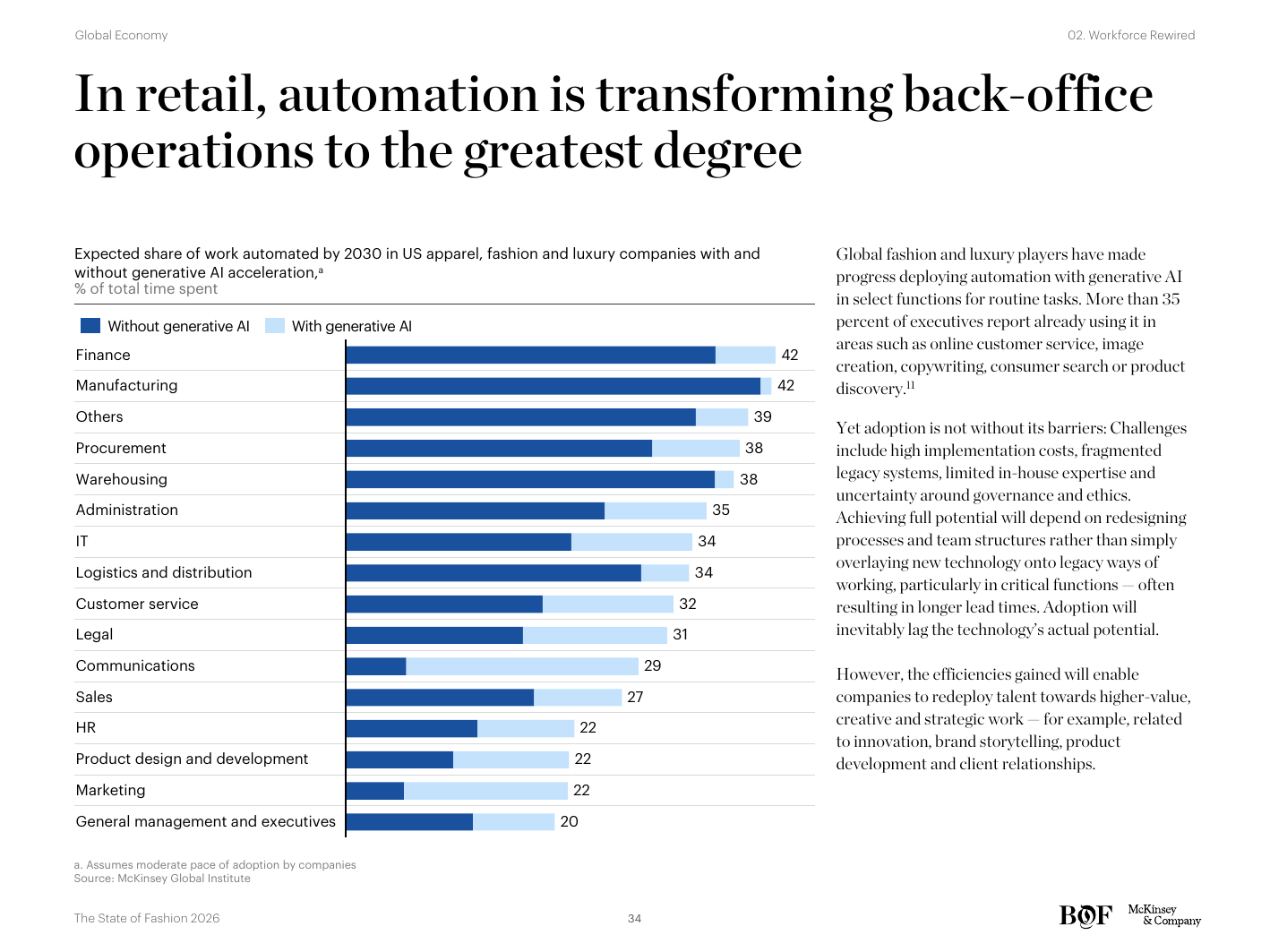

Technology is changing workforces globally, and fashion is no exception. The report frames 2026 as the year the AI workforce transition crosses from pilot to operating model. Companies are entering a pivotal moment as AI transforms work across functions. Generative AI is accelerating shifts in marketing, merchandising and sales most rapidly. Fashion players need to reskill teams and recruit tech expertise (often from outside the fashion ecosystem) to mature their AI pilots into integrated production capabilities.기술이 전 세계 노동력을 바꾸고 있으며, 패션도 예외가 아니다. 보고서는 2026년을 AI 노동력 전환이 파일럿에서 운영 모델로 넘어가는 해로 규정한다. 기업들은 AI가 기능 전반에 걸쳐 일을 변환하는 결정적 시기에 진입하고 있다. 생성형 AI는 마케팅, 머천다이징, 세일즈에서 가장 빠르게 변화를 가속화하고 있다. 패션 플레이어들은 파일럿을 통합된 프로덕션 역량으로 성숙시키기 위해 팀을 재교육하고 (흔히 패션 생태계 외부에서) 기술 전문성을 영입해야 한다.

McKinsey's projection on automation is the central data point: a meaningful share of work in US apparel, fashion and luxury companies is expected to be automated by 2030, with the share substantially higher in companies that actively integrate AI. The integration question is not whether AI will impact functions but at what depth: surface-level chatbots and copywriting tools versus deeply embedded systems that change merchandise planning, allocation, demand forecasting, and design ideation.McKinsey의 자동화 전망이 핵심 데이터 포인트다 — 미국 의류·패션·럭셔리 기업 업무 중 의미 있는 비중이 2030년까지 자동화될 것으로 예상되며, AI를 적극적으로 통합한 기업에서는 그 비중이 훨씬 더 높다. 통합의 질문은 ‘AI가 기능에 영향을 줄 것인가’가 아니라 ‘어느 깊이까지 영향을 줄 것인가’다 — 표면적 챗봇과 카피 도구 vs 머천다이즈 플래닝, 어로케이션, 수요 예측, 디자인 아이디에이션을 바꾸는 깊이 내장된 시스템.

The report's executive prescription: integrate AI into core creative and operational processes, elevate AI-fluent roles into senior leadership, and build seamless data-and-tool architectures rather than continue accumulating disconnected pilots. The brands that win in 2026 will be the ones whose operating model has been redesigned around AI capability rather than the ones that have done the most demos.보고서의 임원 처방: AI를 핵심 크리에이티브 및 운영 프로세스에 통합하고, AI에 능숙한 역할을 시니어 리더십으로 격상시키며, 단절된 파일럿을 누적하기보다 매끄러운 데이터·도구 아키텍처를 구축할 것. 2026년에 승리하는 브랜드는 가장 많은 데모를 한 곳이 아니라, 운영 모델이 AI 역량을 중심으로 재설계된 곳이 될 것이다.

Artificial intelligence is already disrupting how shoppers discover, compare and buy. While traditional search still dominates, shoppers are increasingly turning to large language models for product research, side-by-side comparisons, and personalised recommendations. The structural shift the report flags: generative engine optimisation (GEO) — appearing well in LLM responses — is becoming an essential add-on to traditional search engine optimisation. Brands not appearing in ChatGPT or Gemini responses for category-defining queries will be invisible to the next generation of shoppers.AI는 이미 쇼퍼들이 발견하고, 비교하고, 구매하는 방식을 단절시키고 있다. 전통적 검색이 여전히 우세하지만, 쇼퍼들은 점차 LLM에 의존해 제품을 조사하고, 나란히 비교하고, 개인 맞춤 추천을 받는다. 보고서가 지목하는 구조적 이동: ‘Generative Engine Optimisation(GEO)’ — LLM 응답 안에서 잘 노출되는 것 — 이 전통적 SEO에 필수적으로 추가되는 능력이 되고 있다. 카테고리 정의적 질의에서 ChatGPT나 Gemini의 응답에 등장하지 않는 브랜드는, 차세대 쇼퍼들에게 보이지 않게 된다.

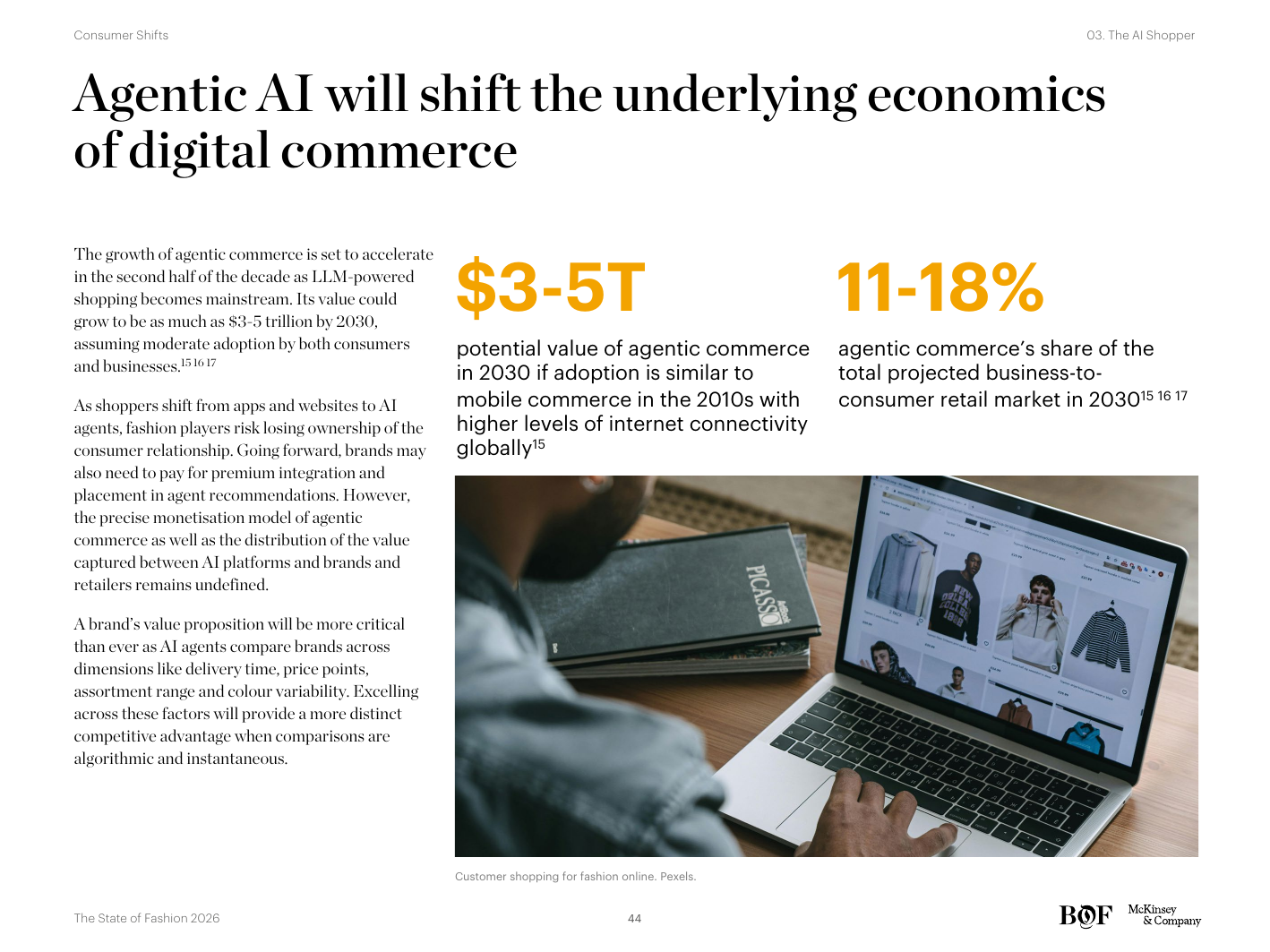

Looking further ahead, consumers could rely on autonomous AI agents to shop on their behalf. The report cites a McKinsey estimate that agentic commerce could be worth $3–5 trillion globally by 2030 if adoption matches the trajectory of comparable consumer-internet shifts. To compete in agentic commerce, some players are already exploring building their own shopping agents. Companies should optimise for agent interaction now — structured product data, machine-readable specs, agent-friendly checkout flows — to maximise discovery in the AI search era.더 멀리 내다보면, 소비자들은 자신을 대신해 쇼핑할 자율 AI 에이전트에 의존할 수 있다. 보고서는 McKinsey 전망을 인용하여, 에이전틱 커머스가 비교 가능한 소비자 인터넷 전환의 궤도를 따른다면 2030년까지 글로벌 3~5조 달러 규모가 될 수 있다고 밝힌다. 에이전틱 커머스에서 경쟁하기 위해 일부 플레이어들은 이미 자체 쇼핑 에이전트 구축을 모색 중이다. 기업들은 지금부터 에이전트 상호작용에 최적화해야 한다 — 구조화된 제품 데이터, 기계 판독 가능한 스펙, 에이전트 친화적 체크아웃 플로우 — AI 검색 시대의 발견을 극대화하기 위해.

Profound builds tools that monitor how brands show up in LLM responses to category-defining queries, then advise on the structured-data, content, and authority signals that influence those answers. Cadwallader's headline observation: when a consumer asks ChatGPT ‘what is the best luxury sneaker for men right now?’, the model is, in effect, a single highly opinionated salesperson speaking with extreme bias. Whether a brand appears in that answer is now a strategic question, not a marketing afterthought.Profound는 카테고리 정의적 질의에 대해 브랜드가 LLM 응답에서 어떻게 등장하는지를 모니터링하는 도구를 구축하고, 그 답변에 영향을 주는 구조화 데이터·콘텐츠·권위 신호에 대해 자문한다. Cadwallader의 핵심 관찰: 소비자가 ChatGPT에게 ‘지금 남성에게 가장 좋은 럭셔리 스니커는 무엇인가?’라고 물을 때, 모델은 사실상 매우 강한 편향을 가진 한 명의 세일즈맨처럼 답한다. 브랜드가 그 답변에 등장하는지는 이제 마케팅의 사후 과제가 아니라 전략적 질문이다.

“You're speaking to someone extremely biased…” — on how to think about brand presence inside LLM responses.“당신은 극도로 편향된 한 사람과 대화하고 있는 것입니다…” — LLM 응답 안에서의 브랜드 존재감에 관해.

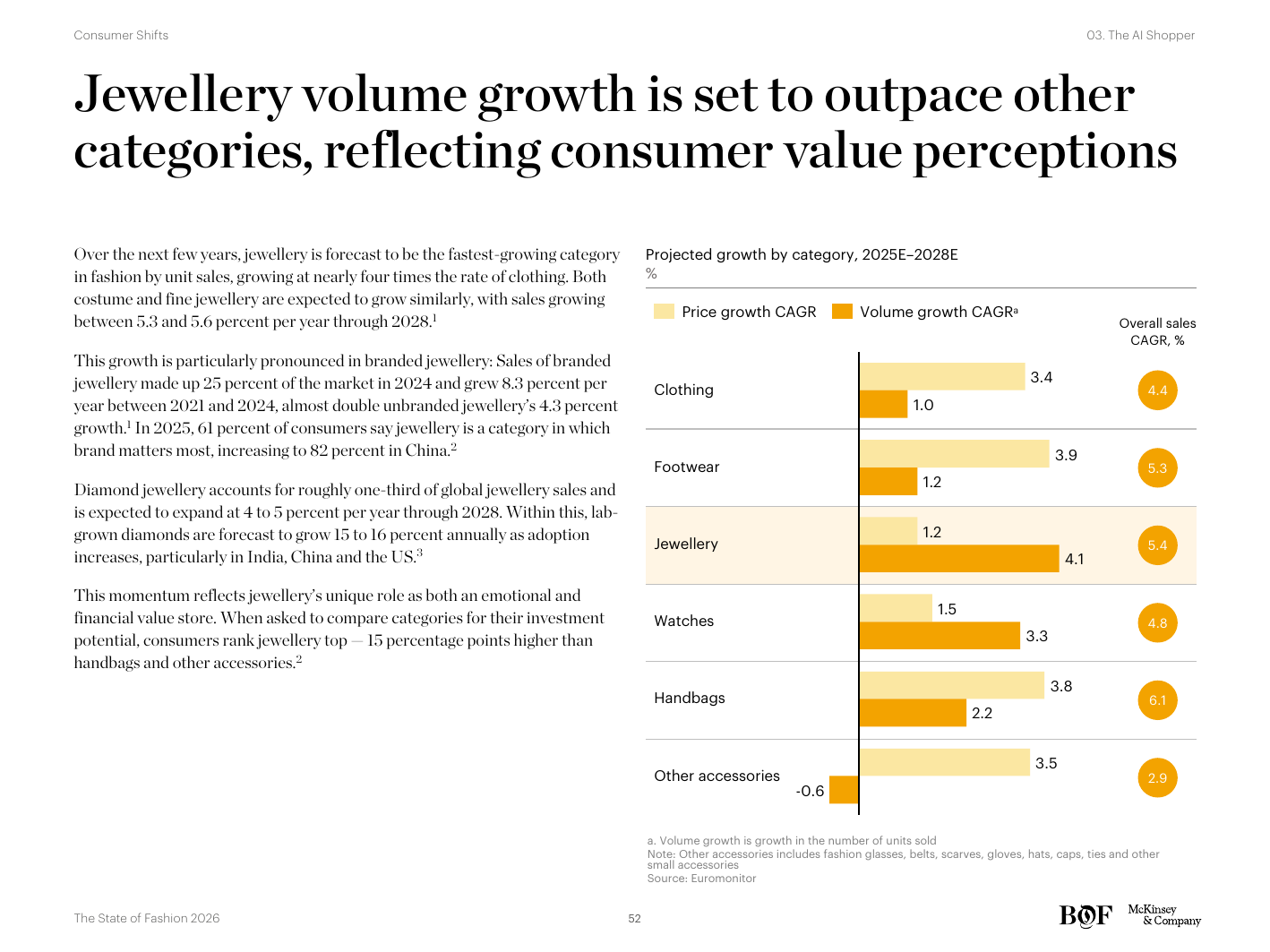

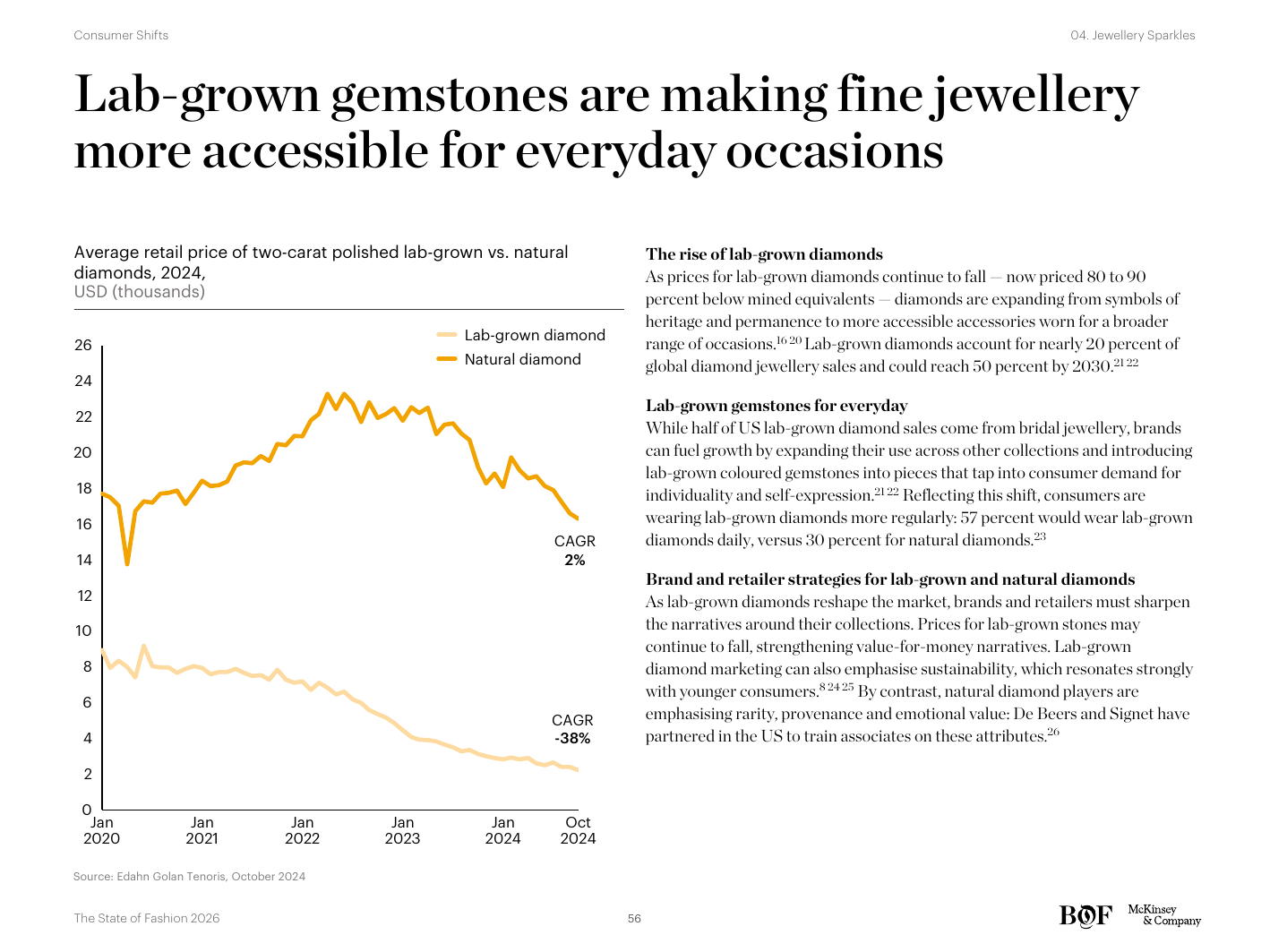

With unit-sales growth outpacing all other fashion segments, jewellery is the standout category in the 2026 outlook. The drivers are three. First, jewellery is moving beyond gifting into self-purchase: both men and women are increasingly buying it for themselves. Second, self-expression is becoming a defining force in the category across price segments, with the line between fashion jewellery and fine jewellery blurring. Third, lab-grown gemstones are making fine jewellery accessible for everyday occasions, expanding the addressable market while putting pressure on natural-stone pricing.단위 판매 성장률이 다른 모든 패션 세그먼트를 추월하면서, 주얼리는 2026년 전망에서 가장 두드러진 카테고리다. 동력은 세 가지다. 첫째, 주얼리는 선물(gifting)을 넘어 자기 자신을 위한 구매(self-purchase)로 이동 중 — 남녀 모두 자기 자신을 위해 더 많이 구매한다. 둘째, 가격대를 가로질러 자기 표현(self-expression)이 카테고리를 정의하는 힘이 되고 있으며, 패션 주얼리와 파인 주얼리 사이의 경계가 흐려지고 있다. 셋째, 랩그로운(lab-grown) 보석이 파인 주얼리를 일상적 상황에서도 접근 가능하게 만들고 있다 — 도달 가능한 시장을 확대하는 동시에 자연석 가격에 압박을 주고 있다.

Asia Pacific will continue to drive the largest share of jewellery market growth through 2028, led by China and India. Brands should capitalise on the sector's growing diversification and changing consumer tastes by widening their reach across price tiers without diluting their core identity. The mass-fashion jewellery and the high-fine-jewellery ends of the market are both expanding; the historically dominant gifting-only middle is the squeezed segment.아시아 태평양은 중국과 인도를 중심으로 2028년까지 주얼리 시장 성장의 가장 큰 비중을 차지할 전망이다. 브랜드들은 카테고리의 다각화와 변화하는 소비자 취향을 활용하기 위해, 핵심 정체성을 훼손하지 않으면서 가격대 전반으로 도달 범위를 확장해야 한다. 매스 패션 주얼리와 하이 파인 주얼리의 양 끝이 모두 확장 중이며, 역사적으로 우세했던 ‘선물 전용 중간(gifting-only middle)’ 세그먼트가 압박받는 영역이다.

Swarovski entered 2025 with strong momentum — its jewellery business grew 9% while luxury fashion struggled with price-hike fatigue. Nasard's thesis: the brand has succeeded by being clearly positioned in the affordable-luxury space, by treating the consumer as wanting jewellery for self-expression rather than as a status symbol alone, and by integrating lab-grown stones early enough to make them a creative asset rather than a defensive response.Swarovski는 2025년을 강한 모멘텀으로 시작했다 — 럭셔리 패션이 가격 인상 피로감에 시달리는 사이, 주얼리 사업은 9% 성장했다. Nasard의 명제: 브랜드는 ‘감당 가능한 럭셔리(affordable luxury)’ 공간에 명확히 포지셔닝됨으로써, 소비자를 ‘지위의 상징’이 아닌 ‘자기 표현을 원하는 사람’으로 다룸으로써, 그리고 랩그로운 보석을 방어적 반응이 아니라 크리에이티브 자산으로 만들 만큼 일찍 통합함으로써 성공했다.

“Lab-grown diamonds are a critical part of the future of jewellery.”“랩그로운 다이아몬드는 주얼리의 미래에서 결정적인 부분입니다.” — Alexis Nasard

On customisation, Nasard is candid: it has not been a category-defining lever for Swarovski, despite repeated industry predictions. Small periodic upticks four to six years ago, but no breakout. The lesson he draws is that consumers want clearly authored product they can choose from, not blank canvases to design themselves.커스터마이즈에 대해 Nasard는 솔직하다: 산업이 반복적으로 예측했던 것과 달리, Swarovski에게 카테고리 정의적 레버는 아니었다. 4~6년 전 일시적 소규모 상승은 있었으나 돌파구는 없었다. 그가 끌어내는 교훈은 이것이다 — 소비자들은 직접 설계할 빈 캔버스가 아니라, 선택 가능한 명확히 저자(author)가 있는 제품을 원한다.

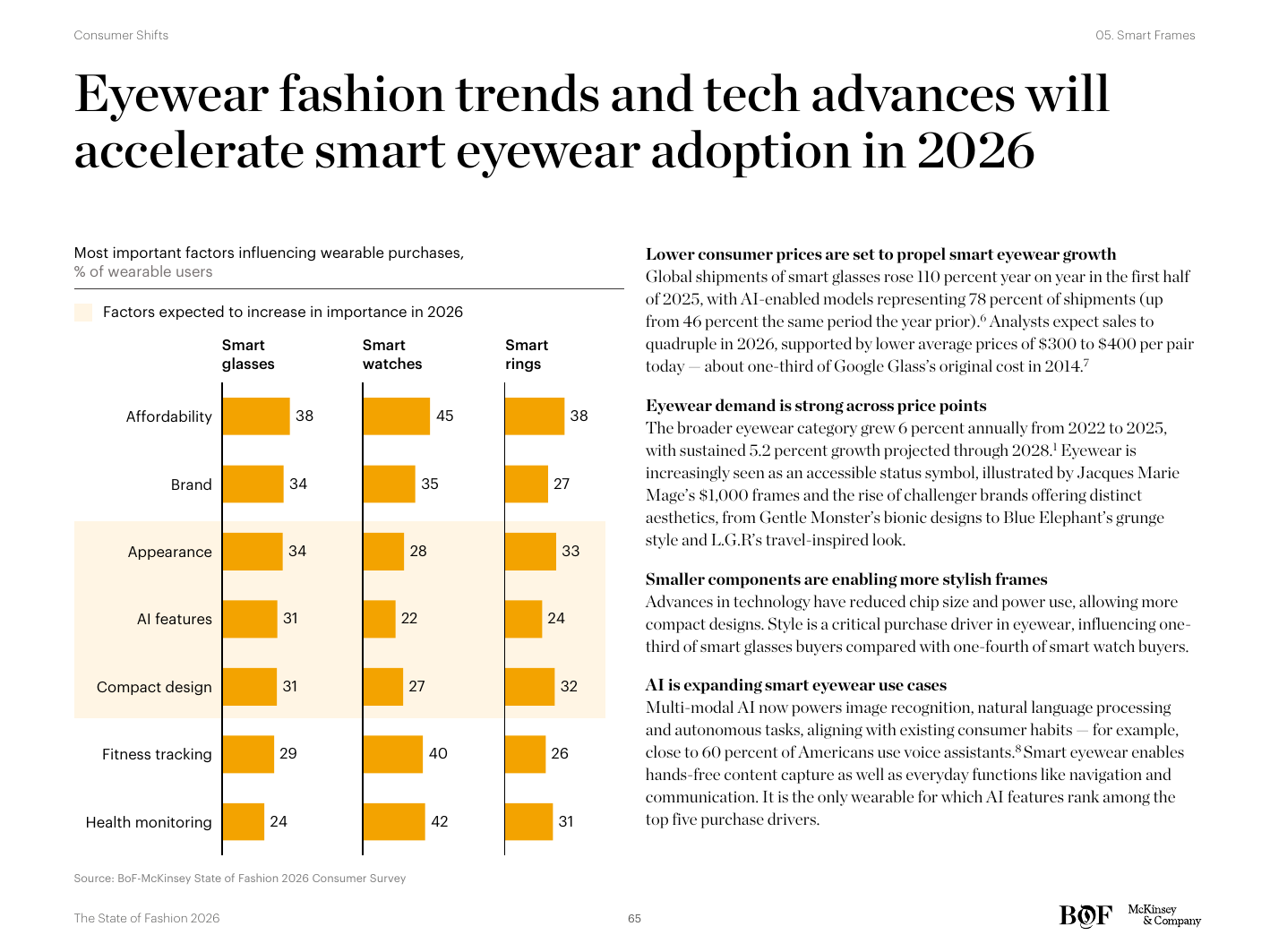

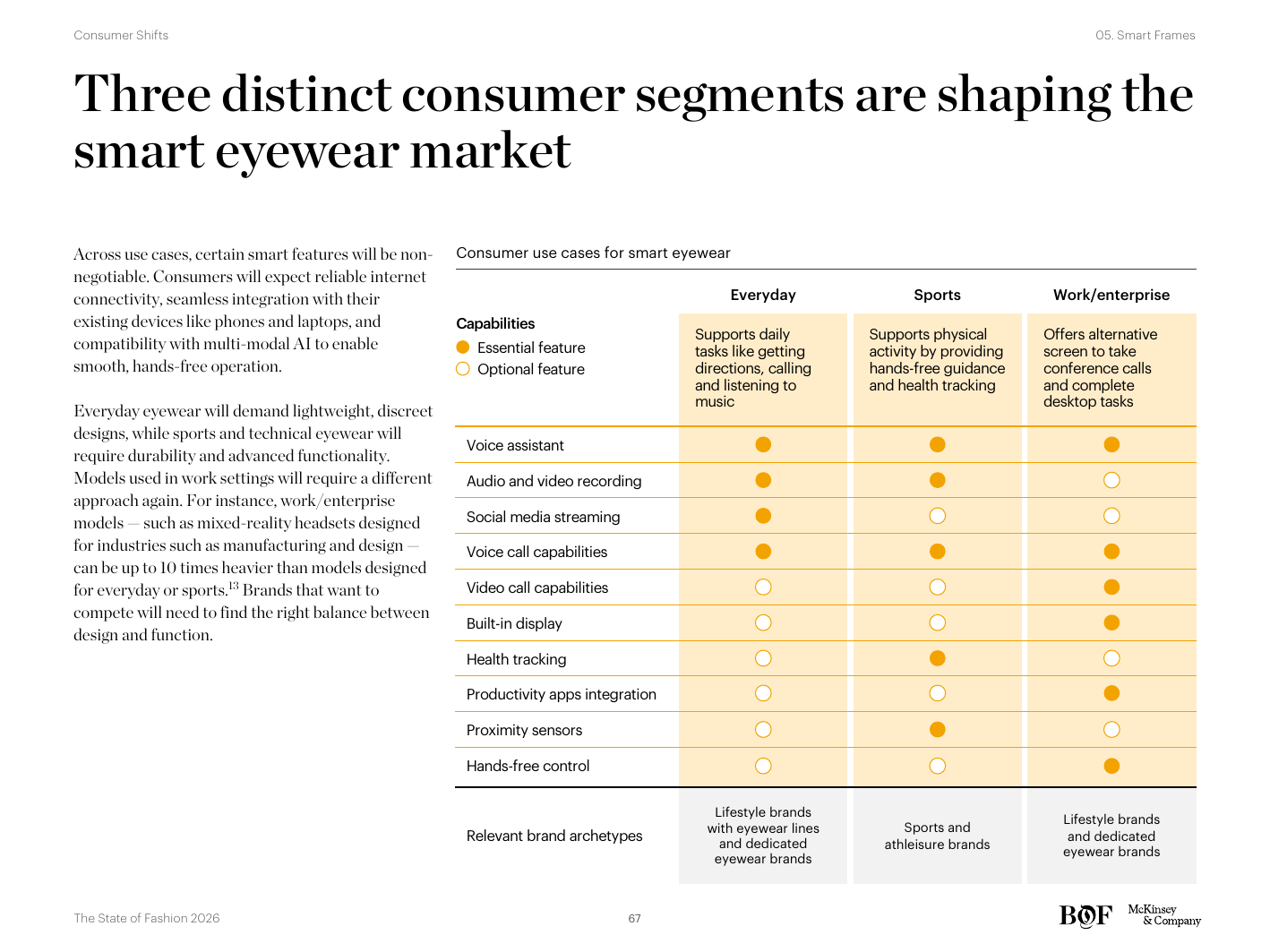

Style-conscious devices equipped with meaningful computing capability — smart eyewear — became, in 2025, the first credible fashion-tech wearable category. Wearables broadly will continue to be the fastest-growing accessory category, and smart eyewear specifically is poised to capture an outsized share. Lower consumer prices, improving battery life, and partnerships between tech companies and traditional eyewear groups (most notably EssilorLuxottica × Meta) are propelling growth. The report identifies three distinct consumer segments shaping the smart eyewear market: essential-feature buyers, lifestyle-enhancement buyers, and early-adopter premium buyers.의미 있는 컴퓨팅 역량을 갖춘 스타일 의식적 디바이스 — 스마트 아이웨어 — 가 2025년 처음으로 신뢰성 있는 패션-테크 웨어러블 카테고리가 되었다. 웨어러블 전반은 가장 빠르게 성장하는 액세서리 카테고리로 남고, 그 안에서도 특히 스마트 아이웨어가 비대칭적으로 큰 점유를 가져갈 것으로 보인다. 낮아지는 소비자 가격, 개선된 배터리 수명, 그리고 테크 기업과 전통 아이웨어 그룹 간 파트너십 (가장 두드러진 사례는 EssilorLuxottica × Meta) 이 성장을 견인하고 있다. 보고서는 스마트 아이웨어 시장을 형성하는 세 가지 별개의 소비자 세그먼트를 식별한다 — 필수 기능 구매자, 라이프스타일 강화 구매자, 그리고 얼리어답터 프리미엄 구매자.

Fashion's involvement in smart eyewear is recent, but 2026 is poised to offer more opportunities. Partnerships will drive the segment's growth as interest rises across both fashion and tech sides. Brands should think about smart eyewear as a new growth platform — eyewear specialists can move into computing-enabled SKUs, while non-eyewear fashion brands can partner with tech companies to enter the category.패션의 스마트 아이웨어 참여는 최근의 일이지만, 2026년은 더 많은 기회를 제공할 것으로 보인다. 패션과 테크 양쪽에서 관심이 높아지면서 파트너십이 세그먼트 성장의 핵심 동력이 될 것이다. 브랜드들은 스마트 아이웨어를 새로운 성장 플랫폼으로 사고해야 한다 — 아이웨어 전문 브랜드는 컴퓨팅 기능이 탑재된 SKU로 이동할 수 있고, 아이웨어가 아닌 패션 브랜드는 테크 기업과의 파트너십으로 카테고리에 진입할 수 있다.

For at least a decade tech companies have tried to make smart glasses a commercial success. EssilorLuxottica and Meta's sixth-year milestone is the first sign that the category has crossed the threshold. Basilico cites a striking customer-acquisition figure: over 60% of new wearable customers reach EssilorLuxottica through the smart-glass partnership — consumers who would not otherwise enter the brand. The smart-glasses launch is, in effect, becoming a customer-acquisition channel for the broader business.최소 10년 동안 테크 기업들은 스마트 글래스를 상업적 성공으로 만들기 위해 노력해 왔다. EssilorLuxottica와 Meta의 6년차 이정표는 카테고리가 임계점을 넘어섰다는 첫 신호다. Basilico는 인상적인 고객 획득 수치를 인용한다 — 새 웨어러블 고객의 60% 이상이 스마트 글래스 파트너십을 통해 EssilorLuxottica에 도달한다. 그렇지 않았다면 브랜드를 만나지 않았을 소비자들이다. 스마트 글래스 런칭은 사실상 더 넓은 사업을 위한 ‘고객 획득 채널’이 되고 있다.

On the path ahead: Basilico is candid that this is uncharted territory and the category will evolve with the product. The headline lesson for fashion: discovery is increasingly happening through products that do something, not products that simply look like something. For an industry historically wired around aesthetic differentiation alone, this is a structural shift.앞으로의 길에 관해, Basilico는 솔직하다 — 이는 미지의 영역이며 카테고리는 제품과 함께 진화할 것이다. 패션을 위한 핵심 교훈: 발견(discovery)은 점점 더 ‘무언가를 하는 제품’을 통해 일어나고 있으며, 단순히 ‘무언가처럼 보이는 제품’을 통해서가 아니다. 역사적으로 미적 차별화만을 중심으로 배선되어 온 산업에게, 이는 구조적 이동이다.

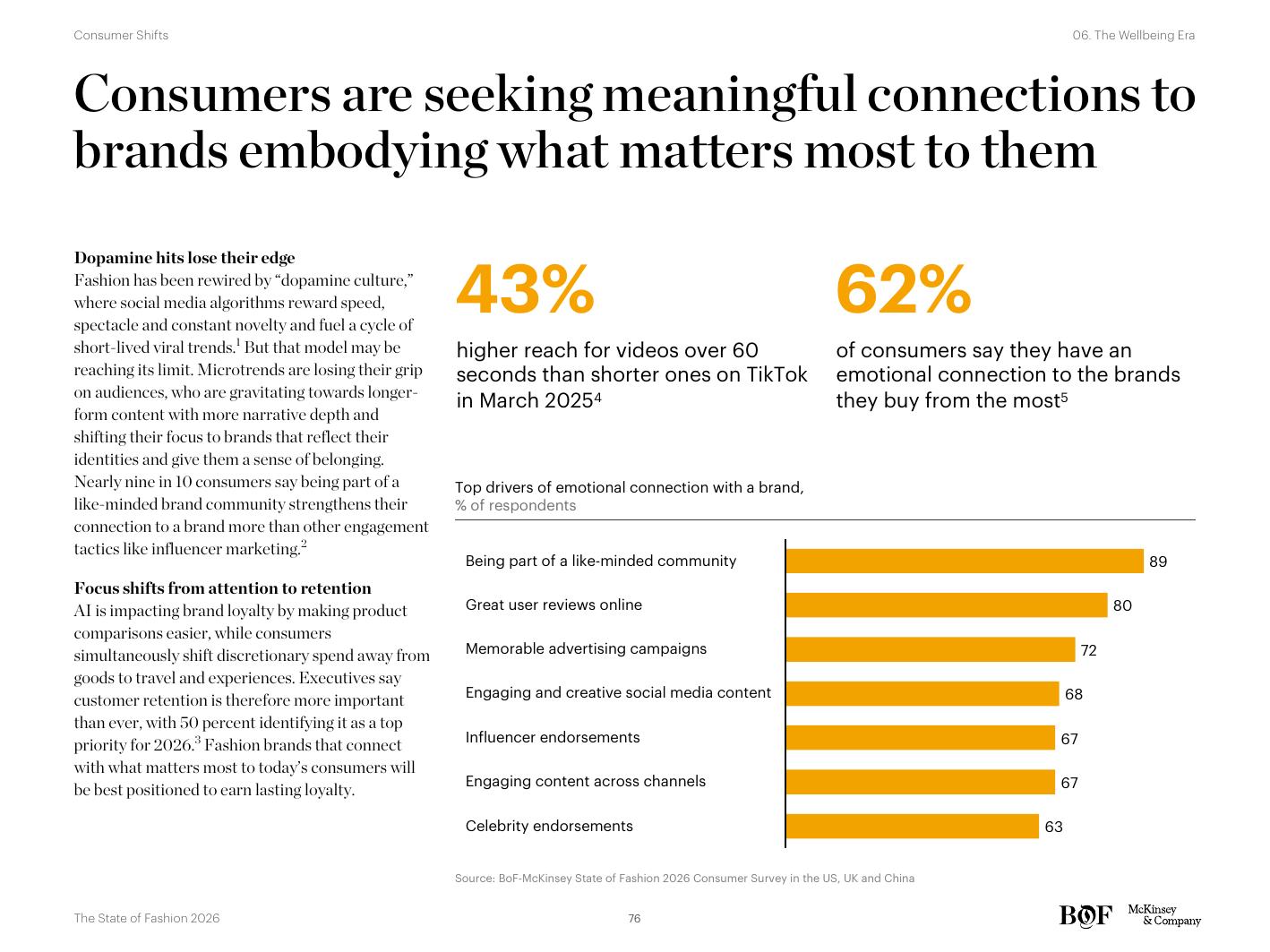

Wellbeing is becoming central to how consumers evaluate brands, including fashion brands. The report frames the shift not as a vertical category but as a lens through which brand identity, product choice, and shopping experience are increasingly judged. Consumers are seeking meaningful connections to brands that embody what matters most to them — physical health, mental health, time well spent, communities they belong to. The wellbeing movement is reshaping the identities and priorities of consumers, and fashion brands that fail to engage credibly will lose relevance.웰빙이 소비자가 패션 브랜드를 포함한 브랜드를 평가하는 방식의 중심으로 자리잡고 있다. 보고서는 이 이동을 별개의 카테고리가 아니라 ‘브랜드 정체성, 제품 선택, 쇼핑 경험이 점점 더 평가되는 렌즈’로 규정한다. 소비자들은 자신에게 가장 중요한 것 — 신체 건강, 정신 건강, 잘 쓰인 시간, 소속된 커뮤니티 — 을 체현하는 브랜드와의 의미 있는 연결을 찾고 있다. 웰빙 운동은 소비자의 정체성과 우선순위를 재편하고 있으며, 신뢰성 있게 참여하지 못하는 패션 브랜드는 관련성을 잃게 될 것이다.

As the wellbeing movement accelerates, there is a growing opportunity for fashion brands to leverage ‘third spaces’ — physical locations beyond the home and workplace where people gather, often increasingly tied to wellbeing (running clubs, fitness collectives, meditation studios, athletic communities). Brands are deepening community connections through investment in these spaces, both literally (sponsoring or operating them) and figuratively (designing product around the activities they host).웰빙 운동이 가속화되면서, 패션 브랜드들은 ‘제3의 공간(third spaces)’ — 집과 직장을 넘어 사람들이 모이는 물리적 장소, 점점 더 웰빙과 결부되는 공간 (러닝 클럽, 피트니스 콜렉티브, 명상 스튜디오, 운동 커뮤니티) — 을 활용할 기회가 커지고 있다. 브랜드들은 이러한 공간에 대한 투자 — 문자 그대로 (후원하거나 운영), 그리고 비유적으로 (그 공간이 호스팅하는 활동을 중심으로 제품 설계) — 를 통해 커뮤니티 연결을 심화시키고 있다.

Aligning with evolving consumer priorities requires a holistic transformation. The report's prescription is that brands must define how wellbeing fits into their identity today and in the years ahead — not as a marketing layer but as a strategic anchor that shapes product, retail, and partnerships.진화하는 소비자 우선순위에 부합하려면 총체적 변환이 필요하다. 보고서의 처방은 다음과 같다 — 브랜드들은 웰빙이 오늘날, 그리고 향후 수년간 자신의 정체성에 어떻게 자리 잡을 것인지를 정의해야 한다. 마케팅 레이어가 아니라, 제품·리테일·파트너십을 형성하는 전략적 앵커로서.

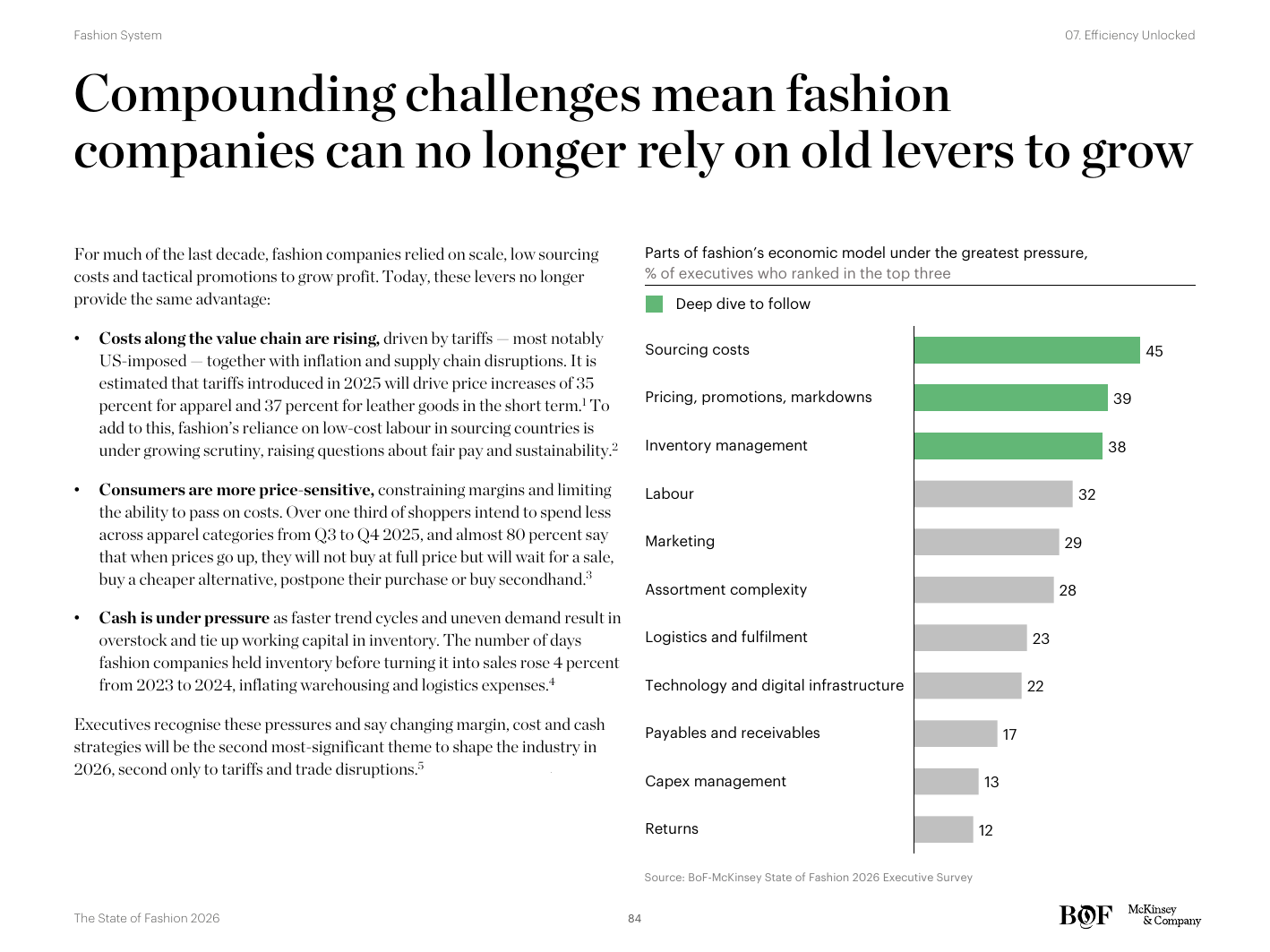

In a challenging fashion market, leaders are increasingly looking to efficiency — not new growth segments — for margin recovery. For much of the last decade, fashion companies relied on scale, low sourcing costs, and tactical promotions to support margins. Rising input costs, geopolitical tensions, and shorter trend cycles are now making those structural levers less reliable. Demand-driven strategies are gaining traction as a way to reduce inventory pressures and shift the operating model toward predictability.도전적인 패션 시장에서, 리더들은 마진 회복을 위해 새로운 성장 세그먼트가 아니라 효율로 시선을 돌리고 있다. 지난 10년 동안 패션 기업들은 마진 지탱을 위해 규모, 낮은 소싱 비용, 전술적 프로모션에 의존해 왔다. 이제 상승하는 투입 비용, 지정학적 긴장, 그리고 짧아진 트렌드 사이클이 이러한 구조적 레버를 덜 신뢰할 수 있게 만들고 있다. 재고 압박을 줄이고 운영 모델을 예측 가능성 쪽으로 옮기는 방법으로서, 수요 주도(demand-driven) 전략이 점차 채택되고 있다.

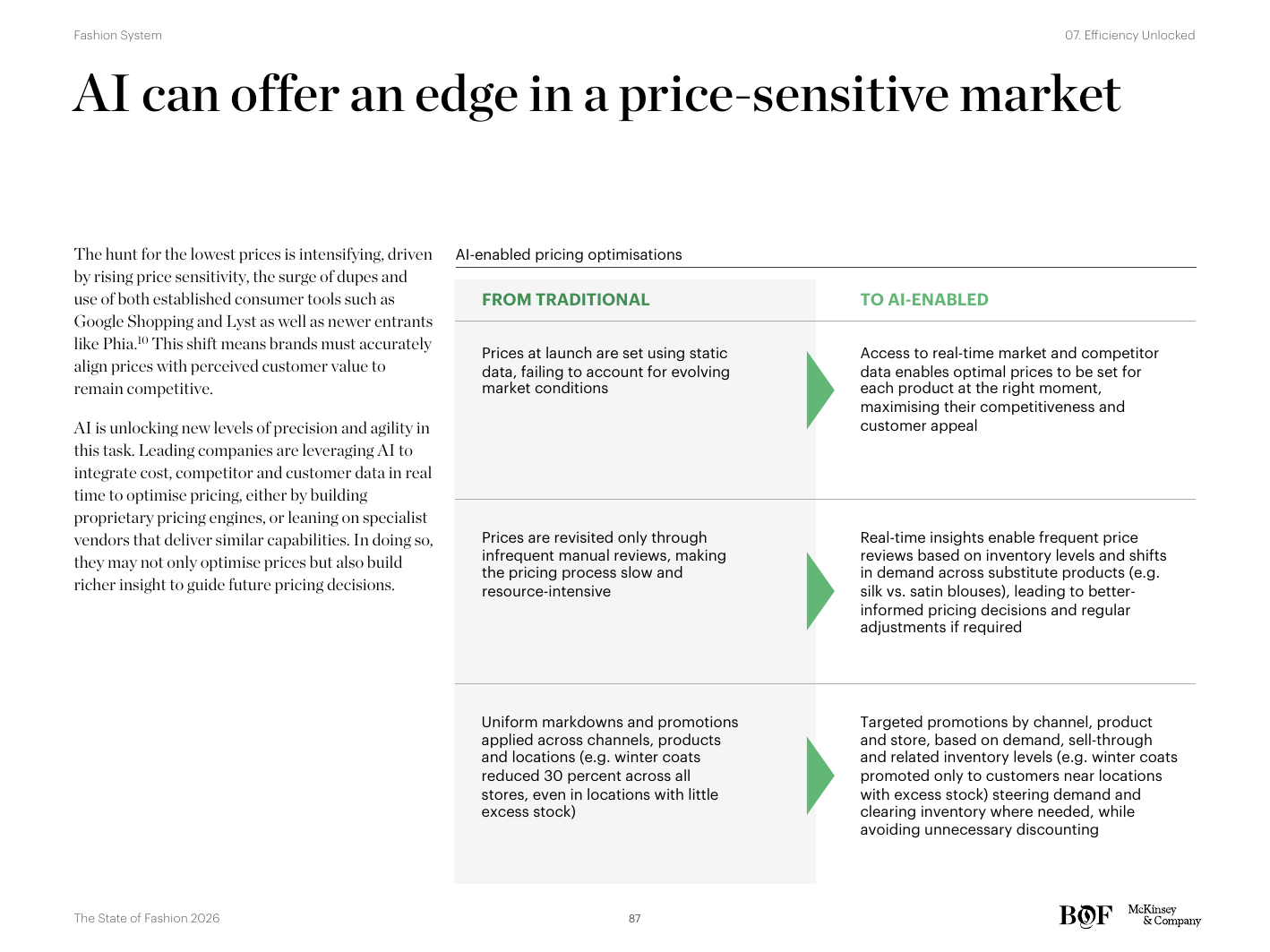

Leading companies are pioneering technology to reshape their economic model. AI offers a meaningful edge in a price-sensitive market — the hunt for the lowest customer-relevant price is intensifying, and the brands with the best demand-prediction and dynamic-pricing capability win. The report's prescription is to evaluate where margin gains can be unlocked by assessing the full company P&L — not just sourcing or store labour but the full set of structural cost lines from design through aftermarket service.선도 기업들은 자신의 경제 모델을 재편하기 위해 기술을 개척하고 있다. AI는 가격 민감 시장에서 의미 있는 우위를 제공한다 — 가장 낮은, 고객 관련성 있는 가격을 향한 사냥이 강화되고 있고, 가장 좋은 수요 예측과 동적 가격 책정 역량을 가진 브랜드가 승리한다. 보고서의 처방은 전사 P&L을 평가하여 마진 이득을 어디서 해제할 수 있는지를 식별하라는 것 — 단순히 소싱이나 매장 인건비뿐 아니라, 디자인에서 사후 서비스까지의 구조적 비용 라인 전체를 검토해야 한다.

Burberry was hit hard by luxury's slowdown. Schulman's initial diagnosis was that the brand had over-elevated — pricing had moved too far above what the core customer recognised as fair value for the actual product. His response was to reintroduce iconic products at accessible price points (notably the heritage polo) while preserving prestige-tier offerings (the £600 polo) for the customer who wants them. The discipline: protect brand authority by ensuring the customer can still find the brand at recognisable prices, while continuing to invest in design, merchandising, and marketing at the elevated end.Burberry는 럭셔리 둔화의 직격탄을 맞았다. Schulman의 초기 진단은, 브랜드가 과도하게 격상되었다는 것 — 가격이 핵심 고객이 실제 제품에 대해 인식하는 공정 가치(fair value)에서 너무 멀리 떨어졌다는 것이었다. 그의 대응은 아이코닉 제품을 접근 가능한 가격대로 재도입하는 것 (특히 헤리티지 폴로)이었고, 동시에 그것을 원하는 고객을 위해 프레스티지 가격대 상품 (600파운드 폴로)도 유지하는 것이었다. 규율은 다음과 같다: 고객이 여전히 브랜드를 인식 가능한 가격에 찾을 수 있도록 보장함으로써 브랜드 권위를 보호하고, 동시에 격상된 끝에서 디자인·머천다이징·마케팅 투자를 계속하는 것.

“We can still sell the £600 polo, but it will have to mean investing in design, merchandising, marketing. Investing in what the consumer will see.”“우리는 여전히 600파운드 폴로를 팔 수 있습니다. 그러나 그것은 곧 디자인, 머천다이징, 마케팅 — 즉 소비자가 볼 모든 것 — 에 대한 투자를 의미합니다.” — Joshua Schulman

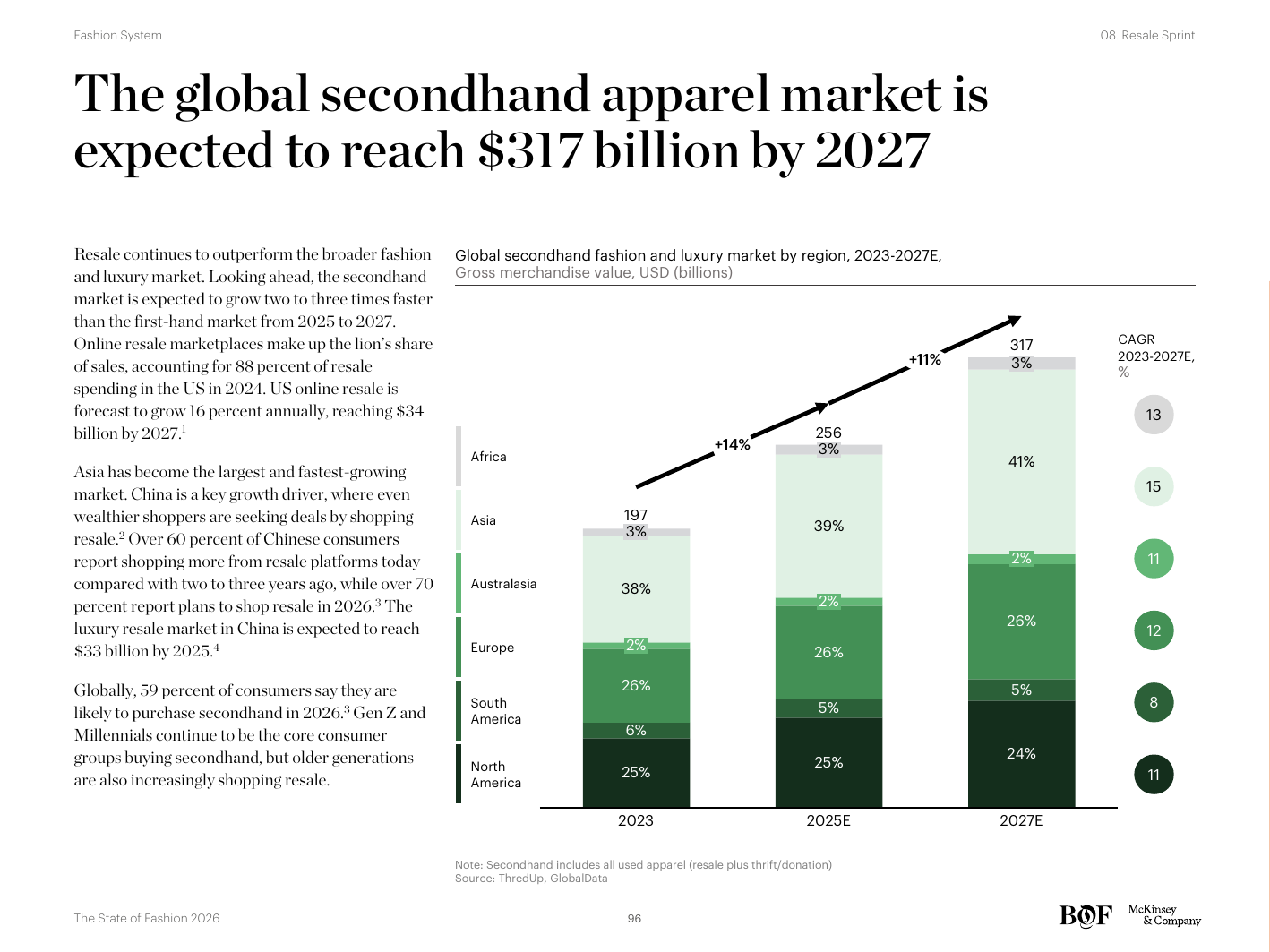

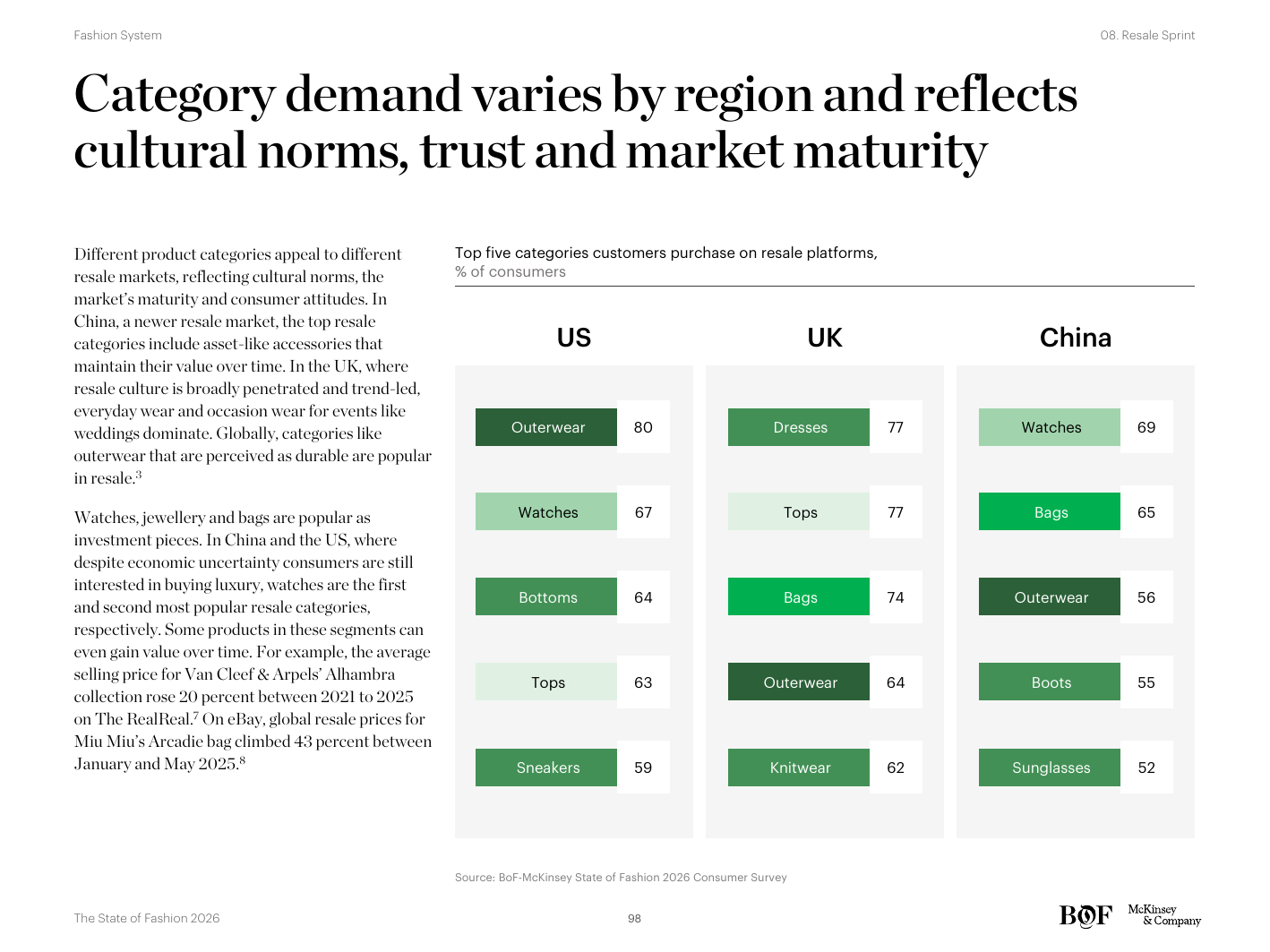

Customers are spending more on secondhand than ever, and resale continues to outperform the broader fashion and luxury market. Looking ahead, the segment is set to keep accelerating — not as a sustainability subculture but as a mainstream alternative for price-sensitive consumers and a brand-building channel for luxury houses. Affordability is the dominant driver across cohorts, though motivations vary: younger buyers cite both price and access to unique pieces, while older buyers more often cite quality and durability.고객들이 어느 때보다 많이 중고에 지출하고 있으며, 리세일은 더 넓은 패션·럭셔리 시장을 지속적으로 앞지르고 있다. 앞으로도 이 세그먼트는 계속 가속될 전망이다 — 지속가능성 하위 문화로서가 아니라, 가격 민감 소비자를 위한 주류 대안이자 럭셔리 하우스를 위한 브랜드 구축 채널로서. 코호트 전반에서 ‘감당 가능한 가격’이 핵심 동력이며, 동기는 다양하다 — 젊은 구매자는 가격과 독특한 아이템 접근을 모두 인용하고, 더 나이 든 구매자는 더 자주 품질과 내구성을 인용한다.

Category demand varies by region and reflects cultural norms, trust, and market maturity. The report highlights both pure-play resale platforms (The RealReal, Vestiaire Collective, Vinted) and branded resale initiatives (Reselfridges, brand-operated programs that capture margin while controlling the consumer experience). For brands and retailers entering resale, the report's prescription is to tailor the model to business needs — high-touch authentication, store-based take-back, online consignment, or partnership with a platform — rather than treating resale as a single template.카테고리 수요는 지역별로 다르며, 문화적 규범, 신뢰, 시장 성숙도를 반영한다. 보고서는 순수 리세일 플랫폼 (The RealReal, Vestiaire Collective, Vinted) 과 브랜드 자체 리세일 이니셔티브 (Reselfridges, 마진을 확보하면서 소비자 경험을 통제하는 브랜드 운영 프로그램) 모두를 조명한다. 리세일에 진입하는 브랜드와 리테일러를 위한 보고서의 처방: 리세일을 단일 템플릿으로 다루지 말고 비즈니스 니즈에 맞춰 모델을 조정할 것 — 하이터치 진위 확인, 매장 기반 회수, 온라인 위탁, 또는 플랫폼과의 파트너십.

By 2026, resale should be viewed as a commercial lever as much as a brand play. Given growing demand and increased price sensitivity, a resale presence is increasingly seen as table stakes for both luxury and mass premium brands.2026년에 리세일은 브랜드 플레이만큼이나 상업적 레버로 봐야 한다. 늘어나는 수요와 가격 민감도 증가를 고려할 때, 리세일 존재감은 점점 럭셔리와 매스 프리미엄 브랜드 모두에게 ‘테이블 스테이크’로 인식되고 있다.

For most of its 14 years in business, The RealReal was another money-losing online resale operator. Levesque's turnaround thesis is built on AI applied to authentication (faster, more consistent, lower unit cost), data-driven pricing that handles the full long tail of categories rather than only high-value items, and physical-store integration that becomes a discovery channel for new consigners. The lesson she draws for the broader industry: resale at scale is an operating-system problem, not an inventory-acquisition problem.사업 14년 중 대부분의 기간 동안 The RealReal은 또 하나의 적자 온라인 리세일 운영자였다. Levesque의 턴어라운드 명제는 다음 위에 구축된다: 진위 확인에 적용된 AI (더 빠르고, 더 일관되고, 단위 비용이 더 낮음), 고가 아이템만이 아니라 카테고리의 긴 꼬리 전체를 다루는 데이터 주도 가격 책정, 그리고 신규 위탁자(consigner)를 위한 발견 채널이 되는 오프라인 매장 통합. 더 넓은 산업을 위해 그녀가 끌어내는 교훈: 규모를 갖춘 리세일은 재고 획득 문제가 아니라 운영체제(operating system) 문제다.

On consumer behavior: Levesque emphasises that customers prize being able to consign everything — not just one bag from one closet, but the full range of categories. The single-category specialist resale platforms struggle precisely because the consigner's relationship is with a closet, not with a category. The RealReal's competitive advantage is the ability to receive anything credibly authentic and find a buyer for it.소비자 행동에 관해, Levesque는 고객들이 ‘모든 것을 위탁할 수 있는 능력’을 가치 있게 여긴다고 강조한다 — 한 옷장의 한 가방이 아니라, 전체 카테고리의 범위. 단일 카테고리 전문 리세일 플랫폼들이 고전하는 이유는 정확히 이것이다 — 위탁자의 관계는 한 카테고리가 아니라 옷장 전체와 맺어진다. The RealReal의 경쟁 우위는 진정성 있게 진품으로 인증할 수 있는 모든 것을 받아서 구매자를 찾아 줄 수 있는 능력이다.

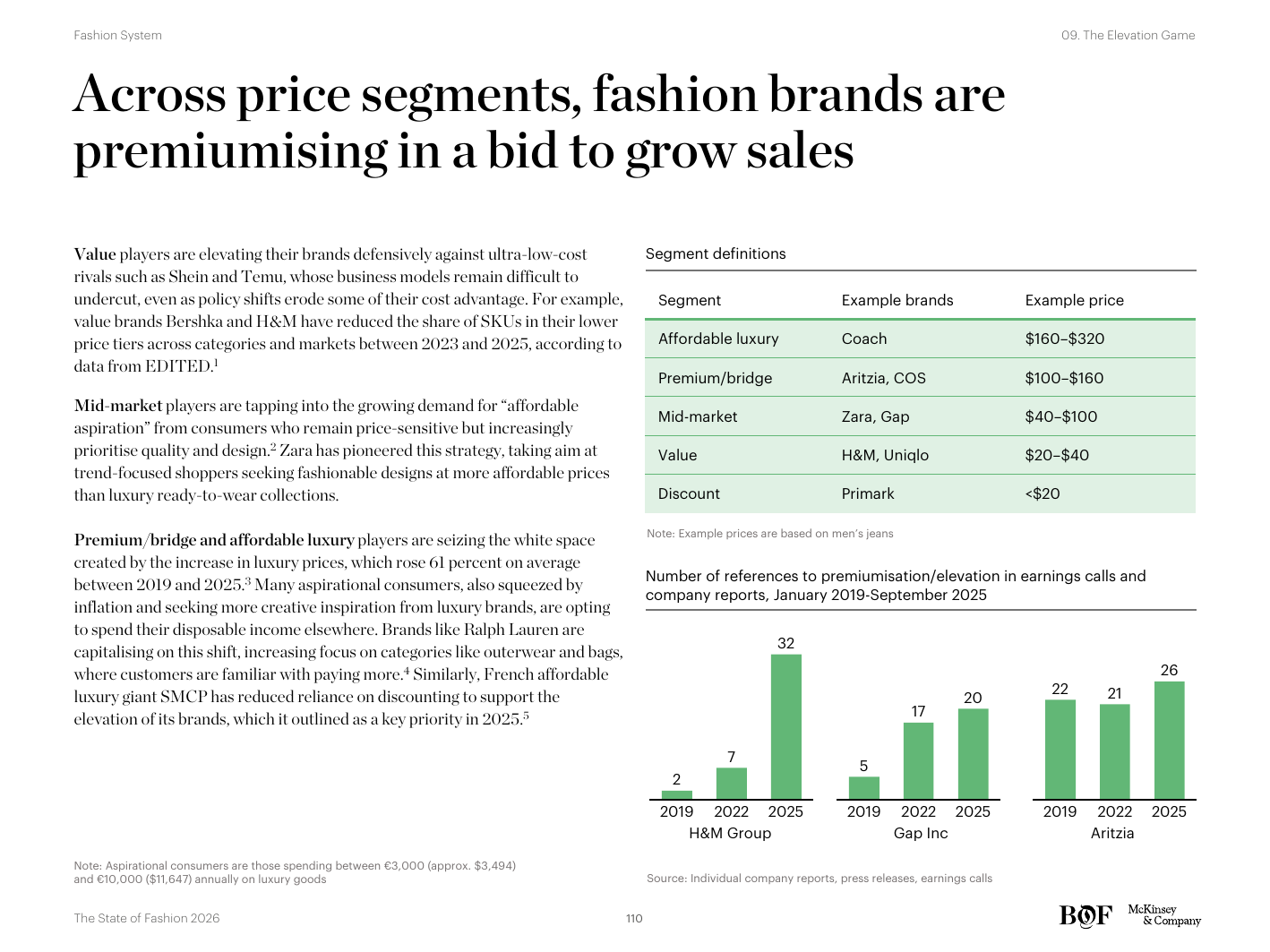

From the value segment up to affordable luxury, fashion brands are premiumising in a coordinated bid to grow sales without expanding unit volume. Value players are introducing higher-quality lines at the top of their assortment. Mid-market brands are repositioning toward affordable luxury. Affordable-luxury brands are pushing into prestige territory. Brand elevation depends on three pillars: price, product, and brand experience. Each must move in coordinated fashion — raising prices without commensurate quality improvement is the fastest way to alienate the core customer.밸류 세그먼트에서 어포더블 럭셔리에 이르기까지, 패션 브랜드들은 단위 볼륨 확장 없이 매출을 늘리기 위한 협조된 시도로 프리미엄화 중이다. 밸류 플레이어들은 구색의 상단에 더 높은 품질의 라인을 도입한다. 미드마켓 브랜드들은 어포더블 럭셔리로 재포지셔닝한다. 어포더블 럭셔리 브랜드들은 프레스티지 영역으로 밀고 들어간다. 브랜드 격상은 세 가지 기둥에 달려 있다 — 가격, 제품, 그리고 브랜드 경험. 셋은 협조된 방식으로 움직여야 한다 — 동등한 품질 개선 없이 가격을 올리는 것은 핵심 고객을 가장 빠르게 이탈시키는 길이다.

Higher prices demand superior quality and refreshed designs. Customers are expected to become increasingly discerning. The case study features Zara's August 2025 reopening of its Manchester flagship under a new concept, designed to express the elevation thesis spatially and in service. The report's prescription is to practise discipline in rolling out elevation strategies — build the price ladder gradually, refresh design and store experience before raising prices, and segment the brand cleanly between elevated and core lines rather than letting them blur into a single confused proposition.더 높은 가격은 우월한 품질과 새로워진 디자인을 요구한다. 고객들은 점점 더 까다로워질 것으로 예상된다. 본 보고서는 2025년 8월 Zara의 맨체스터 플래그십이 새로운 컨셉으로 재오픈한 사례 — 격상 명제를 공간과 서비스로 표현한 사례 — 를 소개한다. 보고서의 처방: 격상 전략 전개에 규율을 발휘할 것 — 가격 사다리를 점진적으로 구축하고, 가격 인상 전에 디자인과 매장 경험을 새로 하고, 격상 라인과 핵심 라인을 단일한 혼란스러운 제안으로 흐려지게 하지 말고 깔끔하게 세분화할 것.

COS launched in 2007 inside the H&M group to serve an older customer than H&M proper. The brand was always designed to be a single coherent design voice, and Herrmann's discomfort with the word ‘elevation’ reflects a deeper view: the brands that win in 2026 will be the ones that have been quietly disciplined about price-product-experience consistency for years, not the ones running an elevation sprint right now. The pricing architecture matters because value perception is so important to the customer.COS는 2007년 H&M 그룹 내에서, H&M 본 브랜드보다 더 나이 든 고객을 위해 출범했다. 브랜드는 처음부터 ‘단일하고 일관된 디자인 보이스’로 설계되었으며, ‘격상’이라는 단어에 대한 Herrmann의 불편함은 더 깊은 관점을 반영한다 — 2026년에 승리하는 브랜드는 지금 격상 스프린트를 뛰는 브랜드가 아니라, 수년 동안 가격-제품-경험의 일관성에 대해 조용히 규율 있게 임해 온 브랜드일 것이다. 고객에게 가치 인식이 그토록 중요하기에, 가격 아키텍처가 핵심이다.

“Value is so important.” — the through-line of the COS conversation.“가치(value)는 매우 중요합니다.” — COS 대화 전체를 관통하는 한 줄.

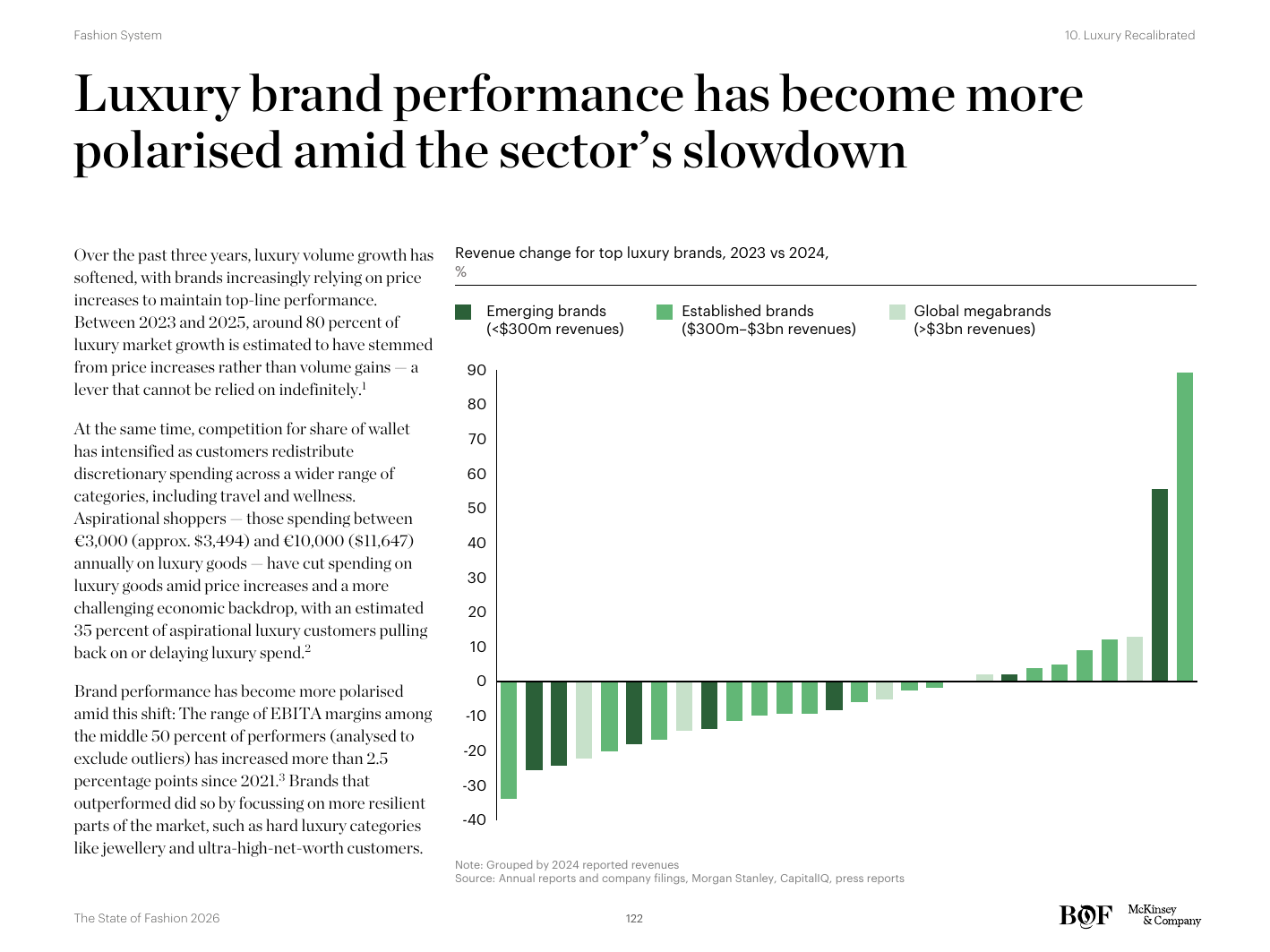

The luxury slowdown is prompting brands to rethink their playbook. Over the past three years, luxury brand performance has become more polarised — a handful of brands continue to outperform sharply while many others have contracted. The report attributes the polarisation to over-elevation by the laggards (price increases that outpaced product and experience improvements) and to over-reliance on Chinese demand that has not recovered to pre-pandemic levels. The recalibration agenda has three pillars: creative reboots to reignite customer demand, rebuilding customer trust through clearer value-for-money, and using insight and analytics to bring discipline to product creation without sacrificing creative authority.럭셔리 둔화가 브랜드들로 하여금 플레이북을 재고하게 만들고 있다. 지난 3년간 럭셔리 브랜드 실적은 점점 더 양극화되어 왔다 — 소수의 브랜드는 큰 폭으로 아웃퍼폼하는 반면, 다수의 브랜드는 위축되었다. 보고서는 이 양극화의 원인으로 둔화된 브랜드들의 과도한 격상 (제품과 경험 개선을 앞서간 가격 인상) 과 팬데믹 이전 수준으로 회복되지 않은 중국 수요에 대한 과도한 의존을 지목한다. 재조정 의제는 세 기둥에 달려 있다 — 고객 수요를 다시 점화하기 위한 크리에이티브 리부트, 더 명확한 ‘가격 대비 가치’를 통한 고객 신뢰 재구축, 그리고 크리에이티브 권위를 희생하지 않으면서 제품 창조에 규율을 부여하기 위한 인사이트와 분석의 활용.

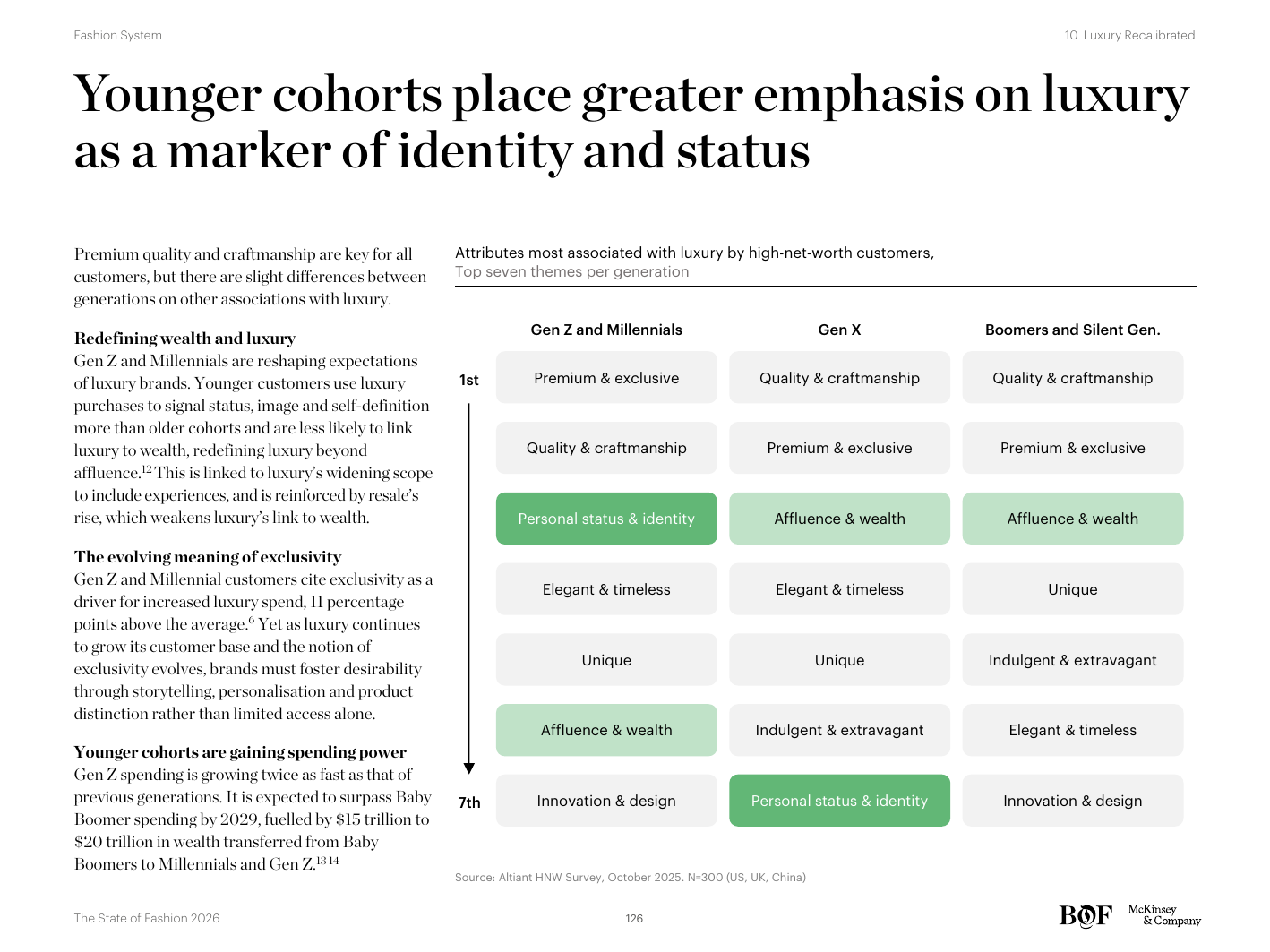

Regional differences in purchase drivers reveal unique formulas to capture high spenders. The report's segmentation shows that younger cohorts place greater emphasis on luxury as a marker of identity and status, while older cohorts place greater weight on craftsmanship and durability. The brands that win across generations balance both vocabularies. The luxury creative refresh wave underway in 2025 (with multiple high-profile designer transitions) is, in this framing, the visible top layer of a deeper recalibration that includes pricing discipline, distribution rationalisation, and a more systematic use of customer data.지역별 구매 동력 차이는 고액 지출자를 잡기 위한 고유의 공식을 드러낸다. 보고서의 세분화는 다음을 보여 준다 — 젊은 코호트는 정체성과 지위의 표식으로서의 럭셔리에 더 큰 비중을 두고, 더 나이 든 코호트는 장인 정신(craftsmanship)과 내구성에 더 큰 비중을 둔다. 세대를 가로질러 승리하는 브랜드는 두 어휘를 모두 균형 잡는다. 2025년 진행 중인 럭셔리 크리에이티브 리프레시 물결 (다수의 주목받는 디자이너 전환을 포함) 은, 이 프레임 안에서 가격 규율, 유통 합리화, 그리고 더 체계적인 고객 데이터 활용을 포함하는 더 깊은 재조정의 가시적 상층(top layer)이다.

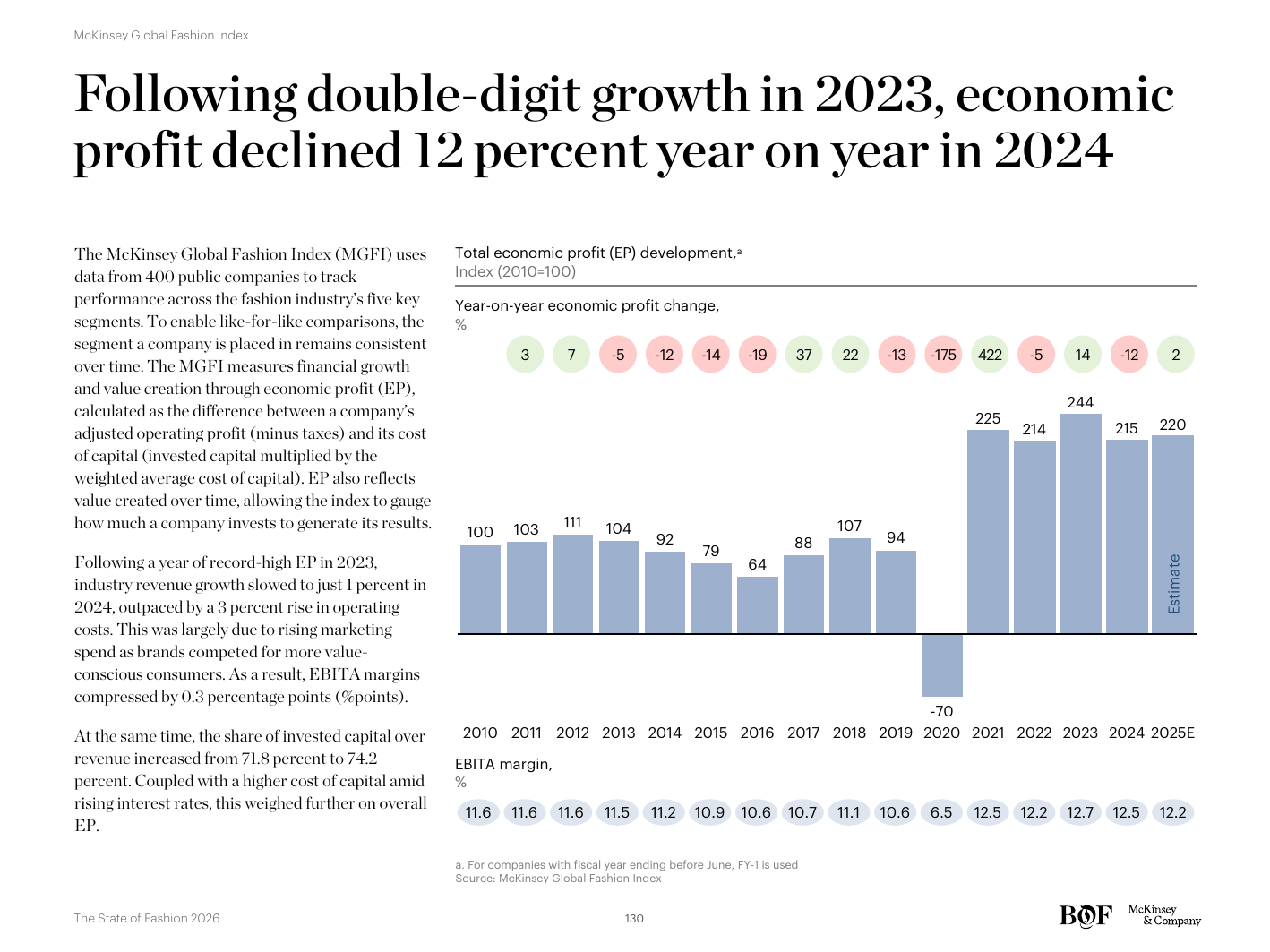

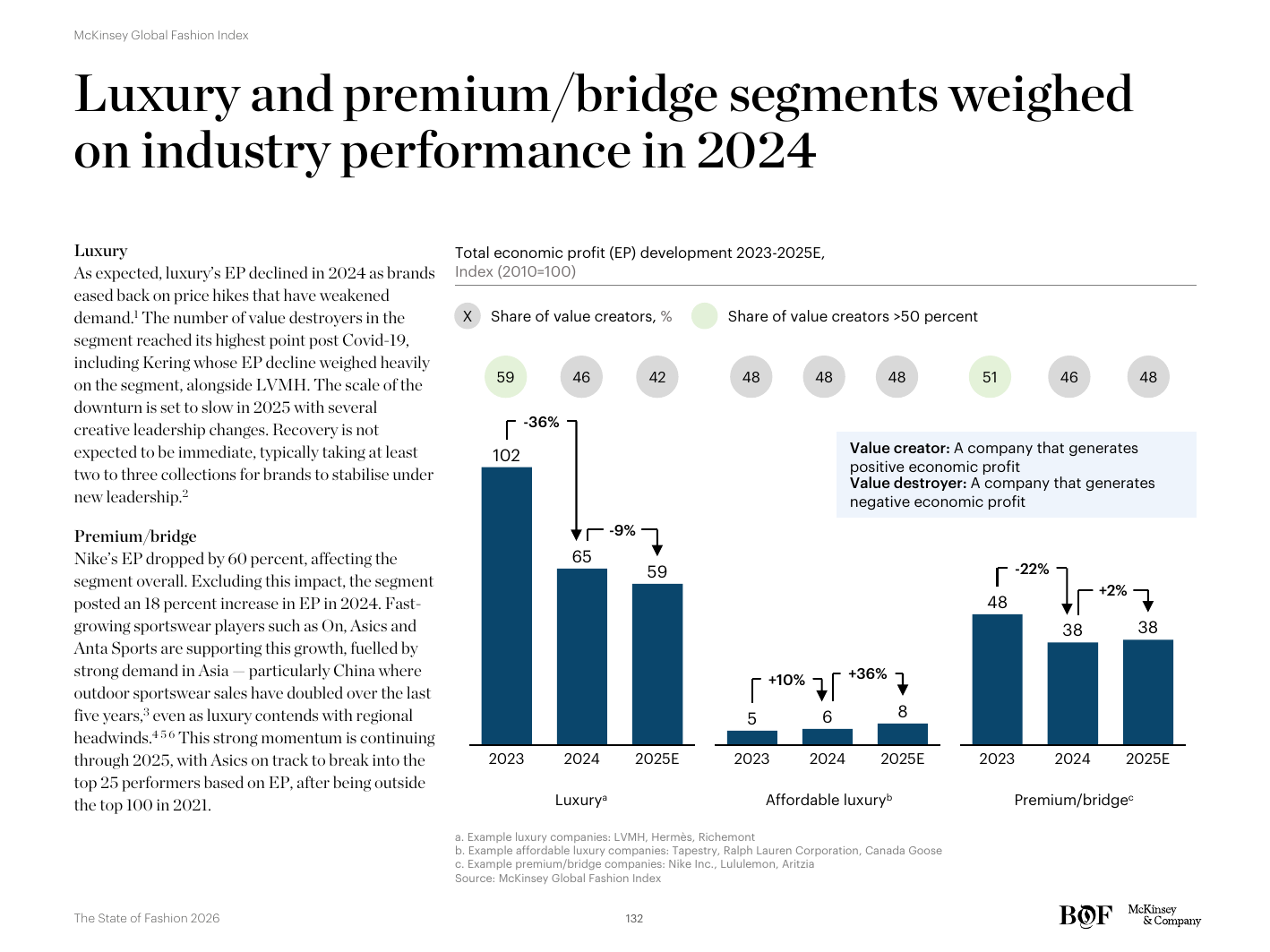

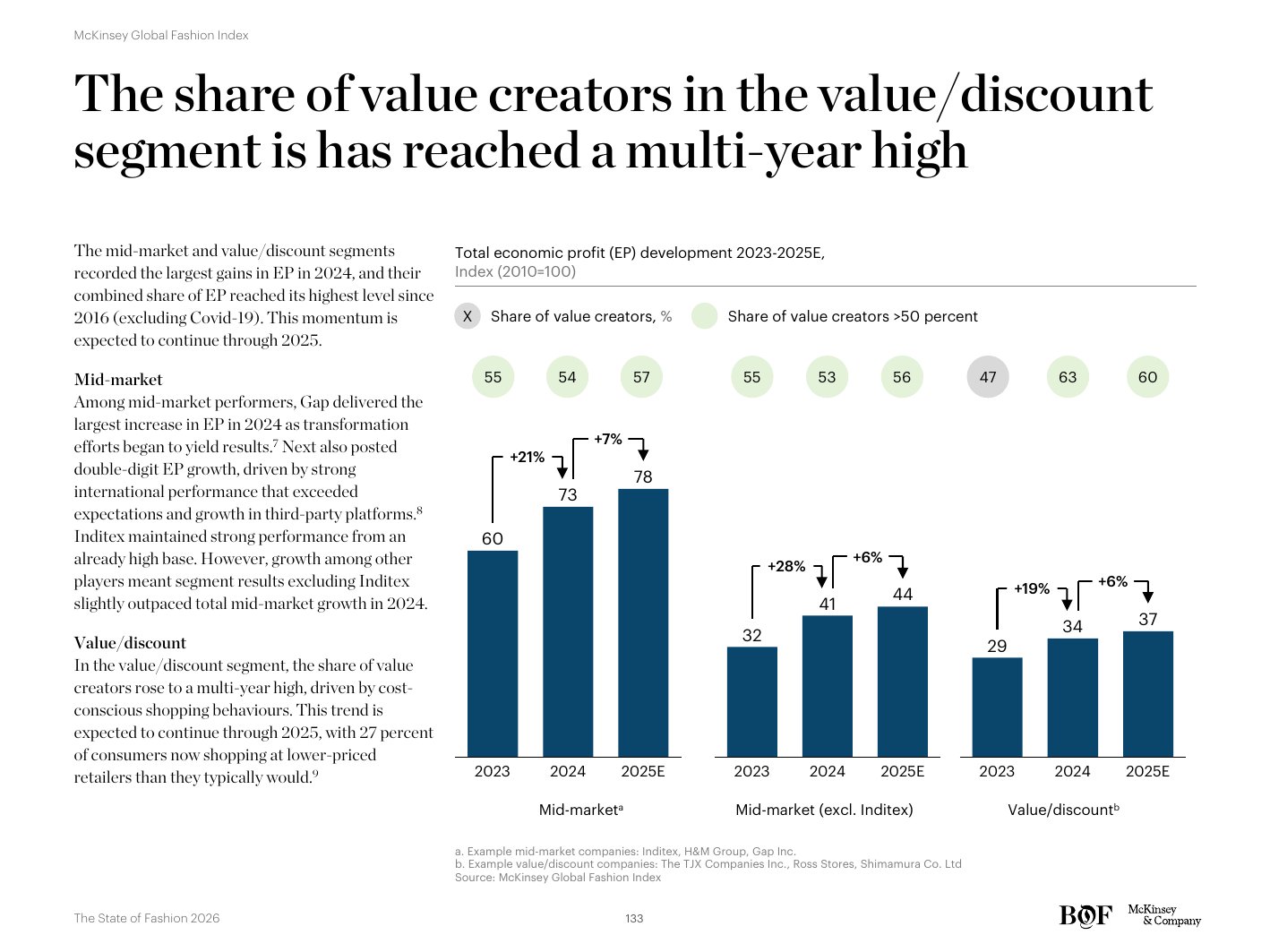

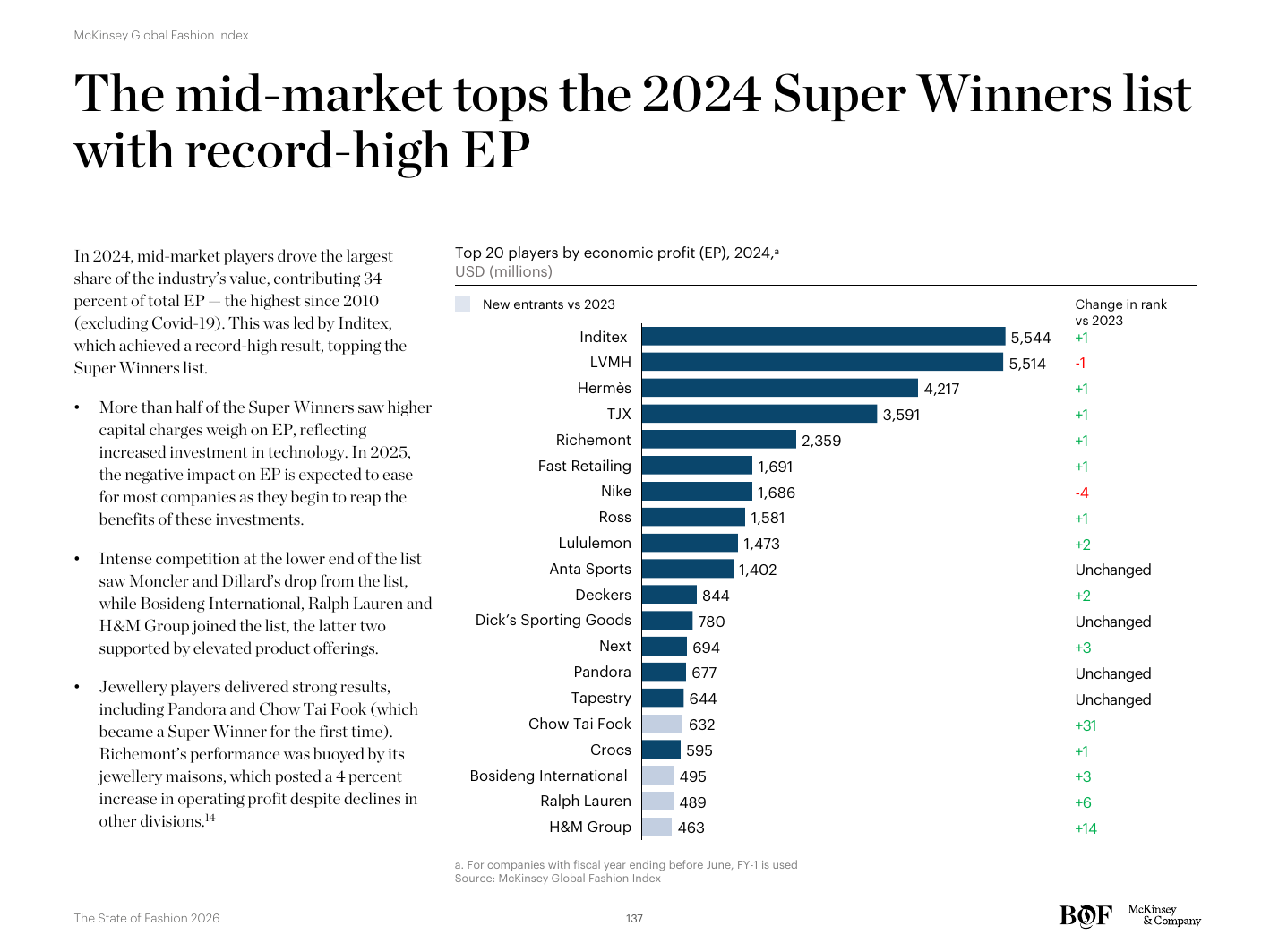

After a record 2023, the fashion industry's economic profit declined 12% year-on-year in 2024 according to the McKinsey Global Fashion Index. Despite the slowdown, the industry remains structurally stronger than its pre-pandemic baseline. Luxury's EP declined as brands eased back on the price hikes that had powered 2022–2023 outperformance — a predictable normalisation after an unusually sharp pricing wave. The mid-market and value/discount segments recorded the largest EP gains in 2024, and a higher share of value/discount players combined margin and sales growth versus other segments.기록적인 2023년 이후, 패션 산업의 경제적 이익(EP)은 McKinsey Global Fashion Index 기준 2024년 전년 대비 12% 감소했다. 둔화에도 불구하고 산업은 팬데믹 이전 기준선보다 구조적으로 더 강한 상태를 유지한다. 럭셔리의 EP는 2022–2023년 아웃퍼폼을 견인했던 가격 인상에서 브랜드들이 한발 물러서면서 감소했다 — 비정상적으로 가팔랐던 가격 파동 이후의 예측 가능한 정상화. 미드마켓과 밸류·디스카운트 세그먼트는 2024년 가장 큰 EP 이득을 기록했고, 밸류·디스카운트 플레이어의 더 높은 비중이 다른 세그먼트 대비 마진과 매출 성장을 동시에 달성했다.

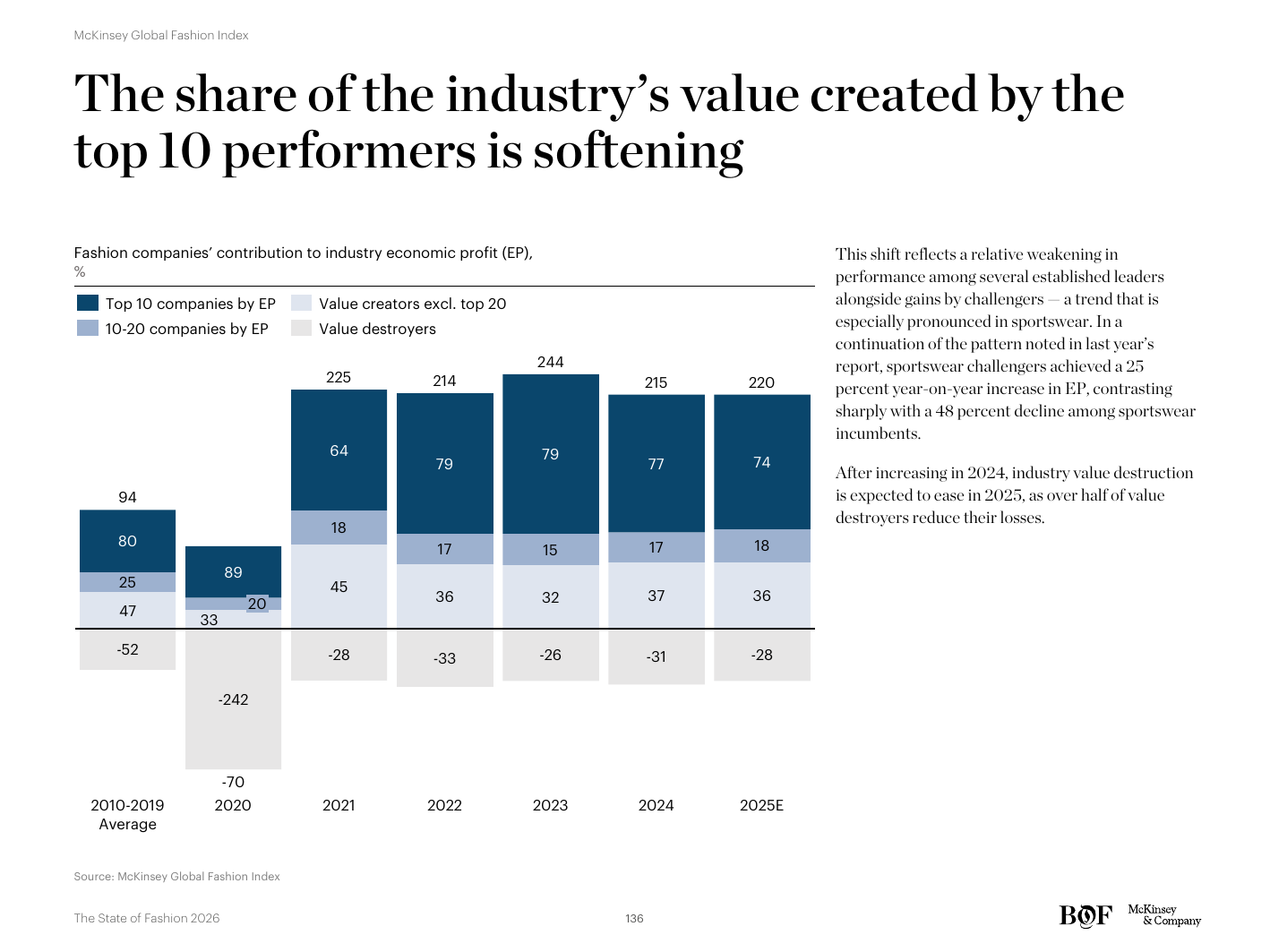

The share of the industry's value created by the top 10 performers is softening — a shift away from the ‘winner-take-most’ concentration of recent years. The mid-market tops the 2024 Super Winners list with record-high EP from a single segment. Looking ahead, a modest uptick in valuations signals cautious optimism from investors. The story of 2024 in the MGFI: luxury normalisation, mid-market and value/discount strength, and a gentle broadening of where industry profit accrues.산업 가치 중 상위 10개 실적자들의 점유 비중이 약화되고 있다 — 최근 수년간의 ‘승자독식’ 집중에서 멀어지는 이동. 미드마켓이 2024년 ‘슈퍼 위너스(Super Winners)’ 리스트의 정상을 차지하며, 단일 세그먼트에서 기록적 EP를 달성했다. 앞을 내다보면 밸류에이션의 완만한 상승은 투자자들의 신중한 낙관을 시사한다. MGFI 안에서의 2024년 이야기: 럭셔리의 정상화, 미드마켓과 밸류·디스카운트의 강세, 그리고 산업 이익이 축적되는 위치의 온건한 확장.