Die Bibliothek · 012 · Industry ReportDie Bibliothek · 012 · 산업 보고서

Once the darling of the consumer goods market, the $441 billion global beauty industry is showing signs of cooling. For years, a seemingly limitless appetite for newness in beauty fuelled robust volume and even greater pricing growth — from 2022 to 2024, the sector grew 7 percent annually. Now, geopolitical and economic uncertainty, along with market saturation, are threatening this momentum. A once-clear formula for success is now a challenging puzzle to solve.한때 소비재 시장의 ‘총아’로 군림했던 4,410억 달러 규모의 글로벌 뷰티 산업이 둔화의 신호를 보이고 있습니다. 지난 수년간, 끝없어 보이던 ‘새로움’에 대한 소비자의 욕구는 견조한 물량(volume) 성장과 그를 웃도는 가격(pricing) 성장을 모두 견인했습니다 — 그 결과 2022년부터 2024년까지 산업은 연평균 7%의 성장을 기록했습니다. 그러나 이제는 지정학적·경제적 불확실성과 시장 포화가 이 성장 동력을 위협하고 있습니다. 한때 명확했던 성공 공식은, 이제 풀어내기 까다로운 퍼즐로 변모했습니다.

Of course, dynamism in the sector persists in pockets, and the market is still growing. We expect the global beauty industry to grow 5 percent annually through 2030. But consumers are broadening their understanding of ‘beauty’ beyond core categories to include wellness, personal care and aesthetic treatments — and they are increasingly value-conscious, sceptical of hype and laser-focused on whether products deliver.물론 산업의 역동성은 일부 영역에서 지속되고 있으며, 시장 자체는 여전히 성장 중입니다. 본 보고서는 2030년까지 글로벌 뷰티 산업이 연 5% 수준의 성장을 이어갈 것으로 전망합니다. 다만 소비자들은 ‘뷰티’의 정의를 핵심 카테고리를 넘어 웰니스, 퍼스널 케어, 미용 시술 영역까지 확장하고 있으며 — 동시에 더 가치 지향적이 되었고, 과대 광고(hype)에 회의적이며, ‘제품이 실제로 효과를 내는가’에 집요하게 집중하고 있습니다.

So how are beauty executives responding to all the change? Seventy-five percent of executives in our survey expect consumer scrutiny on perceived value to be the biggest theme shaping the industry. Fifty-four percent say uncertain consumer appetite or restricted spending is the greatest risk to the market's growth going forward. As the puzzle shifts, beauty players should recalibrate and sharpen their value propositions to stand out.그렇다면 뷰티 기업의 경영진은 이 변화에 어떻게 대응하고 있는가? 본 조사 응답자의 75%는 ‘소비자의 가치(밸류) 검증 강화’를 향후 산업을 좌우할 가장 큰 테마로 꼽았습니다. 54%는 불확실한 소비 심리 혹은 제약된 소비 지출을 가장 큰 성장 리스크로 지목했습니다. 퍼즐의 형태가 바뀐 만큼, 뷰티 기업들 또한 자신만의 가치 제안(value proposition)을 재조정하고, 보다 날카롭게 다듬어 차별화를 도모해야 할 시점입니다.

In the US, the beauty market is still an attractive play, given its size and strong market fundamentals — but political and economic volatility clouds forecasts. In markets like the Middle East and Latin America, where wealth is growing, there are opportunities for global brands — but they will face strong competition from local players. Further east, we expect the Chinese beauty market to rebound in the mid term, though growth is unlikely to reach pre-pandemic rates. Europe will grow in line with global trends, but economic challenges may dampen volume growth.미국은 시장 규모와 견조한 펀더멘털을 고려할 때 여전히 매력적인 시장이지만, 정치적·경제적 변동성이 전망의 안개를 짙게 만듭니다. 부(富)가 빠르게 성장 중인 중동과 라틴아메리카에서는 글로벌 브랜드에 새로운 기회가 열려 있으나, 강력한 로컬 사업자들과의 경쟁이 불가피합니다. 동쪽으로는, 중국 뷰티 시장이 중기적으로 회복할 것으로 전망되지만, 팬데믹 이전 수준의 성장률에는 미치지 못할 것으로 보입니다. 유럽은 글로벌 추세와 보조를 맞추겠으나, 경제적 부담이 물량 성장을 제약할 수 있습니다.

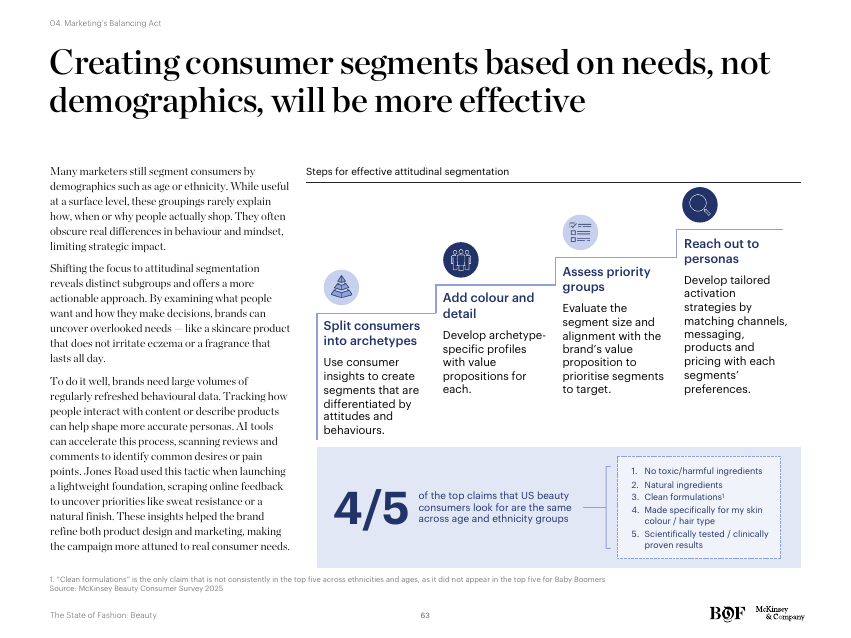

The world is changing and so are beauty consumers' preferences. Shifting demographics have splintered traditional customer profiles. Yesterday's segments defined purely by demographic differences no longer hold — attitudinal consumer insights and hyper-localisation are needed to win.세상이 변하고 있는 만큼, 뷰티 소비자의 선호 또한 변하고 있습니다. 인구 구조의 이동은 기존의 고객 프로파일을 잘게 쪼개 놓았습니다. 단순한 인구통계학적 차이로 정의되던 어제의 세그먼트는 더 이상 유효하지 않습니다 — 이제는 ‘태도(attitude) 기반 소비자 인사이트’와 ‘하이퍼 로컬라이제이션(hyper-localisation)’이 승부의 관건입니다.

Then, there is the question of value. Strong uptake in beauty spend plus higher inflation has pushed shoppers to pay closer attention to whether products perform. Consumers may still consider beauty to be an affordable discretionary item, but that doesn't mean the industry should take the ‘lipstick effect’ for granted. Products in all categories and across all price tiers must demonstrate their prices are justified: 83 percent of consumers feel haircare is affordable, but that figure drops to 67 percent for fragrances. To cut through the noise, beauty labels will need to increase their investments in R&D, emphasise their unique value drivers in marketing campaigns, and create entry-level price points for aspirational and the most discerning beauty shoppers.다음은 ‘가치(value)’의 문제입니다. 강한 뷰티 소비 증가에 더해진 인플레이션은, 소비자들로 하여금 ‘이 제품이 실제로 성능을 내는가’에 더 집요하게 주목하도록 만들었습니다. 소비자들이 여전히 뷰티를 ‘감당 가능한 재량적 사치’로 인식하더라도, 산업이 ‘립스틱 효과’를 당연시할 수 있는 시기는 끝났습니다. 모든 카테고리, 모든 가격대의 제품이 ‘이 가격이 정당하다’는 점을 증명해야 합니다: 소비자의 83%는 헤어케어를 ‘감당할 만하다’고 답한 반면, 향수에서는 그 비율이 67%로 떨어집니다. 시장의 잡음을 뚫고 나가기 위해, 뷰티 브랜드들은 R&D 투자를 확대하고, 마케팅에서 고유의 가치 드라이버를 강조하며, 동경(aspirational) 및 까다로운 고객층을 위한 진입가(entry-level) 가격대를 함께 마련해야 합니다.

Purchase considerations are also evolving. Prominent, public-facing beauty founders were a marketing accelerator for many upstart brands, helping to push them to greater heights. Today, public-facing founders are among the lowest consumer consideration factors. While famous founders can still build brand awareness, a brand's staying power depends on much more. Beauty labels that previously hinged their ethos on specific demographic identities or wholly emphasised sustainability may no longer find success with these branding strategies. Instead, shoppers are focused on product efficacy and a shared aesthetic point of view.구매 고려 요인도 진화하고 있습니다. 한때 공개적으로 활동하는 창업자(founder)의 존재감은 신생 브랜드들에게 강력한 마케팅 가속 장치였고, 많은 브랜드를 정상의 자리로 밀어 올렸습니다. 그러나 오늘날, 공개적으로 활동하는 창업자의 존재감은 소비자 구매 고려 요인 중 가장 낮은 항목으로 분류됩니다. 유명 창업자는 여전히 브랜드 인지도를 만들 수는 있겠지만, 브랜드의 지속력은 그 이상의 무엇에 달려 있습니다. 과거에 특정 인구 집단의 정체성에 자신의 윤리(ethos)를 결부시키거나, 지속가능성만을 전면에 내세웠던 브랜드들은, 이러한 브랜딩 전략만으로는 더 이상 성공하기 어렵습니다. 소비자들은 이제 ‘제품 효능(efficacy)’과 ‘공유 가능한 미학적 관점(aesthetic point of view)’에 집중하고 있습니다.

Two of the most important commercial functions for beauty companies — marketing and retail — are undergoing a reckoning of their own. An overreliance on paid marketing has saturated digital channels while influencers' sway is also waning. Brand marketing can help rebalance the scales, but only if beauty players have an ownable, original story to tell.뷰티 기업의 가장 중요한 두 가지 상업 기능 — 마케팅과 리테일 — 이 동시에 청산기를 맞고 있습니다. 페이드(paid) 마케팅에 대한 과도한 의존은 디지털 채널을 포화 상태로 몰아넣었고, 인플루언서의 영향력 또한 약화되고 있습니다. 브랜드 마케팅이 다시 저울의 균형을 잡아 줄 수 있지만, 이는 오직 자신만이 할 수 있는 독창적인 이야기(ownable, original story)를 가진 브랜드에 한합니다.

Consumers still prefer brick-and-mortar stores for discovery and purchase, but e-commerce, and specifically marketplaces, have become a go-to destination for shopping and replenishment, thanks to widespread discounting and the convenience of ultra-fast shipping. For both brands and retailers, some of these practices may dilute brand positioning or margins. Instead of trying to solely compete on speed or promotions, beauty executives should focus on creating a compelling shopping experience that addresses the needs of their target customers. Technology-driven tools such as AI-led agentic commerce can also yield gains, augmenting the online shopping experience by autonomously carrying out tasks for customers and even helping them to make purchases.소비자들은 발견(discovery)과 구매에서 여전히 오프라인 매장을 선호하지만, 광범위한 할인과 초고속 배송의 편의성에 힘입어 이커머스 — 특히 마켓플레이스 — 가 쇼핑과 재구매(replenishment)의 주요 채널로 부상했습니다. 브랜드와 리테일러 모두에게, 이러한 관행 중 일부는 브랜드 포지셔닝이나 마진을 희석시킬 수 있습니다. 따라서 단순히 속도나 프로모션만으로 경쟁하기보다, 자사의 타깃 고객의 니즈에 맞춘 매력적인 쇼핑 경험을 설계하는 데 집중해야 합니다. 또한 AI 기반의 ‘에이전틱 커머스(agentic commerce)’와 같은 기술 도구는, 고객을 위해 자율적으로 업무를 수행하고 구매까지 보조하면서, 온라인 쇼핑 경험을 한층 증강시킬 수 있습니다.

While only 10 percent of surveyed executives are using AI regularly today, 60 percent are in an exploratory phase. More robust AI adoption — including in research and development, quality control, social listening and marketing personalisation — could unlock more profitable growth. However, when used in any consumer-facing capacity, caution should be taken so as not to erode customer trust.현재 본 조사 응답자 중 정기적으로 AI를 활용한다고 답한 임원은 10%에 불과하나, 60%는 탐색 단계에 있습니다. R&D, 품질 관리, 소셜 리스닝, 마케팅 개인화 등 더 견고한 AI 도입은 한층 수익성 있는 성장의 문을 열 수 있습니다. 다만 소비자 접점(consumer-facing) 영역에 활용할 때는, 고객 신뢰를 훼손하지 않도록 신중함이 요구됩니다.

The beauty industry will maintain its allure for both investors and consumers, but the era of more-is-more consumption has ceded ground to a new focus on value, differentiation and individuality. Addressing these factors is critical to solving the puzzle at hand.뷰티 산업은 투자자와 소비자 모두에게 매력을 유지하겠지만, ‘더 많이, 더 많이’의 소비 시대는 이제 가치(value), 차별화(differentiation), 그리고 개별성(individuality)에 대한 새로운 집중에 자리를 내주었습니다. 이 세 요소에 대한 해법이, 지금 우리가 맞닥뜨린 퍼즐을 푸는 핵심입니다.

— Priya Rao, The Business of Beauty Executive Editor, The Business of Fashion

— Kristi Weaver, Global Beauty, Personal Care and Wellness Leader, McKinsey & Company— Priya Rao, The Business of Beauty 편집장, The Business of Fashion

— Kristi Weaver, Global Beauty, Personal Care and Wellness 리더, McKinsey & Company

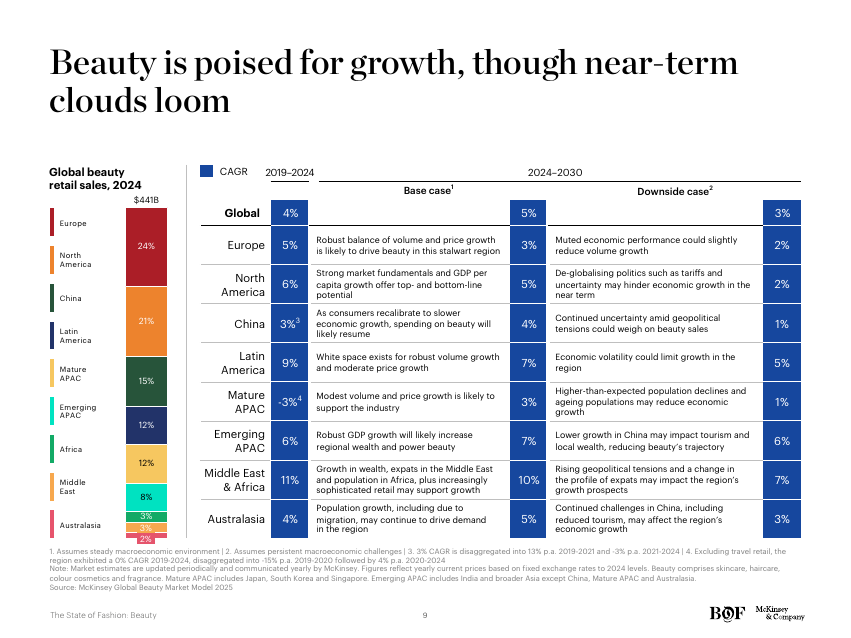

The global beauty industry — $441 billion in 2024 retail sales — is projected to grow at a 5% base-case CAGR through 2030 (3% in the downside case). After three years of effortless 7% annual growth driven by aggressive price increases, the formula has shifted: consumers will no longer absorb price hikes without proof of value.2024년 매출 기준 4,410억 달러 규모의 글로벌 뷰티 산업은, 2030년까지 기본 시나리오 기준 CAGR 5%의 성장세를 보일 것으로 전망됩니다 (다운사이드 시나리오에서는 3%). 공격적인 가격 인상으로 떠받쳐졌던 지난 3년간의 손쉬운 연 7% 성장 공식은 이미 변했습니다. 소비자들은 더 이상 ‘가치(value) 증명’ 없이는 가격 인상을 받아들이지 않습니다.

Regional growth diverges sharply. The Middle East & Africa leads at 11% CAGR (2019–2024), driven by growing wealth, the expat economy, and increasingly sophisticated retail. Latin America (9%) and Emerging APAC including India (6%) are robust. Europe (5%) tracks the global average. China is rebounding from a difficult period and is expected to recover to a mid-single-digit growth rate. Mature APAC — Japan, Korea, Singapore — faces structural decline at −3%, reflecting demographic ageing and a saturated home market.지역별 성장세는 극명하게 갈립니다. 중동&아프리카가 2019–2024년 CAGR 11%로 선두를 달리고 있으며, 이는 부의 성장, 외국인 경제권의 확장, 그리고 보다 정교해진 리테일이 이끌고 있습니다. 라틴아메리카(9%)와 인도를 포함한 신흥 APAC(6%) 또한 견조한 성장을 보입니다. 유럽(5%)은 글로벌 평균에 부합합니다. 중국은 어려운 시기를 지나 중기 회복이 예상되며, 한 자릿수 중반 성장률로 회귀할 것으로 보입니다. 일본·한국·싱가포르를 포함한 성숙 APAC은 인구 고령화와 포화된 내수 시장을 반영하여 −3%의 구조적 역성장에 직면해 있습니다.

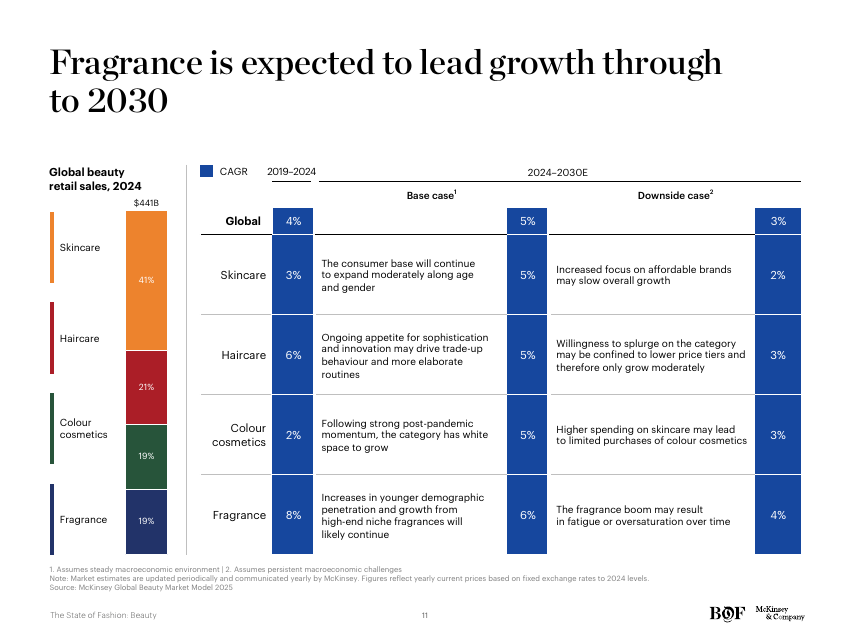

Fragrance grew at a striking 8% CAGR from 2019–2024 and is projected to continue at 6% through 2030 in the base case — the fastest-growing of the four core beauty categories. The drivers: increased penetration among younger consumers (especially Gen-Z and teenage boys via TikTok), and continued white space in high-end niche fragrances. The downside risk: fragrance fatigue or oversaturation. Skincare, the largest category at 41% of $441B global sales, grew 3% historically and is projected at 5% through 2030. Haircare (21% share) at 5%; colour cosmetics (19% share) at 5% recovering from a flat post-pandemic.향수는 2019–2024년 CAGR 8%라는 두드러진 성장을 기록했으며, 기본 시나리오 기준 2030년까지 6%의 성장을 이어갈 것으로 전망됩니다 — 4대 핵심 뷰티 카테고리 중 가장 빠른 성장세입니다. 동력은 두 가지: 젊은 소비자층 (특히 Gen-Z 및 틱톡을 매개로 한 10대 남성)에서의 침투율 확대, 그리고 하이엔드 니치 향수 영역의 지속적인 화이트 스페이스입니다. 다운사이드 리스크는 ‘향수 피로감’(fragrance fatigue) 또는 시장 포화입니다. 4,410억 달러 글로벌 매출의 41%를 차지하는 가장 큰 카테고리인 스킨케어는 과거 3%에서 2030년까지 5%로 회복이 예상됩니다. 헤어케어 (점유율 21%)는 5%, 색조화장품 (점유율 19%)은 팬데믹 이후의 정체기를 지나 5%의 회복세가 전망됩니다.

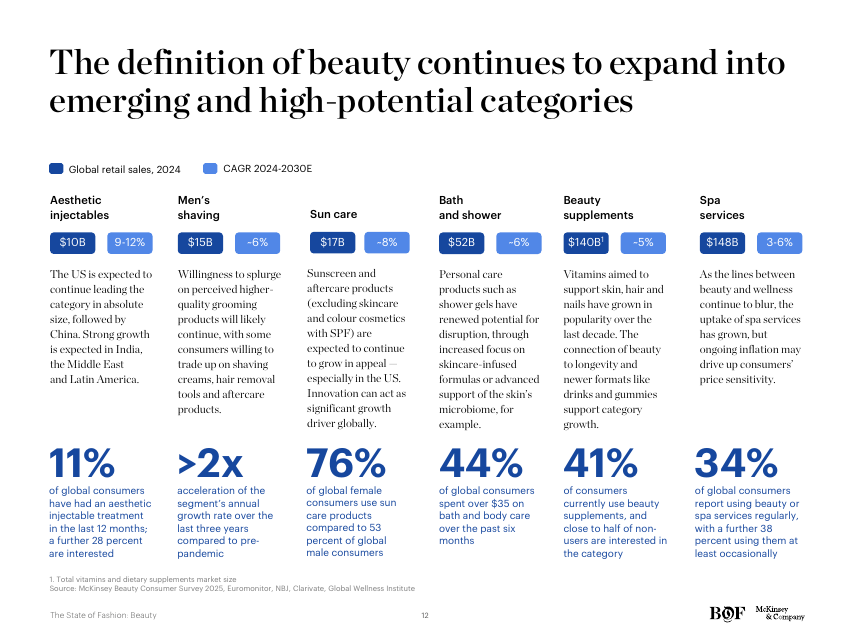

Adjacent categories — bath and shower ($52B, ~6% growth), sun care ($17B, ~8%), oral care, deodorants, supplements, aesthetic treatments — are increasingly competing for the same consumer wallet as core beauty. 44% of global consumers spent over $35 on bath and body care in the past six months. Beauty companies should consider whether to extend into these spaces, partner with wellness brands, or hold the line on their core.인접 카테고리들 — 목욕·샤워 (520억 달러, 약 6% 성장), 선케어 (170억 달러, 약 8% 성장), 구강 케어, 데오드란트, 영양제, 미용 시술 — 은 점차 핵심 뷰티와 같은 소비자 지갑을 두고 경쟁하고 있습니다. 글로벌 소비자의 44%가 지난 6개월간 목욕·바디케어에 35달러 이상을 지출했습니다. 뷰티 기업들은 이러한 영역으로의 확장 여부, 웰니스 브랜드와의 제휴 여부, 또는 핵심에 집중할지를 전략적으로 판단해야 할 시점입니다.

The pricing tailwind that drove much of 2022–2024 growth is essentially spent. Beauty inflation outpaced wages in most major markets, and consumers are now resistant. Affordability perception varies sharply by category: 83% of consumers feel haircare is affordable; only 67% feel fragrance is. For prestige fragrance specifically, the trade-up logic that powered the last cycle now requires a clearer proof of differentiation — either through ingredient quality, narrative, or scarcity.2022–2024년 성장의 상당 부분을 견인한 가격 인상의 순풍은 사실상 소진되었습니다. 뷰티 인플레이션은 대부분의 주요 시장에서 임금 상승률을 추월했고, 소비자들은 이제 가격 인상에 저항하고 있습니다. ‘감당 가능함(affordability)’에 대한 인식은 카테고리별로 크게 갈립니다: 소비자의 83%는 헤어케어를 감당할 만하다고 인식하지만, 향수에서는 그 비율이 67%에 그칩니다. 특히 프레스티지 향수에서는, 지난 사이클을 이끌었던 트레이드업(trade-up) 논리가 이제 보다 명확한 차별화 증명을 요구합니다 — 원료의 품질, 서사(narrative), 또는 희소성 중 무엇으로든.

Shifting macro dynamics, wealth patterns and migration are reshaping shopper profiles across both mature and emerging markets. To stay competitive, companies must prepare for disruption and anticipate changes across generations and cultures. Each market will have layered nuances — hyper-localisation is needed to meet consumer needs.거시 경제 동향의 변화, 부의 패턴, 그리고 이주(migration)는 성숙 시장과 신흥 시장 양쪽 모두에서 소비자 프로파일을 재구성하고 있습니다. 경쟁력을 유지하려면, 기업들은 세대 간·문화 간 변화를 예측하고 그에 따른 격변에 대비해야 합니다. 시장마다 층층의 미묘한 차이가 존재하며 — 진정으로 소비자의 니즈에 부합하기 위해서는 ‘하이퍼 로컬라이제이션’이 필수입니다.

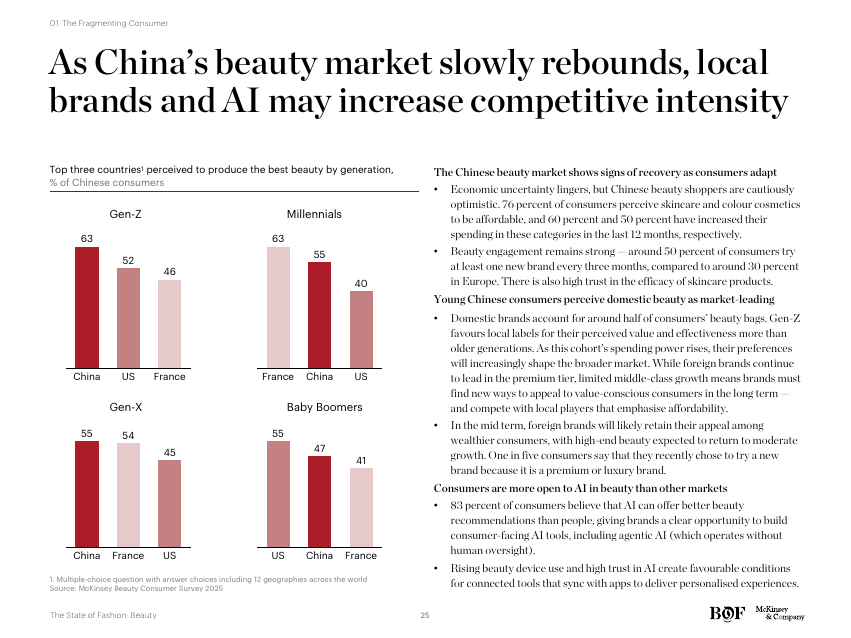

The Chinese beauty market is recovering, but the playing field is different. 76% of Chinese consumers perceive skincare and colour cosmetics to be affordable; 60% and 50% have increased spending in these categories in the past 12 months. Beauty engagement remains strong — around 50% of consumers try at least one new brand every three months, compared to ~30% in Europe. There is also high trust in the efficacy of skincare products.중국 뷰티 시장은 회복 중이나, 경기장의 규칙이 달라졌습니다. 중국 소비자의 76%가 스킨케어와 색조화장품을 감당 가능한 가격대로 인식하고 있으며, 각각 60%와 50%가 지난 12개월 동안 해당 카테고리의 지출을 늘렸습니다. 뷰티에 대한 참여도는 여전히 높습니다 — 약 50%의 소비자가 3개월에 한 번씩 새로운 브랜드를 시도하며, 이는 유럽의 약 30%와 비교됩니다. 스킨케어 제품의 효능에 대한 신뢰도 또한 높습니다.

Young Chinese consumers perceive domestic beauty as market-leading. Domestic brands account for around half of consumers' beauty bags. Gen-Z favours local labels for their perceived value and effectiveness more than older generations. As this cohort's spending power rises, their preferences will increasingly shape the broader market. While foreign brands continue to lead in the premium tier, limited middle-class growth means brands must find new ways to appeal to value-conscious consumers in the long term — and compete with local players that emphasise affordability.젊은 중국 소비자들은 자국 뷰티를 시장 선도적이라고 인식합니다. 자국 브랜드가 소비자 뷰티 백(beauty bag)의 약 절반을 차지하며, Gen-Z는 기성세대보다 더 강하게 자국 브랜드의 ‘가치’와 ‘효능’을 신뢰합니다. 이 세대의 구매력이 상승할수록, 그들의 선호가 시장 전반의 방향을 더 크게 좌우할 것입니다. 외국 브랜드는 여전히 프레스티지 영역을 주도하고 있으나, 중산층 성장의 제약은 장기적으로 가치 지향적 소비자에게 호소할 새로운 방식을 요구합니다 — 동시에 ‘감당 가능함’을 강조하는 로컬 브랜드들과의 경쟁이 불가피합니다.

Consumers in China are more open to AI in beauty than in other markets. 83% of Chinese consumers believe AI can offer better beauty recommendations than people, giving brands a clear opportunity to build consumer-facing AI tools, including agentic AI. Rising beauty device use and high trust in AI create favourable conditions for connected tools that sync with apps to deliver personalised experiences.중국 소비자들은 다른 시장에 비해 뷰티 AI에 훨씬 더 개방적입니다. 중국 소비자의 83%가 ‘AI가 사람보다 더 좋은 뷰티 추천을 할 수 있다’고 응답했으며, 이는 브랜드들이 에이전틱 AI를 포함한 소비자 접점 AI 도구를 구축할 수 있는 명확한 기회입니다. 뷰티 디바이스 사용의 증가와 AI에 대한 높은 신뢰도는, 앱과 동기화하여 개인 맞춤형 경험을 제공하는 커넥티드 도구에 우호적인 환경을 형성합니다.

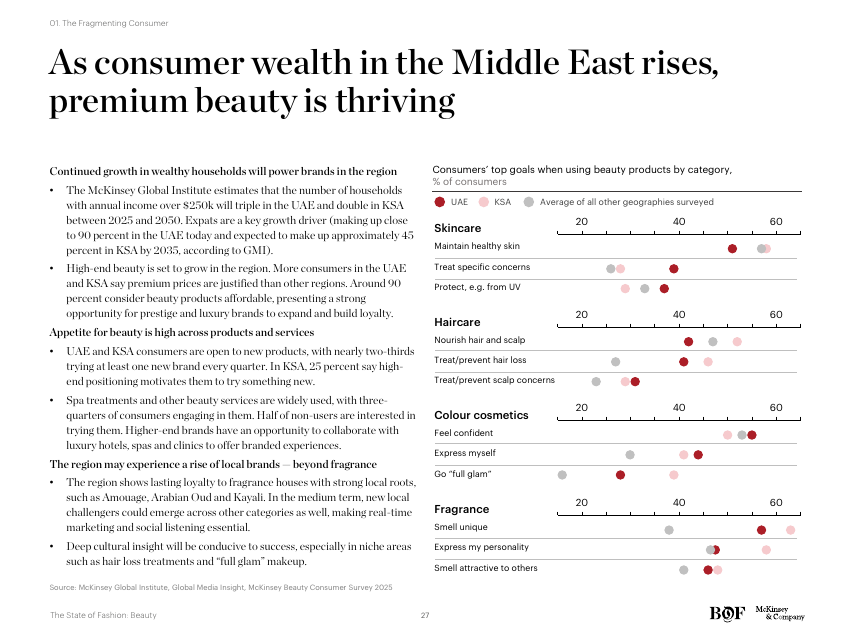

Nearly two-thirds of consumers in the Middle East try at least one new beauty brand every three months, compared to roughly 30% in Europe — the highest brand-experimentation rate in the world. Rising wealth, a young population, an influential expat economy, and increasingly sophisticated retail (especially in the Gulf) are combining to support 11% CAGR for the region, the highest of any. For global premium and niche brands, this is the most actionable single growth opportunity in the report.중동 소비자의 약 2/3가 3개월마다 최소 한 개 이상의 새로운 뷰티 브랜드를 시도합니다 — 유럽의 약 30%와 비교되는, 세계 최고 수준의 브랜드 실험 의향입니다. 부의 성장, 젊은 인구 구조, 영향력 있는 외국인 경제권, 그리고 (특히 걸프 지역에서) 점차 정교해지는 리테일이 결합되어, 이 지역은 모든 권역 중 가장 높은 CAGR 11%를 견인하고 있습니다. 글로벌 프레스티지 및 니치 브랜드에게는, 본 보고서에서 가장 실행 가능한 단일 성장 기회입니다.

Instead of fixating on beauty's slowdown, German beauty conglomerate Beiersdorf is keeping its focus on steady growth. The owner of household brands like Nivea and Aquaphor — as well as luxury labels like La Prairie and Chantecaille — is betting big on emerging markets, strength in mass labels and hero ingredients to keep up momentum.독일 뷰티 그룹 Beiersdorf는 뷰티 산업의 둔화에 매몰되기보다, 꾸준한 성장에 초점을 맞추고 있습니다. Nivea와 Aquaphor 같은 대중적 브랜드, La Prairie와 Chantecaille 같은 럭셔리 브랜드를 보유한 동사는, 신흥 시장 진출, 매스(mass) 브랜드의 강세, 그리고 ‘히어로 원료’ 전략에 크게 베팅하며 성장 모멘텀을 유지하고 있습니다.

In April, the group reported first-quarter sales growth of 3.6% to €2.7 billion ($3 billion) and maintained full-year guidance of 4 to 6% sales growth. Its portfolio of drugstore and dermatological brands has offered the company some stability. Luxury skincare label La Prairie has struggled in part due to the slowdown in China; its global sales dropped 17.5% in the first quarter.4월, 그룹은 1분기 매출이 3.6% 증가한 27억 유로 (30억 달러)를 기록했으며, 연간 가이던스인 매출 성장 4–6%를 유지한다고 발표했습니다. 드러그스토어 및 더마톨로지컬 브랜드 포트폴리오는 일정 수준의 안정성을 제공해 왔습니다. 다만 럭셔리 스킨케어 브랜드 La Prairie는 중국 둔화의 영향으로 부진을 겪었으며, 1분기 글로벌 매출이 17.5% 하락했습니다.

Many companies have been facing a challenging start to this year, but you kept your full-year guidance of 4 to 6 percent growth. What are the biggest headwinds facing beauty right now globally, and how is your company overcoming them?

올해 초 많은 기업이 어려운 출발을 한 가운데, 귀사는 연간 4–6% 성장 가이던스를 유지했습니다. 현재 글로벌 뷰티가 직면한 가장 큰 역풍은 무엇이며, 귀사는 이를 어떻게 극복하고 있습니까?

We have to get used to the fact that the market is going down to a slower growth level. We are no longer in the double-digit growth we had after Covid. In this market, the usual headwind is obviously China, because we don't know what will happen there. We are still all hoping to get a recovery. The new headwind is we are not so sure what will happen in the US with all this stop-and-go on tariffs. Where we have the really good potential is still in emerging markets — not only the usual suspects, like Latin America and Southeast Asia, but for example, India. India is a country where we are all investing a lot, because there is new distribution online. There is also the middle class willing to spend money.

시장이 더 낮은 성장률로 내려앉고 있다는 사실을 받아들여야 합니다. 우리는 더 이상 코로나 직후의 두 자릿수 성장 구간에 있지 않습니다. 이 시장의 통상적 역풍은 단연 중국입니다. 회복이 언제 올지 알 수 없는 상황에서, 우리 모두 회복을 기다리고 있습니다. 새로운 역풍은 미국입니다. 관세를 둘러싼 ‘가다 서다(stop-and-go)’ 정책 때문에 미국에서 무엇이 어떻게 전개될지 명확하지 않습니다. 진정으로 좋은 잠재력이 있는 곳은 여전히 신흥 시장입니다 — 라틴아메리카, 동남아시아 같은 통상적인 시장뿐 아니라, 예를 들어 인도가 그러합니다. 인도는 모두가 큰 투자를 하고 있는 국가입니다. 새로운 온라인 유통이 형성되고 있고, 또한 지출할 의향을 가진 중산층이 성장하고 있기 때문입니다.

For La Prairie, are you focusing more on making changes to the China strategy or on other regions?

La Prairie의 경우, 중국 전략을 수정하는 데 더 집중하고 계십니까, 아니면 다른 지역에 집중하고 계십니까?

We have been pretty late entering the e-commerce ecosystem in China. We are super successful, first with Tmall, then we entered with JD.com and have been active for one year on TikTok. We are trying to correct a few mistakes. For example, we were increasing prices at a level which was not sustainable. The second element: we are trying to make our counters more welcoming. We are changing the way we welcome customers. Beyond that, we are diversifying. La Prairie has been historically very dependent on China. We are trying to develop in regions like the Middle East — we recently opened a counter at Galeries Lafayette in Doha. We are also investing in the US, which is a market where La Prairie has under-indexed historically.

우리는 중국의 이커머스 생태계에 다소 늦게 진입했습니다. 그러나 진입 이후 매우 성공적이었습니다 — 먼저 Tmall, 그 다음 JD.com, 그리고 지난 1년간 TikTok에 적극 진출하고 있습니다. 몇 가지 실수를 바로잡으려 노력 중입니다. 예를 들어, 지속 가능하지 않은 수준으로 가격을 인상해 왔던 부분이 있습니다. 두 번째로, 매장(카운터)을 더 환대(歡待)의 공간으로 만들고자, 고객을 맞이하는 방식 자체를 바꾸고 있습니다. 그 외에도 다각화를 추진 중입니다. La Prairie는 역사적으로 중국 의존도가 매우 높았는데, 이제 중동과 같은 시장에서의 성장을 도모하고 있습니다 — 최근에는 도하의 Galeries Lafayette에 카운터를 개설했습니다. 미국에도 투자하고 있습니다. 역사적으로 La Prairie의 침투가 낮았던 시장이기 때문입니다.

How is the US tariff situation impacting your business?

미국의 관세 상황이 사업에 어떤 영향을 미치고 있습니까?

We don't produce a third of our products in the US. We will not open a new factory. What we have done is some stocking. We had built some inventory in the US ahead of any tariff announcement. The risk is more about consumer sentiment than the tariffs themselves — if consumers reduce spending, that's the bigger concern. There is a little shift from premium to mass, which is not bad for us, because we have both. We have Nivea, which is a fantastic mass brand, and we have Eucerin, which is a derma brand at an affordable price point. So we cover both segments.

우리는 미국 내에서 제품의 1/3을 생산하지 않습니다. 새 공장을 열 계획은 없습니다. 우리가 한 일은 약간의 재고 비축입니다. 관세 발표 이전에 미국 내 일정 재고를 미리 쌓아 두었습니다. 다만 진짜 리스크는 관세 그 자체보다 소비자 심리(consumer sentiment)에 있습니다 — 소비자가 지출을 줄이면, 그것이 더 큰 우려입니다. 일부 프레스티지에서 매스로의 이동이 관찰되는데, 이는 우리에게 나쁜 신호만은 아닙니다. 우리는 양쪽 모두를 보유하고 있기 때문입니다. 환상적인 매스 브랜드 Nivea와, 합리적 가격의 더마 브랜드 Eucerin이 있어 두 세그먼트를 모두 커버합니다.

Beyond regions, what categories give you the most confidence in your growth outlook?

지역을 넘어, 성장 전망에 가장 큰 자신감을 주는 카테고리는 무엇입니까?

Hero ingredients. We have built our brands around a few hero molecules — Hyaluronic Acid, Q10, Thiamidol for hyperpigmentation. Thiamidol in particular is a Nivea/Eucerin asset that we believe still has years of runway. Innovation around proven, branded ingredients is what wins right now. Consumers don't want forty new ingredients each year — they want depth around what already works. Also fragrance: we have Coppertone and we have continued to invest in our derma fragrance launches. The fragrance market is structurally strong and we are taking our share of it.

‘히어로 원료’입니다. 우리는 몇 가지 핵심 분자(hero molecule)를 중심으로 브랜드를 구축해 왔습니다 — 히알루론산, Q10, 그리고 색소침착(hyperpigmentation)에 효과적인 Thiamidol. 특히 Thiamidol은 Nivea와 Eucerin의 자산으로, 앞으로도 수년간 성장 활주로가 남아 있다고 봅니다. 검증된, 브랜드화된 원료를 중심으로 한 혁신이 지금의 승부처입니다. 소비자들은 매년 40가지 새 원료를 원하는 것이 아니라, 효과가 입증된 것을 중심으로 한 ‘깊이(depth)’를 원합니다. 향수 또한 강조하고 싶습니다. Coppertone을 보유하고 있으며, 더마 향수 출시에도 지속적으로 투자해 왔습니다. 향수 시장은 구조적으로 견고하며, 우리는 그 시장에서의 점유를 확대하고 있습니다.

This interview has been edited and condensed.본 인터뷰는 편집 및 축약되었습니다.

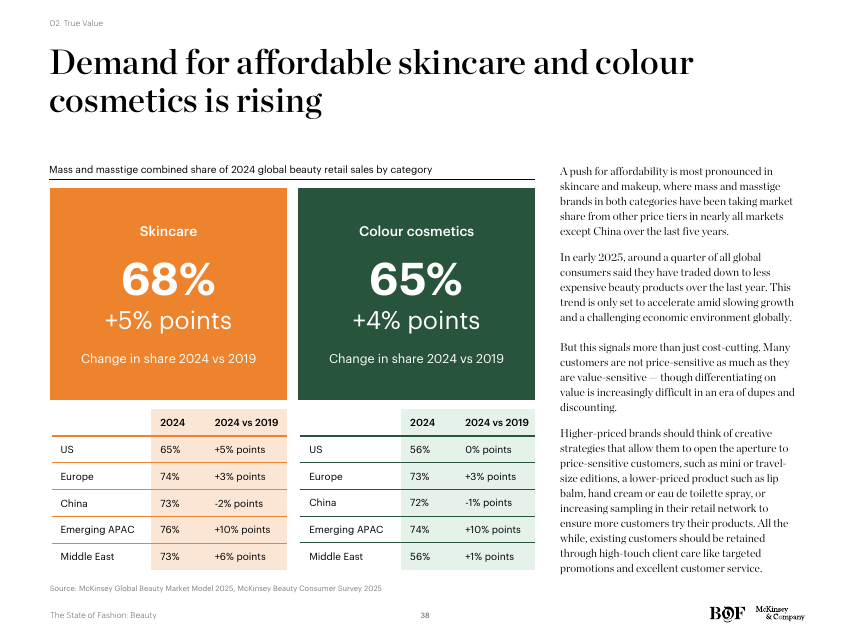

Accessibly priced beauty brands have proven they can challenge pricier counterparts on efficacy, innovation and virality, raising consumer expectations across the market. As consumers grow more selective and cost-conscious, brands must demonstrate a clear and ownable value proposition, regardless of price.합리적 가격대의 뷰티 브랜드들은 효능, 혁신, 그리고 바이럴 측면에서 고가 브랜드에 도전할 수 있음을 입증해 왔고, 이는 시장 전반에서 소비자 기대치를 끌어올렸습니다. 소비자들이 더 선별적이고 가격 민감해질수록, 브랜드는 가격대를 막론하고 명확하고 자기만의(ownable) 가치 제안을 증명해야 합니다.

63% of consumers do not think premium beauty products are higher-performing than mass beauty ones. This is the single most consequential survey finding for the luxury fragrance category — it directly attacks the trade-up narrative that has powered prestige growth for two decades. Brands defending a premium price point now need to demonstrate, not assert, why the price is justified: through superior ingredients, defensible craftsmanship, scarce raw materials, or a worldview the consumer wants to be part of.소비자의 63%는 ‘프레스티지 뷰티 제품이 매스 제품보다 성능이 우수하다’고 생각하지 않습니다. 이는 럭셔리 향수 카테고리에 가장 결정적인 조사 결과입니다 — 지난 20년간 프레스티지 성장의 핵심이었던 ‘트레이드업’ 서사를 정면으로 공격하는 데이터이기 때문입니다. 프레스티지 가격대를 방어하려는 브랜드는, 이제 가격의 정당성을 ‘주장’하는 것이 아니라 ‘증명’해야 합니다: 우월한 원료, 방어 가능한 장인 정신(craftsmanship), 희소한 원자재, 또는 소비자가 일부가 되고 싶어 하는 세계관(worldview)을 통해서입니다.

Kiko Milano, founded in 1997 in Italy, has long walked the tightrope between high-quality cosmetics and accessible pricing. Since 2022, it has begun an elevation strategy — reducing promotions, changing distribution and introducing more premium products. As well as $4.50 lip liners, it now offers a $28 serum-primer hybrid and a $32 eyeshadow palette. The brand can be found in premium department stores like El Corte Inglés and Galeries Lafayette.1997년 이탈리아에서 설립된 Kiko Milano는, 오랜 기간 ‘고품질 화장품’과 ‘합리적 가격’ 사이의 외줄을 걸어 왔습니다. 2022년부터 격상(elevation) 전략을 시작하여 — 프로모션을 줄이고, 유통 전략을 전환했으며, 보다 프레스티지한 제품을 도입했습니다. 4.50달러 립라이너에 더해, 이제 28달러 세럼-프라이머 하이브리드, 32달러 아이섀도 팔레트도 함께 제공합니다. 브랜드는 El Corte Inglés, Galeries Lafayette 같은 프레스티지 백화점에도 입점해 있습니다.

The strategy is working: sales grew 14% in 2024 to €900 million (~$1 billion), and LVMH-backed investment firm L Catterton took a majority stake the same year. CEO Simone Dominici says further premiumisation can grow the brand's global appeal and margins, while maintaining accessible pricing brings in new customers across the wealth spectrum.전략은 효과를 내고 있습니다: 매출은 2024년 14% 증가한 9억 유로 (약 10억 달러)에 도달했고, 같은 해 LVMH 산하 투자사 L Catterton이 경영권 지분을 인수했습니다. CEO Simone Dominici는, 추가적인 프리미엄화가 브랜드의 글로벌 호소력과 마진을 모두 끌어올릴 수 있으며, 동시에 합리적 가격대를 유지함으로써 다양한 소득층의 신규 고객을 확보할 수 있다고 말합니다.

Is your core customer shopping for affordable beauty only?

귀사의 핵심 고객은 오직 합리적 가격대의 뷰티만을 소비합니까?

They mix and match. We define ourselves as an entry-prestige brand now. In our stores, we see Prada bags and Louis Vuitton bags. The customer might have a lipstick from Chanel that they match with their eyeshadow from Kiko; the common denominator is the quality. Because we want to be entry-prestige, it doesn't mean we cannot have affordable products that are still benchmarked against the best of the prestige category. We have to be excellent at every price point.

고객은 ‘믹스 앤 매치’를 합니다. 우리는 이제 스스로를 ‘엔트리 프레스티지(entry-prestige)’ 브랜드로 정의합니다. 매장에서 Prada, Louis Vuitton 가방을 든 고객들을 봅니다. 그들은 Chanel 립스틱에 Kiko 아이섀도를 매치할 수 있습니다. 그 공통 분모는 ‘품질’입니다. 우리가 엔트리 프레스티지를 지향한다고 해서, 합리적 가격대의 제품을 가질 수 없다는 의미는 아닙니다 — 다만 그 제품들조차 프레스티지 카테고리 최고의 제품을 기준으로 측정되어야 합니다. 우리는 모든 가격대에서 탁월해야 합니다.

There's a lot of pressure to continually deliver newness; tell me how you handle that.

지속적으로 ‘새로움’을 출시해야 한다는 압박이 큽니다. 어떻게 대응하고 계십니까?

There's social listening, and talking to suppliers, talking to customers through our loyalty program. It's an ecosystem. Our marketing team works with suppliers to download these ideas into concrete projects that can last between 12 and 18 months. It's a medium- to long-term innovation process. You start today thinking of the concept. What you think of today will probably be ready by the end of 2026. The ingredients, the formulation, the regulation, the compatibility with the packaging — it takes time. True innovation doesn't come in a month, unfortunately.

‘소셜 리스닝’이 있고, 공급사들과의 대화가 있으며, 로열티 프로그램을 통한 고객과의 대화가 있습니다. 그것은 하나의 ‘생태계’입니다. 우리 마케팅 팀은 공급사들과 협업해 이러한 아이디어들을 12~18개월에 걸친 구체적인 프로젝트로 구현합니다. 이는 중장기 혁신 프로세스입니다. 오늘 컨셉을 시작하면, 그 컨셉이 실제 출시되는 시점은 아마 2026년 말입니다. 원료, 처방, 규제, 패키지와의 적합성 — 이 모두에는 시간이 듭니다. 진정한 혁신은 안타깝게도 한 달 안에 나오지 않습니다.

How do you create repeat customers?

재구매 고객은 어떻게 만드십니까?

Even when we are selling through department stores or marketplaces like Amazon, the majority of our sales are DTC, so we have a direct relationship with our customers. We have almost 7 million active loyal customers, meaning they buy with us more than once a year. On average, they buy with us 1.9 times a year. Our communication is more and more personalised. The newsletter you receive is not the same one another receives; it's based on your lifestyle and your past behaviours. The more you are personalising the approach, the more the customers feel heard and the more they come back. We also have a unified commerce platform through which our inventory, customer database and transaction data are shared.

백화점이나 Amazon 같은 마켓플레이스에 판매할 때조차, 우리 매출의 대부분은 DTC입니다 — 따라서 우리는 고객과 ‘직접적인 관계’를 가집니다. 약 700만 명의 액티브 로열 고객이 있으며, 이들은 연 1회 이상 구매합니다. 평균적으로 연 1.9회 구매합니다. 우리의 커뮤니케이션은 점점 더 개인화되고 있습니다. 귀하가 받는 뉴스레터는 다른 고객이 받는 것과 다르며, 귀하의 라이프스타일과 과거 행동에 기반합니다. 접근 방식을 개인화할수록, 고객은 더 ‘경청받고 있다’고 느끼고 더 자주 돌아옵니다. 또한 재고, 고객 DB, 거래 데이터를 통합 공유하는 유니파이드 커머스 플랫폼을 운영하고 있습니다.

In 2025, we see a cooling in beauty market growth. How are you feeling about the near term?

2025년 뷰티 시장 성장이 둔화되는 양상을 보이고 있습니다. 단기 전망에 대해서는 어떻게 보십니까?

In the last three years, we doubled, which is three times the market average. But there is a lot of room for us because our market share is negligible in some very large markets, like the US. This is where L Catterton is helping. It won't be easy, but there is room for high-quality products in this entry-prestige market at a democratic price. We signed a deal with Reliance, one of the largest operators in India, at the beginning of the year. We opened in Indonesia in January, which is home to 200 million people. We opened in Pakistan in 2024, and we're in Brazil, Chile and just opened in Mexico. We're entering Kenya, Ghana, Nigeria. In 2025, there will be 2 billion customers that we have never reached before.

지난 3년간 우리는 매출을 두 배로 늘렸으며 — 이는 시장 평균의 3배입니다. 다만 미국과 같은 거대 시장에서 우리의 점유율은 미미하기에, 여전히 큰 성장 여지가 있습니다. 이 부분에서 L Catterton이 큰 도움이 됩니다. 쉽지는 않겠지만, ‘엔트리 프레스티지’ 시장에서 ‘민주적 가격’의 고품질 제품에 대한 여지는 충분합니다. 우리는 연초 인도 최대 사업자 중 하나인 Reliance와 계약을 체결했습니다. 1월에는 인구 2억의 인도네시아에 진출했고, 2024년에는 파키스탄에 진입했으며, 브라질, 칠레, 그리고 막 멕시코에도 진출했습니다. 케냐, 가나, 나이지리아에도 진출 예정입니다. 2025년에 우리는 이전에 한 번도 도달한 적 없는 20억 명의 신규 잠재 고객을 마주하게 됩니다.

What do you think the beauty consumer of tomorrow wants?

내일의 뷰티 소비자는 무엇을 원한다고 보십니까?

I think they are more equipped than previous generations to spot inauthenticity. I think dupes will become less popular and there will be more demand for authenticity. Value will be an important element, because the economic conditions might not be so relaxed in the future.

그들은 기성세대보다 ‘비진정성(inauthenticity)’을 더 잘 포착할 수 있는 세대입니다. ‘듀프(dupe)’에 대한 인기는 감소하고, ‘진정성(authenticity)’에 대한 수요는 더 커질 것입니다. 미래의 경제 환경이 그리 너그럽지 않을 수 있기에, ‘가치’가 중요한 요소가 될 것입니다.

This interview has been edited and condensed.본 인터뷰는 편집 및 축약되었습니다.

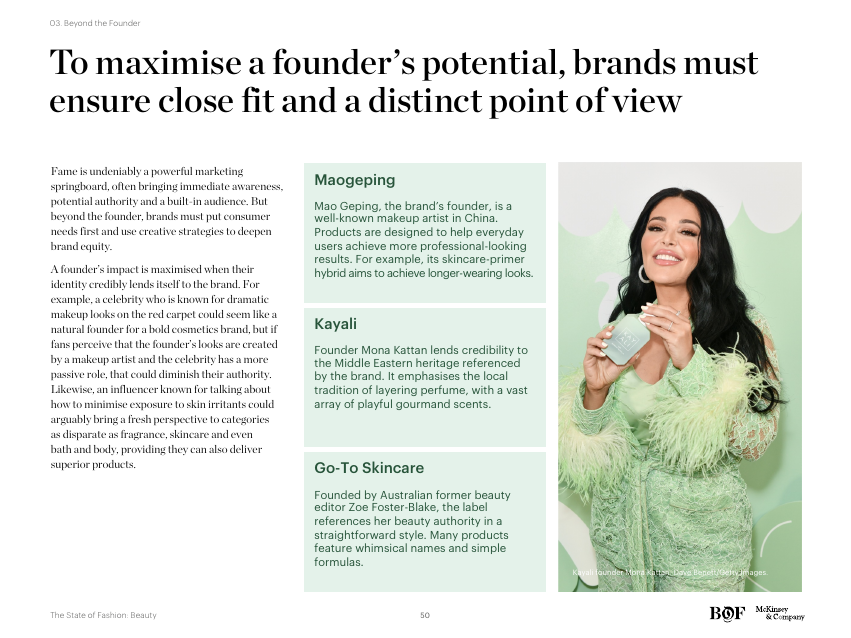

Over the last decade, an avalanche of brands with public-facing founders emerged. Communities were often built around their personal aesthetic, lifestyle, or social presence. But while a prominent founder can propel growth, their appeal alone is insufficient for long-term success. With many branding niches now overcrowded, quality and originality will be key.지난 10년간, ‘공개적으로 활동하는 창업자(public-facing founder)’를 앞세운 브랜드들이 폭발적으로 등장했습니다. 커뮤니티는 종종 그들의 개인적 미학, 라이프스타일, 또는 소셜 미디어 존재감을 중심으로 형성되었습니다. 그러나 두드러진 창업자가 성장을 견인할 수는 있어도, 그들의 호소력만으로 장기적 성공을 담보할 수는 없습니다. 많은 브랜딩 니치가 이미 과밀화된 지금, 결국 ‘품질’과 ‘독창성’이 관건입니다.

The headline statistic: only three founder-led brands established in the past two decades have scaled beyond $1 billion in sales. The cohort effect is even more telling — the vast majority of celebrity- or founder-led launches plateau at the $50–200M range and stall. The brands that have scaled past $1B have done so by building infrastructure, IP, and category leadership that survives the founder's individual story.핵심 통계: 지난 20년간 출범한 창업자 중심 브랜드 중 매출 10억 달러를 넘긴 곳은 단 3개에 불과합니다. 코호트 효과는 더 시사적입니다 — 셀러브리티 또는 창업자 중심으로 출범한 브랜드의 절대 다수가 매출 5,000만~2억 달러 구간에서 정체합니다. 10억 달러를 넘긴 소수의 브랜드들은, 창업자 개인의 서사를 넘어서 살아남는 인프라, IP, 그리고 카테고리 리더십을 구축함으로써 그 단계에 도달했습니다.

When Deciem launched in 2013, it was the ultimate beauty disruptor. The Ordinary changed the skincare game by offering science-backed serums — niacinamide, hyaluronic acid — for under $10 a bottle, with radical transparency in marketing. Estée Lauder first invested in 2017 and completed acquisition in 2024. Today, Deciem operates in a much-changed industry. Co-founder Brandon Truaxe, the brand's most public face, died in 2019. The Ordinary's differentiating factor — ingredient transparency at low prices — is now an industry standard. Countless upstarts nip at its heels.2013년 출범한 Deciem은 ‘뷰티의 궁극적 파괴자’였습니다. The Ordinary는 나이아신아마이드, 히알루론산 같은 과학 기반 세럼을 10달러 이하의 가격에, 마케팅에서의 급진적 투명성과 함께 제공함으로써 스킨케어의 판도를 바꾸었습니다. Estée Lauder는 2017년 첫 투자 이후 2024년에 인수를 완료했습니다. 오늘날 Deciem이 활동하는 산업은 그때와는 매우 다릅니다. 브랜드의 가장 공개적인 얼굴이었던 공동 창립자 Brandon Truaxe는 2019년에 사망했으며, The Ordinary의 차별화 요소였던 ‘합리적 가격대의 원료 투명성’은 이제 업계 표준이 되었습니다. 수많은 신생 브랜드들이 뒤를 바짝 쫓고 있습니다.

The Ordinary has grown from being a founder-led, groundbreaking start-up, to being owned by one of the biggest beauty conglomerates in the world. How do you think being founder-led helped you in the early days, but might limit you now?

The Ordinary는 창업자 주도의 혁신적 스타트업에서, 세계 최대 뷰티 그룹 중 하나의 자회사로 성장했습니다. 초기에 ‘창업자 주도’가 어떻게 도움이 되었고, 또 지금은 어떻게 제약이 될 수 있다고 보십니까?

We were always quite different in that way. Our co-founder Brandon was very visible at the beginning, but the brand was always positioned around the products and the ingredients, not the personalities. The challenge with having those types of very visible female founders is that, in a way, you're limiting your brand. People will think, ‘Well, I'm much older than them, I'm much younger’ — if you don't feel like you fall into that group. We always say we don't think about consumers from a gender or age group. We think about consumers from mindsets. Do they share our values? Are their thoughts aligned with us? Whereas when you're more founder-led, you're naturally going to target a demographic who associates with that person, because actually, the brand could be much wider than that.

우리는 항상 그런 면에서 다소 달랐습니다. 공동 창립자 Brandon은 초기에 매우 가시적이었지만, 브랜드 자체는 항상 제품과 원료를 중심으로 포지셔닝되었지, 인물 중심은 아니었습니다. 매우 가시적인 여성 창업자들의 경우, 어떤 의미에서 그것이 브랜드를 제약합니다. 사람들은 ‘나는 저 사람보다 훨씬 나이가 많네’, ‘훨씬 어리네’라며 자신이 그 집단에 속하지 않는다고 느낍니다. 우리는 항상 ‘소비자를 성별이나 연령으로 보지 않는다’고 말합니다. 우리는 소비자를 ‘마인드셋(mindset)’으로 봅니다. 그들이 우리의 가치를 공유하는가? 그들의 생각이 우리와 일치하는가? ‘창업자 주도’가 강해질수록 자연스럽게 그 인물과 동일시하는 인구 집단을 타기팅하게 되는데, 실제로는 브랜드가 그보다 훨씬 더 넓을 수 있습니다.

How do you think founders can balance wanting to give their brand a human connection without being too reliant on that one person?

창업자들이 브랜드에 ‘인간적 연결성’을 부여하면서도, 그 한 사람에게 과도하게 의존하지 않는 균형을 어떻게 잡을 수 있다고 보십니까?

We've always just put the brand first. Of course, we all do podcasts, we'll do press, and again, that's more just to tell the story because we're good at telling the story. On our social media, you would never see Brandon, particularly on social media, you'd never see myself, because the brand is more than us. The brand is about the community, the values, the integrity, everything we stand for, and we've never really needed to sell it based on an individual.

우리는 항상 브랜드를 우선해 왔습니다. 물론 우리 모두 팟캐스트를 하고, 언론에 출연하지만, 그것은 어디까지나 ‘이야기를 전달하기’ 위함이지, 우리가 이야기 전달에 능하기 때문입니다. 소셜 미디어에서는 Brandon을, 그리고 저 자신을 거의 보실 수 없습니다. 브랜드는 우리보다 큰 존재이기 때문입니다. 브랜드는 커뮤니티, 가치, 진정성 — 우리가 추구하는 모든 것에 관한 것입니다. 우리는 한 번도 개인을 기반으로 브랜드를 팔 필요가 없었습니다.

There's so much talk about the importance of building a community as a brand. How have you maintained that, even as the brand has grown?

‘브랜드로서의 커뮤니티 구축’이 매우 강조되는 시대입니다. 브랜드가 성장하는 동안 커뮤니티를 어떻게 유지해 오셨습니까?

We were lucky in the beginning that I feel like the community formed itself. On Facebook, there's The Ordinary chat room, which has over 200,000 members. That community is independent of us, which I actually think is much more organic. The reason it started is because we actually gave people the tools to talk about skincare because, before that, people didn't understand niacinamide or all these other ingredients. Also, the fact is that we've always stayed true to our values, even as we've gone through difficult times. We've lost our founder, we went through an acquisition, but people have always felt we maintained our values.

초기에 우리는 운이 좋게도 커뮤니티가 스스로 형성되었습니다. 페이스북에는 20만 명 이상의 멤버를 보유한 ‘The Ordinary 챗룸’이 있습니다. 그 커뮤니티는 우리와 독립적으로 존재하며, 오히려 그 점이 훨씬 더 유기적이라고 봅니다. 그 커뮤니티가 시작될 수 있었던 이유는, 우리가 사람들에게 ‘스킨케어에 대해 이야기할 수 있는 도구’를 제공했기 때문입니다. 그 전까지 사람들은 나이아신아마이드나 그 외 원료들을 잘 이해하지 못했습니다. 또한, 어려운 시기를 거치면서도 우리는 항상 가치에 충실했다는 점이 중요합니다. 창업자를 잃었고, 인수도 거쳤지만, 사람들은 항상 우리가 가치를 지켰다고 느꼈습니다.

This interview has been edited and condensed.본 인터뷰는 편집 및 축약되었습니다.

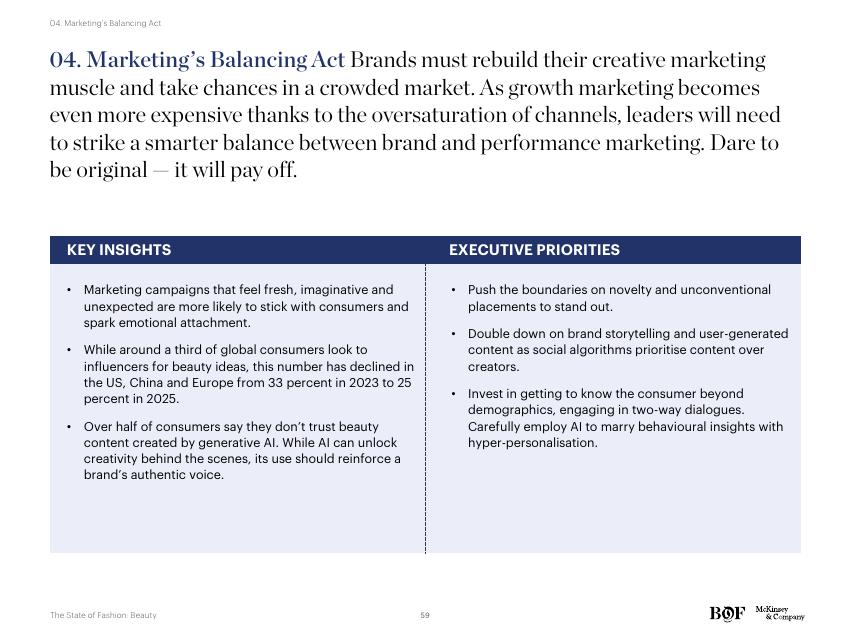

Brands must rebuild their creative marketing muscle and take chances in a crowded market. As growth marketing becomes even more expensive thanks to the oversaturation of channels, leaders will need to strike a smarter balance between brand and performance marketing. Dare to be original — it will pay off.브랜드는 창의적 마케팅 근육을 재건하고, 포화된 시장에서 과감한 베팅에 나서야 합니다. 채널 과포화로 인해 그로스 마케팅이 더욱 비싸지는 가운데, 리더들은 브랜드 마케팅과 퍼포먼스 마케팅 사이의 더 영리한 균형점을 찾아야 합니다. ‘독창성에 베팅하라’ — 그것이 결국 보상을 가져옵니다.

Influencer marketing's grip on consumer purchase decisions has weakened. The importance of influencers in inspiring beauty purchases declined 8 percentage points in the US, China and Europe between 2023 and 2025. The peak of pure influencer-driven launches has passed; consumers are increasingly aware of paid placements and increasingly resistant. Brands that compounded their growth through scaled creator deals now face plateauing returns.구매 결정에 대한 인플루언서 마케팅의 영향력은 약화되고 있습니다. 뷰티 구매를 영감(inspiration)하는 데 있어 인플루언서의 중요성은, 2023년과 2025년 사이 미국, 중국, 유럽에서 평균 8&percntp; 하락했습니다. 순수 인플루언서 주도형 출시의 정점은 이미 지났으며, 소비자들은 페이드 배치(paid placement)를 점점 더 잘 인식하고 점점 더 저항합니다. 대규모 크리에이터 거래를 통해 성장을 복리화했던 브랜드들은, 이제 수확 체감 구간에 진입했습니다.

Puig owns 14 prestige brands and three licences. The group has turned heritage names like Carolina Herrera and Rabanne into contemporary hits and built audiences for disruptor labels like Byredo, L'Artisan Parfumeur and Charlotte Tilbury. CEO Marc Puig — third-generation head — led the company through its near-€14 billion IPO in 2024. He says, to propel brands forward, it's more important to take risks than try to follow a set path. Fragrance, along with the group's fashion brands, accounts for 73% of Puig's business.Puig은 14개의 프레스티지 브랜드와 3개의 라이선스를 보유하고 있습니다. 동사는 Carolina Herrera와 Rabanne 같은 전통 브랜드들을 컨템포러리 히트작으로 전환시켰고, Byredo, L'Artisan Parfumeur, Charlotte Tilbury 같은 파괴자 브랜드의 팬덤도 구축해 왔습니다. 3대(代) 경영자인 Marc Puig CEO는 2024년 약 140억 유로 규모의 IPO를 이끌었습니다. 그는 브랜드를 진전시키기 위해서는 정해진 경로를 따르려 하기보다 ‘리스크를 감수하는 것’이 더 중요하다고 말합니다. 향수와 패션 브랜드는 합쳐서 Puig 사업의 73%를 차지합니다.

One of your biggest recent successes is Carolina Herrera Good Girl. The fragrance has a very distinct identity, separate from the fashion brand. How do you know when you can push marketing even further?

최근 가장 큰 성공 중 하나가 Carolina Herrera의 Good Girl입니다. 이 향수는 패션 브랜드와는 별개의 매우 독특한 정체성을 가졌습니다. 마케팅을 더 밀어붙일 수 있는 시점은 어떻게 판단하십니까?

There is this tension between the essence of the brand that we have to protect because otherwise we'll lose the identity. At the same time, we need to let the brand have its own life and keep evolving. It's like going on a bicycle; if you don't move, you fall. It's a delicate balance to decide what it is that makes the brand work. In this case, it's the sophistication and the atmosphere. The typical women's fragrance is in a cylinder bottle and male fragrance is a square bottle. Look at Good Girl; it's a shoe. When we launched it, people said, ‘Does this smell like a foot? How are you going to launch a fragrance in a shoe?’ Now it's the number one women's fragrance in the world. Look at 1 Million [a Rabanne fragrance], it's a gold ingot. We wanted, in the crisis year it launched in 2008, to talk to consumers in a way like, ‘Money will give you power.’

‘반드시 보호해야 하는 브랜드의 본질’과 ‘브랜드가 자신만의 생명을 가지고 계속 진화해야 한다는 필요’ 사이에는 늘 긴장이 있습니다. 그러지 않으면 정체성을 잃기 때문입니다. 이는 자전거를 타는 것과 비슷합니다. 움직이지 않으면 넘어집니다. 무엇이 그 브랜드를 작동하게 만드는지를 결정하는 일은 매우 섬세한 균형의 작업입니다. 이 경우, 그것은 ‘세련됨(sophistication)’과 ‘무드(atmosphere)’입니다. 일반적인 여성 향수는 원기둥 보틀, 남성 향수는 사각 보틀에 담깁니다. Good Girl을 보십시오 — 그것은 ‘구두(shoe)’입니다. 출시 당시 사람들은 ‘발 냄새가 나는 거 아니냐? 어떻게 구두 모양 보틀로 향수를 출시할 거냐?’라고 했습니다. 지금 그것은 세계 1위 여성 향수입니다. Rabanne의 1 Million을 보십시오 — 그것은 ‘금괴(gold ingot)’입니다. 위기였던 2008년 출시 당시, 우리는 소비자에게 ‘돈이 너에게 힘을 줄 것이다’라는 방식으로 말하고 싶었습니다.

Influencer marketing is a space always in flux. How big a part will it play in your overall strategy?

인플루언서 마케팅은 끊임없이 변화하는 영역입니다. 전체 전략에서 이 영역은 얼마나 큰 비중을 차지하게 될까요?

You cannot plan a social ‘pick.’ You have to create the conditions for that to happen. When it happens, make sure you're quick enough to feed it. You can't say, ‘my marketing plan is that I'm going to create a social frenzy.’ Marketing spend can feel just ever-justify a P&L, so there is a certain amount that you dedicate to promote your brands, and you try to make those expenses as efficient as possible, so you can do more with them. But we will try new things, whether it's AI in digital marketing or whatever.

‘소셜 픽(social pick)’은 계획할 수 있는 것이 아닙니다. 그것이 일어날 수 있는 ‘조건’을 만들어야 합니다. 일단 일어나면, 충분히 빠르게 그 파동을 키울 수 있어야 합니다. ‘나의 마케팅 계획은 소셜 광풍(frenzy)을 일으키는 것’이라고 말할 수는 없습니다. 마케팅 비용은 항상 P&L을 정당화해야 하기에, 브랜드 홍보에 일정 금액을 배정하고 가능한 한 효율적으로 사용하려 합니다. 그러나 디지털 마케팅에서의 AI든 무엇이든, 우리는 새로운 시도를 멈추지 않을 것입니다.

There will always be new challenger brands coming in, especially in makeup and fragrance. How do you stay ahead of the noise?

메이크업과 향수에서는 특히 신규 챌린저 브랜드가 끊임없이 등장합니다. 시장의 잡음을 어떻게 앞서가십니까?

New brands are born all the time, but very few pass the test of time. When I look at the brands we've partnered with in the last few years, they were in the market for up to 20 years before we got excited about their proposition. It's very easy to launch a new brand, because at the end of the day, it's not that complicated to create products, and there's third parties that can help you do that. It's very difficult to escalate and to pass the fad of the moment. There has to be a reason, a point of view that is differentiated, and not all brands have that. I think there will continue to be many new brands coming up. I think that 99 percent of them will not pass the test of time, and a few, yes, will escalate and will be able to make a dent in the industry.

새로운 브랜드는 늘 태어나지만, ‘시간의 시험’을 통과하는 브랜드는 극히 드뭅니다. 우리가 최근 몇 년간 파트너십을 맺은 브랜드들을 보면, 우리가 그들의 제안(proposition)에 흥분하기까지 그들이 시장에서 최대 20년을 보냈습니다. 신규 브랜드 출시는 매우 쉽습니다. 결국 제품을 만드는 것 자체는 그리 복잡하지 않고, 도와줄 제3자도 많기 때문입니다. 그러나 그것을 확장(escalate)하고, ‘한순간의 유행’을 넘어서는 것은 매우 어렵습니다. 차별화된 ‘이유’, ‘관점(point of view)’이 있어야 하며, 모든 브랜드가 그것을 갖고 있지는 않습니다. 앞으로도 많은 신규 브랜드가 등장할 것입니다. 그 중 99%는 시간의 시험을 통과하지 못할 것이며, 소수만이 확장하여 산업에 의미 있는 자국을 남길 것입니다.

This interview has been edited and condensed.본 인터뷰는 편집 및 축약되었습니다.

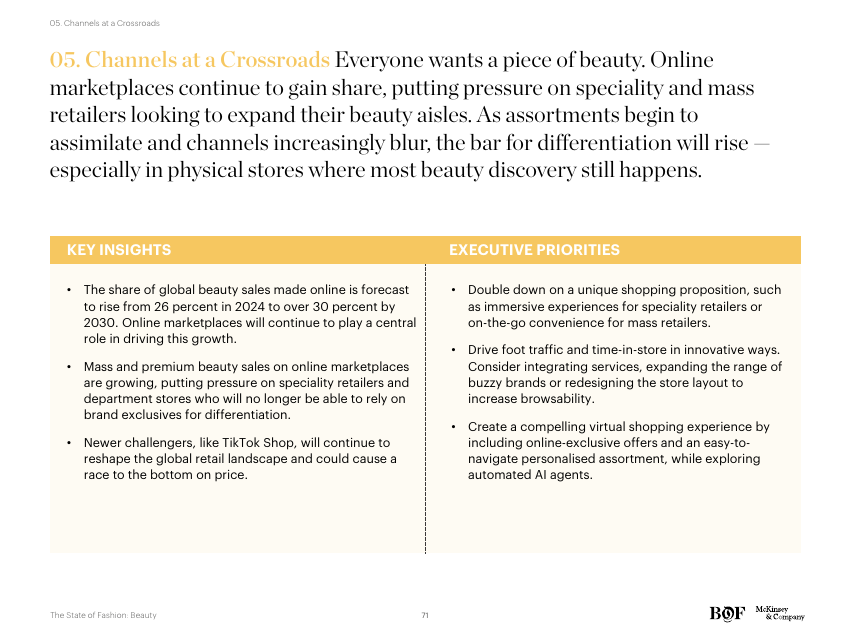

Everyone wants a piece of beauty. Online marketplaces continue to gain share, putting pressure on speciality and mass retailers looking to expand their beauty aisles. As assortments begin to assimilate and channels increasingly blur, the bar for differentiation will rise — especially in physical stores where most beauty discovery still happens.모두가 뷰티의 한 조각을 원합니다. 온라인 마켓플레이스가 지속적으로 점유율을 확대하고 있으며, 이는 뷰티 진열을 확장하려는 전문 리테일러와 매스 리테일러에 압박을 가하고 있습니다. 구색(assortment)이 동질화되고 채널 간 경계가 흐려질수록, 차별화의 허들은 높아질 것입니다 — 특히 여전히 뷰티 발견(discovery)의 대부분이 일어나는 오프라인 매장에서는 더욱 그러합니다.

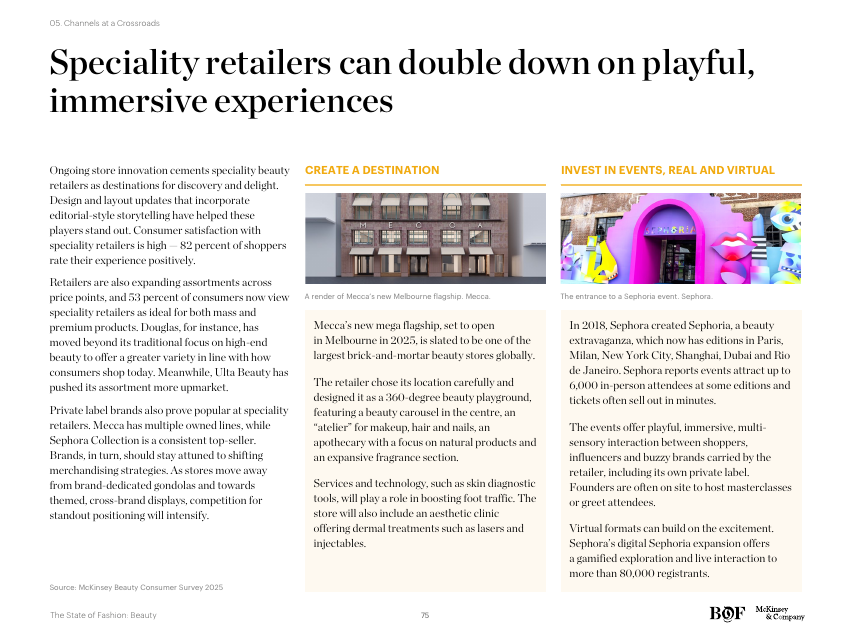

The share of global beauty sales made online could reach one-third by 2030 (from approximately one-fifth today). Marketplaces — especially Amazon and TikTok Shop in the US, Tmall and JD in China, and increasingly the Walmart Marketplace — are the channel of choice for replenishment and discovery search. But brick-and-mortar still dominates true discovery moments; consumers still want to try, smell, and be helped in-store. Pure-play e-commerce brands now invest heavily in physical retail; pure-play physical retailers invest in digital. The convergence is real.글로벌 뷰티 매출 중 온라인 비중은 2030년까지 약 1/3까지 도달할 수 있을 것으로 전망됩니다 (현재는 약 1/5). 마켓플레이스 — 미국의 Amazon과 TikTok Shop, 중국의 Tmall과 JD, 그리고 점차 확대되는 Walmart Marketplace — 는 재구매(replenishment)와 발견 검색(discovery search)의 핵심 채널이 되었습니다. 그러나 ‘진정한 발견의 순간’은 여전히 오프라인이 압도적입니다. 소비자들은 여전히 매장에서 직접 시도하고, 향을 맡고, 도움을 받기를 원합니다. 순수 이커머스 브랜드는 이제 오프라인에 막대한 투자를 하고 있고, 순수 오프라인 리테일러는 디지털에 투자하고 있습니다. 채널 융합(convergence)은 현실입니다.

Walmart operates over 10,000 stores worldwide. Since being appointed VP of beauty in July 2024, Vinima Shekhar has expanded Walmart's premium business to serve value-seeking customers who have grown more discerning, and to capture shoppers who might otherwise go to Sephora or browse online. Walmart was once the undisputed number one beauty retailer in the US, but has ceded share to Amazon. Walmart Marketplace and three-hour delivery are central to the comeback.Walmart은 전 세계적으로 1만 개 이상의 매장을 운영합니다. 2024년 7월 뷰티 부문 VP로 임명된 Vinima Shekhar는, 한층 까다로워진 가치 지향적 고객층에 부응하고 Sephora나 온라인으로 향할 수 있는 고객을 흡수하기 위해, 프레스티지 사업을 확장해 왔습니다. Walmart은 한때 미국에서 압도적인 1위 뷰티 리테일러였으나 Amazon에 점유율을 내준 상태입니다. Walmart Marketplace와 3시간 배송이 동사의 반격에서 핵심 역할을 합니다.

Who is the Walmart beauty customer today, and how will they evolve over the coming years?

오늘날의 Walmart 뷰티 고객은 누구이며, 향후 몇 년간 어떻게 진화하리라 보십니까?

The Walmart beauty customer reflects America. There are over 145 million customers coming to Walmart every week, whether in store or online, but 71 percent of our beauty shoppers are women. Of our customers below the age of 40, 66 percent of them are shopping beauty at Walmart, and these customers are continuing to grow and spend on beauty. Seventy-one percent of beauty customers are making $100,000 or more. The under-40, over-$100,000 segment is actually our fastest-growing cohort. Our assortment is resonating with these high-growth customers.

Walmart 뷰티 고객은 ‘미국 그 자체’를 반영합니다. 매주 매장과 온라인을 합쳐 1억 4,500만 명 이상의 고객이 Walmart을 찾으며, 그 중 뷰티 쇼퍼의 71%는 여성입니다. 40세 미만 고객의 66%가 Walmart에서 뷰티를 구매하고 있으며, 이들은 뷰티 소비를 계속 늘려 가는 코호트입니다. 뷰티 고객의 71%는 연 소득 10만 달러 이상입니다. ‘40세 미만 + 연 소득 10만 달러 이상’의 세그먼트가 사실상 가장 빠르게 성장하는 코호트입니다. 우리의 구색이 이 고성장 고객층에 강하게 호응하고 있습니다.

Do you think the relationship between channel and product is changing?

‘채널과 제품의 관계’가 변화하고 있다고 보십니까?

A hundred percent. The customer is more sophisticated and more knowledgeable, and at the end of the day — I say this all the time — no matter how rich you are, everyone wants to save money and time. That's what positions Walmart really well. We have stores in the South that will carry more sun care products than probably any other geography, and stores in the North that will carry more cold-weather skincare. We localise based on what each community needs. The job is to make sure the right product is in the right store, and that's where our logistics and data capabilities show up.

백 퍼센트 그렇습니다. 고객은 더 정교하고 더 박식해졌으며, 결국 — 저는 늘 이렇게 말합니다 — 얼마나 부유하든 모든 사람은 ‘돈과 시간을 아끼고 싶어 합니다’. 그것이 Walmart을 진정으로 좋은 위치에 둡니다. 남부 매장은 다른 어떤 지역보다 많은 선케어 제품을 진열하고, 북부 매장은 추운 날씨용 스킨케어를 더 많이 진열합니다. 우리는 각 커뮤니티의 필요에 맞춰 로컬라이즈합니다. 핵심은 ‘올바른 제품을 올바른 매장에’ 배치하는 일이며, 그것이 우리의 물류와 데이터 역량이 발휘되는 지점입니다.

How are you working with prestige brands to bring them into Walmart?

프레스티지 브랜드를 Walmart에 입점시키기 위해 어떻게 협업하고 계십니까?

We work with them, we actually give them a path to be successful at retail and invest in those brands. The brands that have come in, like Born to Glow from e.l.f., or our prestige-tier launches with brands that historically only sold at Sephora — they are seeing volume that they could not have anticipated. Walmart reaches a customer base they don't reach elsewhere. The conversation has shifted from ‘will Walmart hurt my brand?’ to ‘how do I get the assortment right at Walmart?’

우리는 그들과 협업하면서, 리테일에서 성공할 수 있는 경로를 함께 제공하고 그 브랜드에 투자합니다. e.l.f.의 Born to Glow처럼 입점한 브랜드들이나, 역사적으로 Sephora에서만 판매되던 프레스티지 브랜드들과의 출시 모두 — 그들은 예상치 못한 수준의 볼륨을 경험하고 있습니다. Walmart은 그들이 다른 곳에서는 도달할 수 없는 고객 기반에 접근합니다. 대화의 본질은 ‘Walmart이 우리 브랜드에 해(害)가 되지 않을까?’에서 ‘Walmart에서 어떻게 올바른 구색을 갖출 것인가?’로 옮겨 갔습니다.

This interview has been edited and condensed.본 인터뷰는 편집 및 축약되었습니다.